Pan Mine, Nevada

1. Introduction

Fiore Gold Ltd. (F:TSX.V; FIOGF:OTCQB) has progressed its Pan Mine in Nevada, U.S. in a very steady fashion, on time and on budget. Exploration for additional resources (and hopefully years of mine life as well) has been successful so far, and a new COO has been hired. Recently, the latest financials regarding the first quarter of the new year were released, which are always an interesting reference of the state of a company, especially with producers. Therefore, it was time to have a closer look at Fiore Gold, Frank Giustra’s baby. Besides an update on proceedings, the other purpose of this article will be the outlining of future cash flow and valuation potential, as I view Fiore Gold as misunderstood by the markets at the moment.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. Pan Mine

The ramping up of the Pan Mine is progressing according to plan, and the company is actually ahead of schedule, as the production rate increased from the planned 10,000 tpd capacity to 14,000 tpd, which was supposed to happen much later. The highlights of the first quarter of fiscal year 2018 are according to the news release:

- Revenues of $8.26 million from the sale of 6,467 gold ounces with a gross margin of $2.54 million or 31%.

- Inventory of 11,335 estimated recoverable ounces placed on the leach pad at Pan as of December 31, 2017.

- Working capital of $13.51 million as of December 31, 2017.

- The first full quarter of steady-state production at the Pan Mine in Nevada.

- Operating costs ($/ore ton) 6.2% below budget for the quarter.

- Successful construction of the Phase II heap leach pad at the Pan Mine, adding an additional 2.2 million square feet of leach pad space. Approximately $5.3 million of capital expenditures for the Phase II expansion was treated as sustaining capital costs for the quarter, resulting in significantly higher All-In Sustaining Costs (AISC) for the current period.

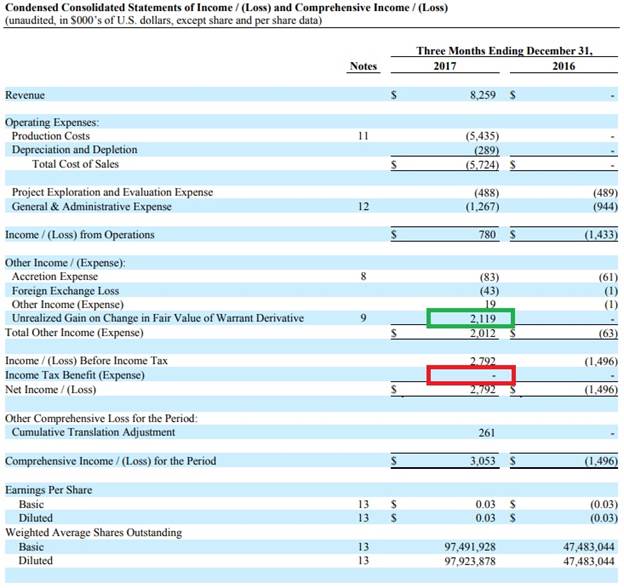

Let’s dig a little deeper into the financials here. In the first quarter of the current financial year, Fiore was surprisingly able to report a comprehensive income of $3.05M, or roughly 3 cents per share. However, this strong net profit was predominantly caused by an unrealized benefit from the fair value of the warrants (in green) and the lack of any tax payments (in red):

The tax holiday is into effect as the company has substantial carry forward losses (in red):

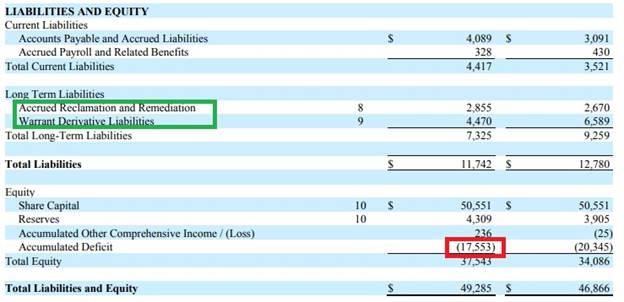

The operating income in the first quarter was $780,000. Fiore Gold is debt-free though, as the long-term liabilities (in green) aren’t long-term debt obligations.

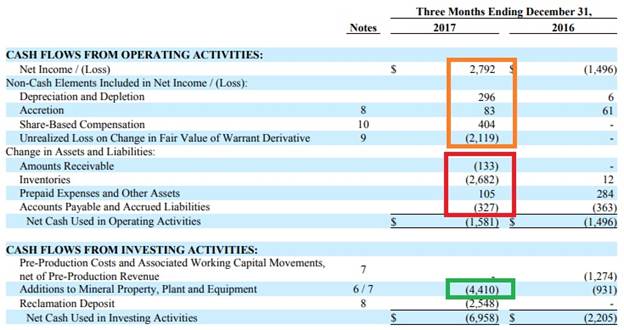

The cash flow statements indicate a ramping up producer as well. The operating cash flow (or OCF, before changes in Fiore’s working capital position, which is the most reliable figure for small producers, especially when ramping up, as OCF after changes can vary a lot in this case) was approximately $1.5M (OCF in orange, without changes in working capital in red, for an operating cash flow of approximately 225 dollar per ounce), and this wasn’t sufficient to cover the $4.4M in capital expenditures (in green):

However, there are two important remarks to make here.

First of all, Fiore Gold plans to produce 35,000-40,000 oz Au this year. Even if the lower end of this guidance is used, Fiore Gold will still have to produce about 35,000 – 6,467 = 28,500 oz Au in the next three quarters of its financial year. This equates to an average of 9,500 oz Au per quarter, or an increase of almost 50% compared to the Q1 production rate.

This means that if production increases, the economies of scale will start to have an effect and the operating margins will improve. Keep in mind that the quoted margin of $225/oz in the first quarter includes $1.267M in G&A expenses. The G&A cost per ounce was $195 in Q1, when this fixed cost could be spread out over 9,500 oz, it drops to $133/oz, which is a pretty substantial improvement. On top of that, the other relatively fixed expenses will also be divided over more ounces. So, the margins will increase as more gold is being produced.

Second, Fiore Gold has guided for a full year capex of $5.5M (red):

On a side note but an important one: comparing the 2018 forecast for gold ounces mined vs gold ounces produced shows a global recovery target of about 50%. However, the Feasibility Study provides a recovery of 72% for an operation with crushers and an agglomerator, and 60% for a run-of-mine operation. As Pan is a heap-leach operation ramping up production, it is never easy to start up heap leach mines, and recoveries often seem a matter of trial and error it seems before all issues are ironed out. The option to add a $14M crusher and agglomerator is a likely one but still uncertain, depending on the outcomes of ongoing test work. A decision on the C&A circuit will likely be made mid-2018, and a realistic timeline on eventual completion of this will be Q1 2019 according to management. At the last PDAC I met with CEO Tim Warman, and he had this to add:

“The idea was always there to use the crusher and the belt agglomerator, but it was such a close call that we decided this could be best tested in a production environment using available space on our newly constructed Phase II leach pad.”

As current working capital stands at $13.5M and the Pan mine is about to become free cash flow positive, the timing is perfect. Let’s continue with the budgeted $5.5M. A big part of this was spent in Q1 alone which means the earlier planned capital expenditures in the next few quarters will be substantially lower as well. Fiore Gold has started a drill program but the combination of higher operating cash flows (due to production increases and margin expansions) and a lower capex should ensure Fiore Gold reaches positive free cash flow.

The interesting thing is that Fiore’s operating costs are pretty much fixed which means the additional ounces will be high-margin ounces. Assuming a production increase of 3,000 ounces per quarter, the operating cash flow will very likely increase by $2.75-3.25M per quarter (assuming $1,300/oz Au, and no taxes will be due for the first few years as mentioned earlier) towards $4.25-4.75M per quarter. Besides this, keep in mind that gold stands at $1353/oz at the time of writing, which could add a further $0.5M per quarter. Furthermore, I’m also assuming the sustaining capex will reach an average of $1.5M per quarter; this should result in Fiore Gold generating approximately $2.75-3.25M per quarter in free cash flow until the taxes start to kick in. And on top of that, U.S. corporate taxes enjoyed a big haircut recently thanks to Trump, so this is beneficial for Fiore in the future. Production will probably improve according to guidance, resulting in an annualized $17-19M operating cash flow in H2, 2018. Using a $1350/oz gold price would result in an annualized $19-21M operating cash flow, which is huge for a small producer in Nevada with just a C$65M market cap. More on this later; let’s have a look at ongoing exploration.

3. Exploration

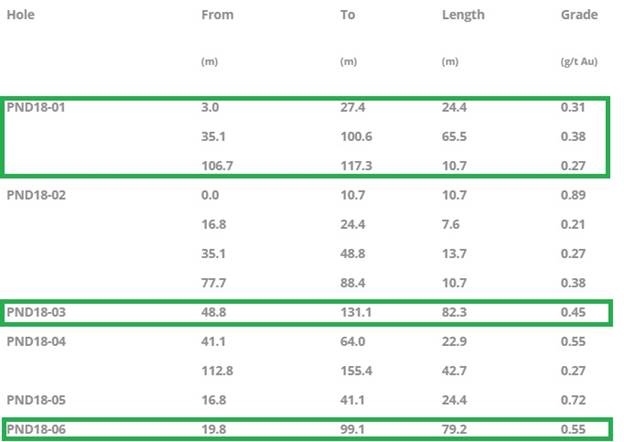

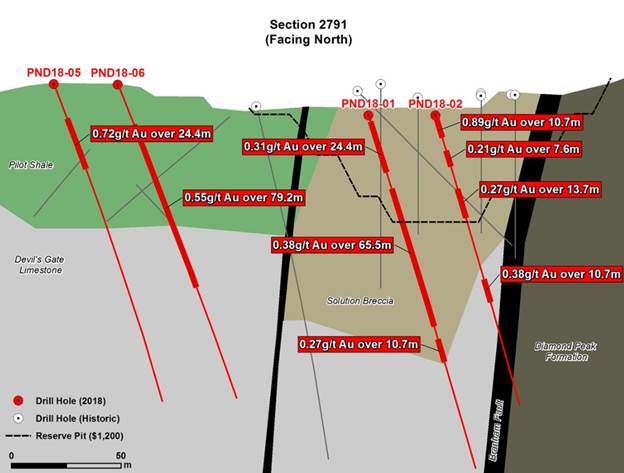

Besides production, Fiore Gold is also busy with exploration on every asset at this time. I will focus on the infill- and stepout drilling on Pan, as management is looking to extend the mine life substantially. The results of the first six holes were released a month ago, and delivered good intercepts, the best ones highlighted in green:

As a matter of fact, all holes returned economic mineralization as the mine cut-off grade is 0.14-0.21g/t Au, according to CEO Tim Warman:

“These first six holes show excellent potential to increase the resource and reserve base both at depth and laterally beyond the current mine plan boundaries. We’re extremely pleased with the success rate so far, with each of the first six holes encountering mineable widths of gold mineralization above the mine cut-off grade. This is a very good start to a program that we’re confident will allow us to extend operations at Pan well beyond the current mine life.”

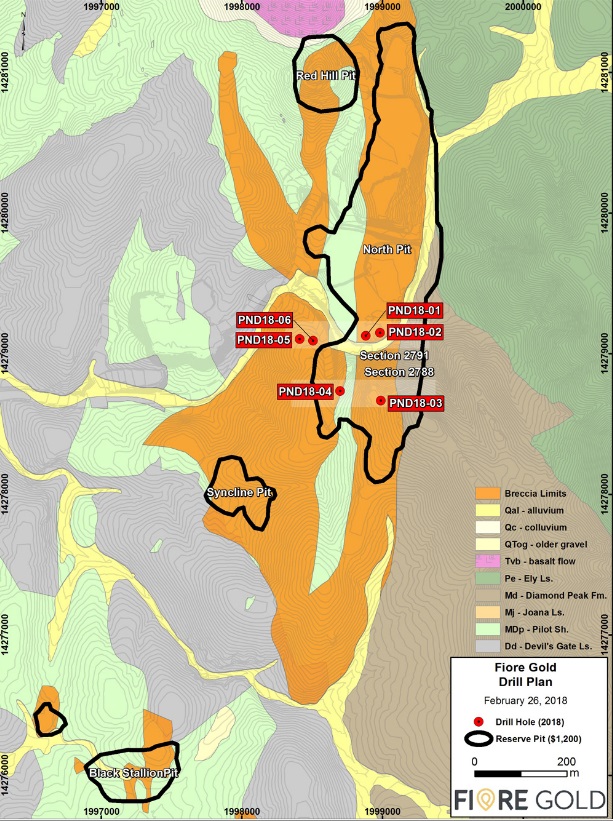

In order to get an idea of locations of drill collars here is a map representing them:

To get a good impression about the significance of these intercepts, let’s have a look at this section:

It will be clear that if Fiore manages to prove up sufficient mineralized tonnage below/west of the current pit outline between PND18-06 and PND18-01, a new and much deeper pit outline could be based on these intercepts and significantly expand mineable reserves/resources. In case ongoing drilling would generate the same kind of results for the entire southern part of the North pit, I wouldn’t rule out an increase of 100-150koz Au, which in turn would extend the life of mine (LOM) to eight to nine years from the current six years.

As the company returned some good intercepts on Pan recently, I felt it was time to ask CEO Tim Warman for some color on proceedings:

TCI: 13 holes were completed, and 6 assays reported so far. When can we expect the remaining 7 assays?

TW: We expect to have those in early April. Through the end of March, we have drilled about 10,000 feet (about 3,000 m), and we expect to do 15,000-20,000 ft RC and DD combined.

TCI: Hole 5 and 6 seem to have resulted in economic mineralization, but hole 3 as an extension at depth at relatively low grade seems unlikely to be economic considering the increased strip ratio?

TW: We think the mineralization of hole 3 isn’t too deep but this area needs more drilling for sure to define new resources.

TCI: Where exactly is further drilling targeted?

TW: Drilling in this first phase is targeting areas close to the North Pit, as well as some smaller future satellite pits in the central part of the deposit.

TCI: I see that RC drilling is used a lot in this round of drilling; don’t you have the risk of contamination with this method in this environment? I recall the same thing happening when Gustavson was working out the resource estimate for Pan in the not-too-distant past.

TW: There is always a bit of smearing with RC, but we understand the deposit a lot better now than in the Midway days. For this type of resource expansion, doing only DD is too expensive now, although we will be doing about 5,000 ft of diamond drilling in key areas.

TCI: Is the Gold Rock resource update planned for late 2018?

TW: We are still planning the program for Gold Rock; we like to fund this from incoming Pan cash flow and use the rig from Pan when drilling is finished there. This will probably be April or May after the snow is cleared.

TCI: Do you have new plans for the Chile asset and the Washington asset?

TW: We are still reviewing plans for the Chilean assets, although we just announced some good exploration results from Rio Loa. As for the Washington asset, we’re talking to a few people about it but it’s still in the early stages.

TCI: The Gold Rock FEIS (= EIA) has been submitted for review, and the Federal Record of Decision should be received before mid-year. What is the status nowadays?

TW: The Record of Decision wraps up the Federal permit, which is the one that takes the longest. The various state permits typically take six to eight months, but we won’t start applying for those until we’ve done a lot more engineering work, since they require fairly specific information.

TCI: Last question: what can you tell us about met work for Gold Rock so far?

TW: The recovery appears to be pretty good, actually a little better than at Pan, Gold Rock has a recovery of about 65-75%. And as you know we are looking at improving Pan recoveries by adding a crusher and an agglomerator.

This concludes the short interview with Tim Warman, which provided a solid update on exploration and related subjects. Now it’s time to take a look at ways how to value Fiore Gold.

4. Valuation

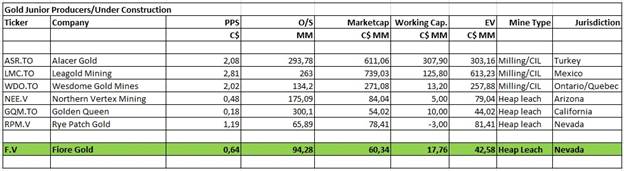

When Fiore Gold is compared to a few other junior gold producers (some data coming from Haywood’s weekly update the Weekly Dig) it can be seen that Fiore Gold is pro forma (as a ramping up producer) valued on EV/CF ratios comparable to the more adventurous jurisdictions like Turkey or Mexico:

And part II:

For the best jurisdictions in this list, Ontario/Quebec and Nevada, the EV/CF metric is substantially higher, and I don’t even consider the corresponding companies top notch although Rye Patch got acquired by Alio Gold very recently.

At a current market cap of about C$61M, it seems that Fiore Gold is valued only on the Pan NPV, when using my estimate from another article on the company:

- the current exploration assets, of which I estimate El Peñon at C$1M and Cerro Tostado at C$4M

- about C$7M in cash, zero debt

- the Pan Mine with a C$65M NPV and ramping up production

- the Gold Rock historical deposit and the exploration potential of both Pan and Gold Rock combined at C$20M

- Golden Eagle at C$5M, bringing the total NAV at C$102M.

Obviously, Pan is discounted by investors, as it is still ramping up production and is looking at adding the crusher and agglomerator for better recoveries, and the market doesn’t appear to assign much value to the other assets. Especially Gold Rock could be capable to add a $80-100M NPV in a few years as it is a bigger and higher grade mineralized project in my view. Nevertheless, the valuation of a producer is usually much better represented by the market cap to operational cash flow ratio (which varies from about 8 to 12 (even 16 for very profitable mines) in good jurisdictions at current gold prices/sentiment), which can be narrowed down further to EV/CF.

When looking at this metric and using the operating cash flow estimates mentioned earlier in this article, the re-rating potential becomes clear. With a potential estimated OCF of $17-19M (= C$22-25M), the company would be valued at 2.0/2.8 times cash flow which is very cheap on EV/CF and P/CF metrics for a profitable Nevada gold play. When Fiore Gold starts generating quarterly cash flows as estimated, and coverage picks up, I am happy to stick with my forecast for a potential double. Increased resources should be able to add LOM years for Pan, and a solid resource on Gold Rock could likely further support a higher valuation.

5. Conclusion

Ramping up to 14,000 tpd steady state went almost flawless for Fiore Gold, as the company did save on operational costs, but didn’t reach its desired 60% run of mine recovery, as it expects to get to 50% for the full year 2018. Therefore, the option to add a crusher and an agglomerator is being evaluated at the moment, increasing recovery, hopefully in line with FS levels. When this staged development would be completed, Fiore Gold will likely boast an annualized cash flow of about C$22-25M, which in turn deserves a much higher share price based on producer average multiples. It is a stock that demands more patience than others, but in the current positive gold environment investors could very well be nicely rewarded in the not-too-distant future.

Pan Mine; scenery

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor. The author holds a long position in this stock. Fiore Gold is a sponsoring company. All facts are to be checked by the reader. For more information go to fioregold.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long term commodity pricing/market sentiments, and often looking for long term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan