Rockridge Resources (TSX-V: ROCK) / (Frankfurt: RR0) is an exploration company focused on acquiring, exploring & developing mineral resource properties in Canada. Its focus is copper & base metals; more specifically — base, green energy & battery metals — of which copper is all three. Not just in any place, only top-tier mining jurisdictions such as Saskatchewan. And, only in mining districts that have had significant past exploration, development or production. And, only projects in close proximity to key infrastructure. Rockridge’s management team, Advisors & Board expertly and methodically eliminate many of the risk factors, early on, that can kill projects. This is a tremendous team for a company with a market cap of just C$5.6M / US$4.2M.

New CEO Bolsters Already Strong Team

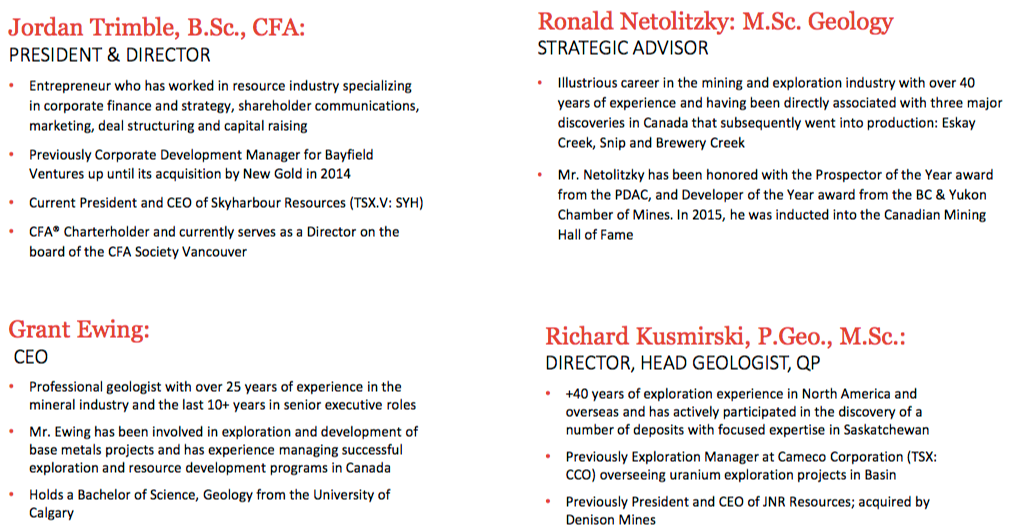

Late last month, Rockridge appointed Grant Ewing, P.Geo to be its new CEO. Jordan Trimble remains as President & a Director. Grant has more than 25 years’ experience in the Metals & Mining space. His expertise covers the mine development cycle, from early stage exploration through to production. I spoke with Grant last week and was impressed with his very extensive knowledge of base metals and his understanding of the district that hosts the Company’s Knife Lake project. Grant seems to be an ideal person to help advance the Project and make new discoveries. Please see more about CEO Grant Ewing, P.Geo here.

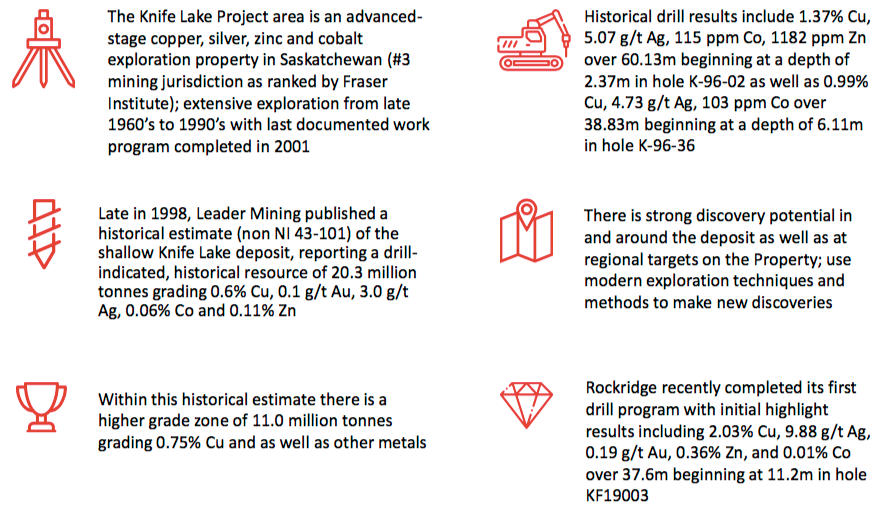

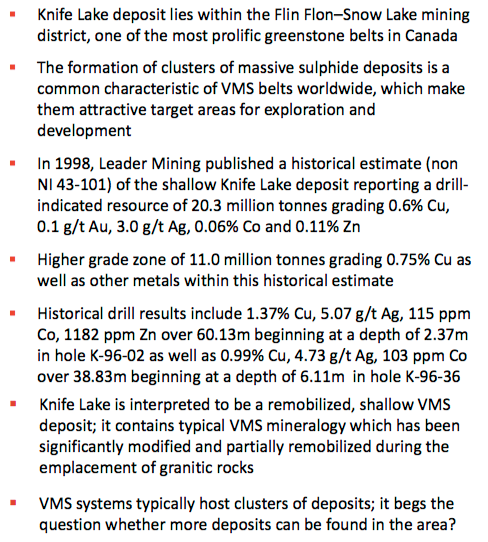

The Company’s flagship project, Knife Lake, is in Saskatchewan, Canada, (ranked 3rd best mining jurisdiction in the world) in the Fraser Institute Mining Company Survey. The Project hosts a near-surface, (high-grade copper) VMS copper-zinc-silver-gold-cobalt deposit, open along strike and at depth. Management believes that there’s strong discovery potential in and around the deposit area, and at additional targets on roughly 85,200 hectares of contiguous claims. As a reminder, Rockridge has an option agreement with Eagle Plains Resources to acquire a 100% Interest in the majority of the Knife Lake VMS deposit.

Flagship Project, Knife Lake, 12 Drill Hole Results Now in….

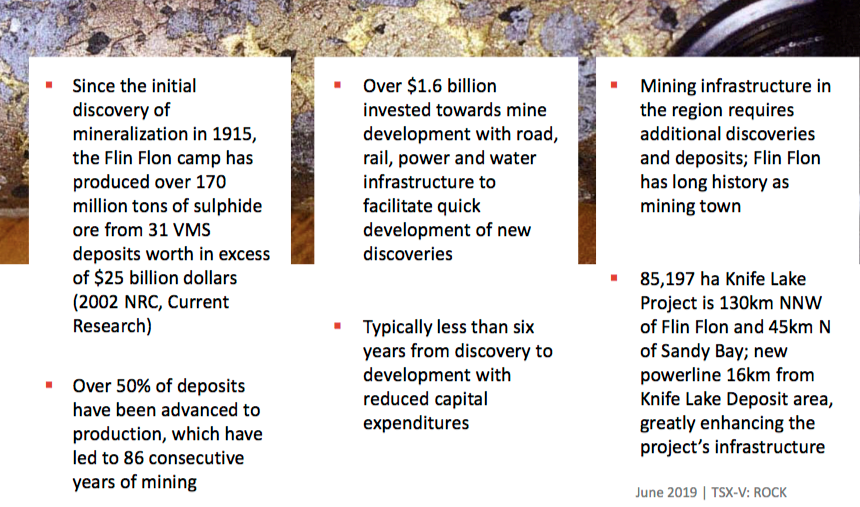

The Project is within the famous Flin Flon-Snow Lake mining district that contains a prolific VMS base metals belt. Management believes there’s tremendous exploration upside. The goal? High-grade discoveries in a mineralized belt that could host multiple deposits, as VMS–style zones often contain clusters of mineralized zones. Of course, the trick is finding them.

However, no modern exploration, drilling method or technology has been deployed at Knife Lake. It was discovered 50 years ago and last explored in the late 1990s. Airborne geophysics, regional mapping & geochemistry was done, but technologies have improved. Management believes that modern geophysics; high resolution, deep penetrating EM & drone mag surveys to cover large areas in detail, could make a big difference.

Earlier this year, Rockridge drilled 12 holes for a total of 1,053 meters. Importantly, this represents the first significant work on the property since 2001. Readers may recall from reading past articles & interviews on Epstein Research & Equity.Guru & Aheadoftheherd, and viewing videos of then CEO Trimble, that the Company’s primary goal is to explore districts that have been under-explored, never explored, or not recently explored. Management’s highly skilled & experienced technical team & advisors deploy the latest exploration technologies & methods. A lot has changed in 18 years; a simple example would be the use of lower-cost, high resolution drones to fly various surveys.

These 12 assays, added to the historical database, will generate a new NI 43-101 mineral resource estimate in late July or early August. This will be a major milestone that will hopefully draw the attention of prospective strategic partners. Subsequent to that de-risking event, Rockridge is funded for a Summer exploration program, that will likely stretch into Fall. The goal is to identify & refine targets at depth and regionally. Modern vectoring techniques will be deployed, using metal ratios & structural interpretation to identify “primary” VMS deposits.

Other modern methods include high-resolution geophysics, deep penetrating EM to identify conductors, and drone mag surveys to cover large areas in detail. Finally, ground work & sampling will be conducted, analyzing rock geochemistry to identify prospective VMS style hydrothermal systems. Importantly, very limited previous drilling was done below 100m, but of the deeper holes, several intersected mineralization at around 300m. Could they be mineralized lenses?

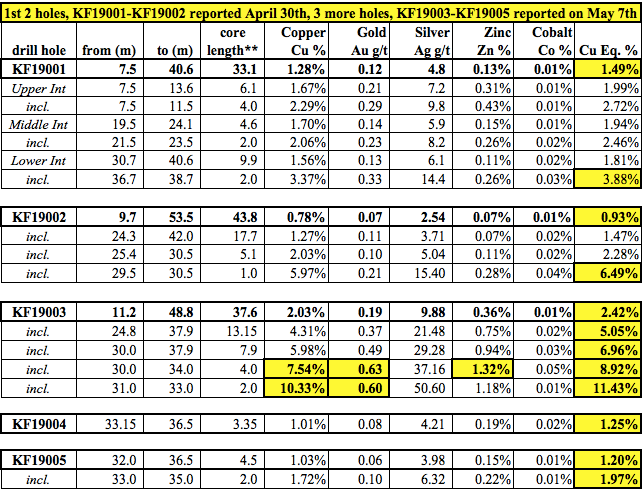

Last month Rockridge reported additional results from its Winter diamond drill program. The first 5 holes are shown in the chart above. Readers may recall that a key takeaway was that holes KF19001 & KF19002 largely confirmed historical grades, intercept widths & geological conditions. Hole KF19003, reported on May 7th, was a blockbuster, 37.6m of 2.42% Cu Eq., significantly better than the first 2 holes. KF19003 had a grade (Cu Eq.) x thickness (in meters) value of 91, compared to 41 & 49. Importantly, it confirmed high-grade mineralization up-dip of KF19002 in an area where no historical drilling is known to have been done. Therefore, this assay, and perhaps nearby assays to follow, could potentially increase the size & grade of the upcoming mineral resource estimate.

Best Intercept in Last 7 Holes: 15.2 m of 2.45% Cu Eq.

In a press release June 10th, holes KF19006 thru KF19012 did not contain any blockbusters, but 6 of 7 were nicely mineralized with Cu Eq. values ranging from 0.46% to 2.45%. The interval widths averaged nearly 8 meters. The best intercept was 15.15 m at 2.45% Cu Eq. in hole KF19006. This intercept is a good one, like those found in holes KF19001 & KF19002, reported in the April 30th. press release. Importantly, KF19006 tested the up-dip extension of the Knife Lake deposit in an area that had not been previously tested. Likewise, hole KF19007 tested the down-dip extension of the deposit near KF19006. KF19007 intersected a solid 2.95 m of 0.82% Cu Eq. grade. The latest property map provided from today’s press release is too large to fit comfortably within this article, please click on link here.

Rockridge’s CEO, Grant Ewing commented:

“The Knife Lake property package is highly prospective for new discoveries using modern exploration techniques & methods given the lack of recent field work. The known deposit is thought to be a remobilized portion of a presumably larger primary VMS deposit, and there is excellent potential for deposit expansion at depth which we plan to test in future programs. Furthermore, there are several high quality targets to test on the expansive landholding, and there have yet to be satellite deposits discovered in the vicinity as VMS systems often host clusters or stacked deposits.”

Something I found interesting was the 2 portions of the 15.2 m intercept in KF19006 that assayed 7.25 m of 0.72 g/t Gold, (from 8.75 to 16.0 m), and 5.0 m of 0.93 g/t Gold, (from 11.0 to 16.0 m), both within 16.0 m of surface. Those 2 grades (true widths undetermined) are the highest Gold values reported to date. The 0.93 g/t showing is nearly 50% higher, and 1.0 m longer, (5.0 vs. 4.0 m) than the next highest grade Gold showing, in blockbuster hole KF19003. While intriguing, these values in isolation may not amount to much. Still, they’re worth keeping an eye on.

Rockridge’s President & Director, Jordan Trimble commented:

“The results from this first-pass drill program have exceeded our expectations with almost all drill holes having intersected high-grade copper mineralization, and in doing so, we have successfully confirmed the tenor of mineralization reported by previous operators, while expanding known zones of mineralization. We are working towards issuing an NI 43-101 compliant resource estimate as well as planning a regional summer field program, both of which will provide steady news flow and catalysts over the near term. We will continue to execute on our value creation strategy of going into overlooked but prospective projects in prolific mining jurisdictions and using modern exploration methodologies to test new ideas and make new discoveries.”

The deposit remains open at depth. Additional discoveries are very possible as the property is nearly 85,200 hectares in size and vastly under-explored. The Winter drill program gives the Company’s technical team valuable information about geology, alteration & mineralization that will be applied to regional exploration targets. The Company is now working towards completing an NI 43-101 compliant resource estimate for Knife Lake with the results from this drill program. A summer exploration program is also being planned, details to follow.

Conclusion

As mentioned, Rockridge Resources (TSX-V: ROCK) / (Frankfurt: RR0) has a tremendous team — Management, Board & Advisors — for a company with a market cap of C$5.6M = US$4.2M. Readers should take just 5-10 minutes to review the Company’s new June Corporate Presentation. And, the latest press releases can be found here. The flagship Knife Lake project is large enough, at ~85,200 hectares, to keep the Company busy for years to come. Even if management were to farm out (get free-carried) a portion of the Property, there would still be tens of thousands of hectares remaining to explore in a top mining district in Canada.

Copper prices are down into the US$2.60’s/lb. from close to US$3/lb., but near-term fluctuations in the price are meaningless for anyone who believes that copper is needed for, 1) clean-green energy storage, 2) the global electrification of passenger & commercial vehicles, and 3) the surge of infrastructure building needed to accommodate a growing global middle-class population migrating to ever-larger cities. Not to mention the re-building of old and destroyed infrastructure like buildings, roads & bridges. Everything uses copper, everything will continue to use copper. The price of copper has to rise, or there won’t be enough copper, it’s that simple. Several experts believe that the copper price is headed to US$4-$5/lb. by 2020 or 2021. If so, a company like Rockridge Resources has a lot of leverage to that outcome.

Peter Epstein

Epstein Research (ER)

June 13, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] about Rockridge Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Rockridge Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock in Rockridge Resources and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

The major gold miners’ stocks remain mired in universal bearishness, largely left for dead. They are just wrapping up their third-quarter earnings season, which proved challenging. Lower gold prices cut deeply into cash flows and profits, and production-growth struggles persisted. But these elite companies did hold the line on costs, portending soaring earnings as gold recovers. Their absurdly-cheap stock prices aren’t justified. Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the U.S. Securities and Exchange Commission by 40 calendar days after quarter-ends. Canadian companies have similar requirements at 45 days. In other countries with half-year reporting, many companies still partially report quarterly.

These quarterlies offer the best fundamental data available for individual major gold miners, showing how their operations are really faring. That helps dispel the thick obscuring fogs of sentiment that billow up the rest of the time. While I always eagerly anticipate perusing these key reports, I worried what this Q3’18 earnings season would reveal. Lower gold prices, flagging production, and weak sentiment are a witches’ brew.

The definitive list of major gold-mining stocks to analyze comes from the world’s most-popular gold-stock investment vehicle, the GDX VanEck Vectors Gold Miners ETF. Its composition and performance are similar to the benchmark HUI gold-stock index. GDX utterly dominates this sector, with no meaningful competition. This week GDX’s net assets are 50.5x larger than the next-biggest 1x-long major-gold-miners ETF!

GDX is effectively the gold-mining industry’s blue-chip index, including the biggest and best publicly-traded gold miners from around the globe. GDX inclusion is not only prestigious, but grants gold miners better access to the vast pools of stock-market capital. As ETF investing continues to rise, capital inflows into leading sector ETFs require their managers to buy more shares in underlying component companies.

My earnings-season trepidation soared on October 25th. The gold stocks were doing fairly well then, with GDX rallying 14.4% out of mid-September’s deep forced-capitulation lows . Sentiment was slowly improving. But that day GDX plunged 4.4% out of the blue, and the flat gold price at upleg highs certainly wasn’t the driver. The most-loved major gold miner had plummeted after reporting shockingly-bad Q3 results. Goldcorp has always been one of GDX’s top components. It reported mining just 503k ounces of gold last quarter, which plunged 11.9% sequentially quarter-on-quarter and 20.5% year-over-year! That forced its all-in sustaining costs a proportional 20.8% higher YoY to $999 per ounce. Investors panicked and fled, hammering GG stock 18.7% lower. That was the worst down day in the 24.6-year history of this company.

That left it at an extreme 16.2-year low! GG hadn’t been lower since August 2002 when gold was still in the low $300s, it was apocalyptic. That really torpedoed still-fragile sentiment in this sector, even though GG’s woes looked short-lived. It was bringing a new expansion online at one of its big mines, which was what caused the shortfall. Now in Q4’18 Goldcorp expects production to rebound to 620k ounces at $750 AISCs.

After GG’s Q3 disaster, I worried frayed investors would dump other gold stocks on any hints of less-than-optimal quarterly results. But GDX has ground sideways on balance since that GG shock, weathering this risky earnings season with sentiment so fragile. Ever since I’ve been anxious to analyze the collective Q3 results of the major gold miners as a whole, to see if GG’s travails were unique to it or more systemic.

GDX’s component list this week ran 48 “Gold Miners” long. While the great majority of GDX stocks do fit that bill, it also contains gold-royalty companies and major silver miners. All the world’s big primary gold miners publicly traded in major markets are included. Every quarter I look into the latest operating and financial results of the top 34 GDX companies, which is just an arbitrary number fitting neatly into these tables.

That’s a commanding sample, as GDX’s 34 largest components now account for a whopping 93.5% of its total weighting! These elite miners that reported Q3’18 results produced 296.4 metric tons of gold, which accounts for fully 33.9% of last quarter’s total global gold production. That ran 875.3t per the recently-released Q3’18 Gold Demand Trends report from the World Gold Council. I’ll discuss production more below.

Most of these top 34 GDX gold miners trade in the U.S. and Canada where comprehensive quarterly reporting is required by regulators. But some trade in Australia and the U.K., where companies just need to report in half-year increments. Fortunately those gold miners do still tend to issue production reports without financial statements each quarter. There are still wide variations in reporting styles and data offered.

Every quarter I wade through a ton of data from these major gold miners’ latest results and dump it into a big spreadsheet for analysis. The highlights make it into these tables. Blank fields mean a company had not reported that data for Q3’18 as of this Wednesday. Looking at the major gold miners’ latest results in aggregate offers valuable insights on this industry’s current fundamental health unrivaled anywhere else.

The first couple columns of these tables show each GDX component’s symbol and weighting within this ETF as of this week. While most of these stocks trade on US exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each gold miner’s Q3’18 production in ounces, which is mostly in pure-gold terms. That excludes byproduct metals often present in gold ore. Those are usually silver and base metals like copper, which are valuable. They are sold to offset some of the considerable costs of gold mining, lowering per- ounce costs and thus raising overall profitability. In cases where companies didn’t separate out gold and lumped all production into gold-equivalent ounces, those GEOs are included instead. Then production’s absolute year-over-year change from Q3’17 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, revenues, and cash on hand with a couple exceptions. Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. This whole dataset together offers a fantastic high-level read on how the major gold miners are faring fundamentally as an industry. Was Goldcorp’s disaster systemic?

The recent weakness in Gold and gold mining stocks is not over. In fact, we are worried about another leg down getting underway.

If that comes to pass, we are positioned to profit from it. But I digress.

Long-term oriented investors and speculators should be aware of the near term trends but they should also be aware of the conditions that will lead to a shift from a bear market to a bull market.

Here, we focus on five factors that precede major bottoms in precious metals.

Gold Outperforms the Stock Market

Other than in 1985 through 1987 there has never been a real bull market in Gold without it outperforming the stock market. A weak stock market usually coincides with conditions that are favorable for precious metals. That’s either high inflation or economic weakness that induces policy that is usually bullish for precious metals. The 2016-2017 period failed to be a bull market because the equity market continued to outperform Gold. Note that the Gold to Stocks ratio bottomed prior to the 2001 and 2008 bottoms.

Gold Outperforms Foreign Currencies

Gold outperforming foreign currencies is important because this usually happens while the US Dollar remains in an uptrend. It signals relative strength in Gold and shows that Gold is not being held hostage by the strong dollar. It also can signal a coming peak in the dollar. Gold was outperforming foreign currencies prior to the 2001, 2008 and late 2015 bottoms. There are currently no positive divergences in place.

Major Peak in the US Dollar

This does not precede bottoms in Gold as it typically is a lagging indicator. But a list of “4” things does not carry the same weight as five. Anyway, Gold is not going to embark on a major, long-lasting bull market without a corresponding peak in the US Dollar. Sure, they can rise at the same time and for months on end. However, it’s difficult to imagine a multi-year bull market in Gold without a corresponding peak in the dollar. Peaks in 1993 and 2016 led to brief runs in Gold but those were nothing like the 1985 and 2001 peaks.

Gold Mining Stocks Crash

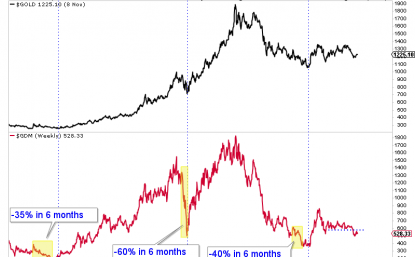

This is not a mandatory component of major bottoms but definitely is something that can occur before a major bottom. Below we plot GDM, which is the forerunner to GDX. Note that gold stocks essentially crashed into their late 2000 and late 2008 lows. They also crashed into their summer 2015 low which wasn’t the final low for the sector but was for the senior miners. The main point is that if gold mining stocks fall apart again it could very well be a sign that a bottom is almost imminent.

Fed Policy Change

Over the past 60 years, gold stocks have often bottomed almost immediately after the peak in the Fed Funds rate (FFR). In 10 of 12 rate cut cycles, gold stocks bottomed a median of one month and an average of two months after the peak in the FFR. The average gain of gold stocks following that low was 185%. There are also points where the gold stocks declined during a period of rate cuts or no Fed activity. Bottoms then were sometimes followed by the start of Fed hikes. However, given the current conditions, we are quite confident that gold stocks will bottom immediately after the Fed’s final rate hike.

Now you know what to look for to signal that a major bottom is imminent.

Better yet, consider our premium service which can help you ride out the downside and profit ahead of a major bottom in the sector. To prepare yourself for an epic buying opportunity in junior gold and silver stocks in 2019, consider learning more about our premiums service.

The S&P/Venture Composite Index finished down 0.3% to 768.04 and the S&P/TSX Global Mining index was up 0.15% to 66.52 for the day as the summer doldrums roll on. Gold closed up $1.50 at $1274.90 while silver closed down 9 cents to $16.70 and copper down 1.6 cents to $2.875. On the TSX Venture, 327 issues advanced, while 368 remained unchanged and 365 declined, 115,365,198 shares traded hands in 19,555 trades worth approximately $54,171,000. On the day, 21 companies reached new highs while 69 reached new lows on the Venture Exchange and 8 venture mining companies released drill results and sample assays.

The S&P/Venture Composite Index finished down 0.3% to 768.04 and the S&P/TSX Global Mining index was up 0.15% to 66.52 for the day as the summer doldrums roll on. Gold closed up $1.50 at $1274.90 while silver closed down 9 cents to $16.70 and copper down 1.6 cents to $2.875. On the TSX Venture, 327 issues advanced, while 368 remained unchanged and 365 declined, 115,365,198 shares traded hands in 19,555 trades worth approximately $54,171,000. On the day, 21 companies reached new highs while 69 reached new lows on the Venture Exchange and 8 venture mining companies released drill results and sample assays.

Precipitate Gold Corp. (PG) released results that included the discovery of mineralization in a previously untested anomaly to the south of the main zone yielding a 1.1-metre interval of 2.59 grams per tonne gold (including 0.11 per cent copper, 0.6 per cent lead and 0.65 per cent zinc) (GR17-15) and a main zone drill intercept of 14.73 metres of 1.16 grams per tonne gold, including 2.67 metres of 2.23 grams per tonne gold (GR17-13). Laboratory results are pending for eight more holes.

Klondike Gold Corp. (KG) reported today results from its lonestar property in the Yukon with 30.7 m of 1.6 g/t Au at Lone Star in the Yukon. Thus far in 2017, the drill program has completed 35 holes. Assays for the earliest 11 holes have been received, including 9 holes released today. Twenty-four holes are still in the lab queue, while drilling continues. The market response to the news was muted as shares in the company were down half a cent on 209,000 shares to 30 cents.

Panoro Minerals Ltd. (PML) provided an update of its exploration drill program at its Cotabambas copper-gold-silver project in Peru. Highlights of the program are from Drillhole CB-157, the first hole completed at the Maria Jose zone, intersected 195.2 m of copper mineralization grading 0.34 % Cu, 0.06 g/t Au and 1.6 g/t Ag. Shares of the company remain unchanged at 15.5 cents for the day.

Altamira Gold Corp. (ALTA) identified two new zones of mineralization have been identified at both Baldo East and Toninho, at its Cajueiro Project, Brazil. Results from the initial five trenches at Baldo East include 3m @ 6.54g/t gold including 1m @ 17.54g/t gold, and 6m @ 2.26g/t gold, and 3m @ 5.83 g/t including 1m @ 16.24g/t, and 1m @ 9.15g/t, and 9m @ 1.19 g/t including 1m @ 5.62g/t . Shares in the company were down half a cent to 18.5 cents on 286,700 shares.

Aurion Resources Ltd. (AU) released 452 rock samples assayed from nil to 2,520 grams per tonne (81.4 ounces per ton) with 32 assaying greater than 31 g/t Au (one ounce per ton), 45 greater than five g/t Au and 70 assaying greater than 1.0 g/t Au from its Aamurusko gold prospect, Finland. Share price declined 3 cents to $1.78 on 436,000 shares.

Margaux Resources Ltd. (MGX) released the results from initial surface rock sampling on its Bayonne and Jackpot properties, in Southern British Columbia. The results include gold assays from grab samples of up to 27.5 g/t (grams per tonne) gold on the Bayonne and widespread zinc mineralization at Jackpot including 20.8 per cent zinc from Jackpot Main. Shares in the company remained unchanged at 28 cents on 50,500 shares.

Galantas Gold Corp. (GAL) reported grab samples of between 1.1 and 11.0 grams per tonne gold and between 1.4 and 7.0 g/t silver from its underground mine Omagh Gold Mine, Ireland. The share price remained unchanged at 8 cents on 20,000 shares.

Mexican Gold Corp. (MEX) released its initial mineral resource estimate for the El Dorado/Juan Bran and Santa Cruz zones at its Las Minas project, Mexico. Total measured and indicated resource amount to 304,000 ounces AuEq contained within 4.97 million tonnes grading 1.9 g/t AuEq. The initial mineral resource estimate is for two of the eight known zones of mineralization at Las Minas. The company was halted at remains so at the end of the trading day.

According to TMX earnings calendar for the TSX venture, Avino Silver and Gold Mines Ltd. (ASM) should be releasing its second quarter 2017 results after the close of the market on August 2, 2017. Barkerville Gold Mines (BGM), North Arrow Minerals Inc. (NAR), and Orsu Metals Corp. are expected to be publishing their earnings tomorrow as well.

© 2017 MiningFeeds.com. All rights reserved.

ANGLO American’s (LSE:AAL) recent corporate maneouvres have really caught the eye, especially the sale of its 24.5% stake in Anglo American Sur, its Chile base metals company, to Mitsubishi.

Analysts have described it as ‘fancy footwork’ and ‘corporate theater’; another, in martial terms as Anglo having ‘outflanked’ Codelco. Codelco is Chile’s state-owned mining company that last month announced its intention to exercise its option agreement over Anglo American Sur in January.

For me, I can only wonder, again, at the power of the team. In rejecting Xstrata’s (LSE:XTA) merger of equals proposal two years ago, Anglo CEO Cynthia Carroll not only saved her job but got herself a steely board of directors.

As a colleague of mine once said, the softest part of Sir John Parker, the industrialist drafted into Anglo at the time of the Xstrata bid, is his tooth enamel. The swiftness of the Mitsubishi move has the paws of a sly fox all over it. I’d love to know how this plan was hatched, when, and by whom.

In any event, Anglo has at a stroke achieved a few things. It has increased the valuation of 100% of Anglo American Sur 10% to $22 billion against the $19.9 billion value attached to the company by Codelco (and financier, Mitsui).

Secondly, Anglo seems confident it has reduced the amount of the stake over which Codelco has its lower value option agreement. So if Codelco exercises its option, the company will be shared as follows: Anglo American (51%), Mitsubishi (24.5%) and Codelco (24.5%).

Thirdly, Anglo also has the optionality of dispensing the remaining 24.5% Codelco still has rights over which the government can only do in January. An Anglo spokesperson confirmed the group could have sold 50% of Anglo Sur if it had wanted.

Assuming Anglo doesn’t do this, and waits for Codelco to exercise its option, it will stand to bag some $8.4 billion (before capital gains tax on the Mitsubishi sale which is a whopping $1 billion). This fourth element of Anglo’s coup raises the question again: what will Anglo do with the cash?

One analyst, who asked not to be named, said there would be enough cash left over to build a balance sheet robust enough to buy out the Oppenheimer family’s stake in De Beers – the other corporate manoeuvre which earned Carroll kudos earlier this month – and take out Kumba Iron Ore minority shareholders, equal to 35% of total shares in issue valued at some $7 billion.

Shares in Kumba Iron Ore (JSE:KIO) have increased 11.5% since November 1. It’s worth noting that the volatility in iron ore prices didn’t much affect the company given the niche value of its product suggesting the possibility of a takeout might be getting priced into the share, perhaps.

From the article entitled, “Anglo may line up Kumba Iron Ore” by David McKay of Miningmx. Miningmx is a leading online publication providing news, editorial and analysis on the African resources sector. The information provided herein has been provided to MiningFeeds.com by the author and, as such, is subject to our disclaimer: CLICK HERE.

In mining and economics, base metals are often referred to as non-ferrous metals. Non-ferrous metals is a broad category that includes the likes of aluminum, molybdenum, tantalum and magnesium. However, ‘The Big 5’ in the group are copper, zinc, lead, nickel and iron.

When investors think of base metals they probably think of China as well. China’s metal capacity continues to rise, 2010 was a record production year for all base metals and China is ranked number one in the world for output of aluminum, lead, zinc and tin. It is also the leading copper and nickel consumer.

Base metals oxidize, tarnish or corrode relatively easily when exposed to air or moisture. Base metals are widely used in commercial and industrial applications. They are more abundant in nature and therefore far cheaper than precious metals such as gold, silver and platinum.

The term “base” metals arose because these materials are inexpensive and more commonly found than “noble” metals such as gold and platinum; however, base metals are invaluable to the global economy because of their utility and ubiquity.

Copper, a leading base metal, is often called the “metal with a Ph.D. in economics” because its widespread use makes its price very sensitive to global economic trends. For this reason, many call it “Dr. Copper”.

MiningFeeds.com

Base metal mining companies have, for many years, operated in the shadows of precious metal miners. But with increasing demand from China and developing nations around the world, base metal miners may finally be getting the respect they deserve. Patricia Mohr, commodities specialist at Scotiabank, recently went so far as to call copper the ‘new gold’. Mohr says “Copper is much more profitable than gold. Considerably more, even with the record gold prices we’ve been seeing recently. That’s why I’ve been calling copper the new gold.”

Lately, other base metals have also fared well. Prices for nickel, zinc, iron and lead have rebounded dramatically from 2008/2009 lows and since stabilized. Unlike copper, however, other base metals have not reached new highs as the world recovers from the economic downturn.

Tom Whelan, head of mining and metals research at consultancy firm Ernst & Young notes, “Statistics from the Chinese government indicate demand (for copper) will grow to 12 million tonnes over the next 10 years on an annual basis. But the world’s supply won’t expand fast enough to keep up with the demand. It’s not like mining companies can just flip a switch.” China currently consumes 7 million tonnes per year or almost 40% of world’s supply.

One need look no further than Barrick Gold’s takeover offer of Equinox Minerals to illustrate that precious metals miners are becoming increasingly more comfortable with copper. Copper is of natural interest because it’s often found in deposits with gold.

The Grasberg Mine, located in the province of Papua, Indonesia, is both the largest gold mine and the third largest copper mine in the world. And the Grasberg mining district contains the world’s largest recoverable copper reserve and the largest gold reserve. It is majority owned through a subsidiary by Freeport-McMoRan Copper & Gold (NYSE: FCX). Annual production from the Grasberg Mine is estimated at over 600,000 tonnes of copper; 58,000,000 grams of gold; and 170,000,000 grams of silver.

Gold, and lately, even silver have gained cultish disciples that the less glamourous base metals cannot hope to match. But those looking for dependability in their investments can be assured of one simple metric; as the world grows, so too will the demand for industrial metals. To some, the dynamic between supply and demand for base metals in emerging markets can only mean one thing: good news for miners in the medium to long-term.

1. Lundin Mining Corp. (TSX:LUN)

On February 28th, 2011 Equinox Minerals launched a hostile bid for Lundin Mining that left Symterra blowing in the wind. Symterra was the proposed name of a new entity resulting from the friendly merger between Lundin Mining and Inmet Mining – a transaction valued at $9 billion.

Although Lundin pushed hard to complete the merger with Inmet Mining and thwart off the unsolicited bid from Equinox, Symterra was ultimately derailed after Panama imposed development rules that affected the proposed power supply to Inmet’s Cobre Panama mine. Panama’s government opposes the construction of a coal-fired power plant to supply electricity. Inmet CEO Jochen Tilk pointed out the mine would not face delays if the plant isn’t built because the project could rely on power from the national grid in the first few years of operation. At the time, Peter Campbell, a Toronto-based analyst at Jennings Capital Inc., said Lundin may be preparing to back out of its deal with Inmet, citing “material adverse change” in relation to the Cobre Panama project.

The merger and acquisition saga became even more convoluted when Barrick Gold, the world’s biggest gold producer, announced on April 25th, that it planned to buy Equinox for US$7.3 billion. Barrick President and CEO stated, “The acquisition of Equinox would add a high-quality, long-life asset to our portfolio and is consistent with our strategy of increasing gold and copper reserves through exploration and acquisitions.” Equinox’s main asset is the Lumbwana mine in Zambia, one of the largest copper mines to be developed globally in the last few years.

Prior to Barrick’s offer, Equinox was in the process of defending against its own unsolicited US$6.3 billion bid from China’s Minmetals Resources. But a substantial offer from Barrick was enough to scare off Minmetals and they promptly withdrew their offer. CEO of the Hong Kong Unit of one of China’s largest mining companies Andrew Michelmore noted, “Competing with Barrick at these prices would, in our view, be value destructive for MMR’s shareholders.”

With the Equinox board in support of Barrick’s offer, which included, that they terminate the Lundin offer or let the offer expire, this could be the third time a high-profile takeover has fallen apart for Lundin. In 2008, HudBay Minerals’ bid for Lundin was unsuccessful after its own shareholders objected to the deal.

So what’s next for Lundin Mining? For now, the company is neither hunter nor prey – or is it? On Friday April 29th, it was leaked to the press that a buying group headed by one of China’s largest base metal miners, Jinchuan Group Ltd., and includes the country’s giant sovereign wealth fund, China Investment Corp. was “in talks” to buy the company. Shares of Lundin Mining traded over 21 million shares on the day and closed at $9.26 up $0.92 on the speculative news.

2. Canada Zinc Metals Corp. (TSXV:CZX)

Zinc, the fourth most used metal on the planet trailing only iron, aluminum and copper, has a worldwide annual production of roughly ten million tonnes. Zinc’s primary use is in the galvanizing process of steel and in making alloys including brass and bronze. Although zinc doesn’t get anywhere near the same amount of attention as its sexier cousin copper, that may begin to change. China’s refined copper imports fell 43 percent in March year over year due to high stock piles and strong international prices while their Zinc imports surged 108 percent over last year.

In November 2006, Zinc prices hit a record high of US$4,580 tonne. At the time, analysts cited that the growing demand for zinc in China could increase by 56% by 2010 which certainly helped fuel the fire. China became a net importer of zinc in 2004. With the onset of the “Great Recession” in 2008 the price of zinc declined dramatically to just above $1,000 per tonne, far below the bullish projections a few years earlier. But in the first quarter of 2009, as marginal zinc mines were being shut down all over the world, zinc began a swift and steady recovery, reaching US$2,560 per tonne by the end of the same year, just slightly higher than where it currently trades.

Today, China produces about a quarter of the world’s zinc and consumes a third of it. And overall, Zinc consumption in China has tripled since 2000 – China consumes more zinc than USA, Japan, India, Germany, Italy and Belgium combined. Some analysts, however, believe this time China’s demand for zinc will continue unabated. This, coupled with demand from other emerging nations around the world is expected to push consumption to 15.5 million tonnes per year by 2020.

Peeyush Varshney, President and CEO of TSX-V listed Canada Zinc Metals is solidly in this camp. In August, 2005 Canada Zinc Metals entered an earn-in option agreement for 65% of its Akie property. A few years later, in 2007, the company acquired 100% of the Akie property and their entire claim package pursuant to a takeover. The next year the company completed its first NI 43-101 report on the Akie property. Soon after, China came calling in the form of Tongling Nonferrous Metals Group which subsequently made a substantial investment in Canada Zinc Metals. MiningFeeds.com sat down with Peeyush Varshney, President & CEO of Canada Zinc Metals to find out more about the company’s Chinese shareholder and what else is in store for 2011. CLICK HERE – for the interview.

For 10 Base Metal Stocks to Watch in 2011 – Part 2 – CLICK HERE.

Disclosure: at publication Canada Zinc Metals is a client of MiningFeeds.com.

3. Mirabela Nickel Ltd. (TSX:MNB)

By the end of 2008 Nickel prices had fallen by 80% from their May 2007 high of just over (US) $52,000 per tonne. In the first half of 2009, in the midst of the economic crisis, around a quarter of all nickel production from 2008 was suspended. Major producers such as Norilsk Nickel, BHP Billiton, Vale Inco and Xstrata all had to curtail production. Since then, prices have stabilized; nickel currently trades on the London Metals Exchange for US$26,605 per tonne.

Mirabela Nickel’s focus is its Santa Rita project in Bahia, Brazil. The company says the mine is expected to be among the largest open-pit nickel sulphide mines in the world, with an estimated life of 23 years. Proven and probable reserves are reported to be 121 million tonnes at 0.60% Ni (726,000 tonnes of contained nickel); and, the company’s nickel sulphide concentration plant produces metal concentrate (nickel-copper-cobalt) containing approximately 14% nickel.

Mirabela has off-take agreements covering 100% of its nickel production until December 2014 with Votorantim Metais, a Brazilian mining company that is the world’s sixth largest nickel producer worldwide. In addition, the company has an agreement with Norilsk Nickel, the world’s largest producer. Votorantim takes delivery at the mine site and then trucks the concentrate to its Fortaleza de Minas smelter in Brazil. Mirabela ships the concentrate to Norilsk CIF Rotterdam where it is then transported to Norilsk’s Harjavalta refinery in Finland. Payment is determined based on the metal content of the nickel concentrate produced and market metal prices.

Unfortunately, Santa Rita’s slower than expected production ramp-up led Mirabela back to the equity market. On April 15th, 2011 the company announced the closing of a US$395 million of 8.75% senior unsecured notes. Once released from escrow, Mirabela intends to use the net proceeds to pay down its senior and subordinated debt facilities, to make prepayments in connection with the termination of certain commodity call options, interest rate hedging and foreign exchange hedging, to provide further general working capital and for general corporate purposes.

Standard & Poor’s rated the notes ‘B-‘ whereby S&P credit analyst Thomas Jacquot said, “The ‘B-‘ corporate credit rating reflects our view of Mirabela’s lack of geographic and revenue diversity, which stems from the operation of a single site in Brazil that is almost exclusively focused on the extraction of nickel, a product that has historically experienced high price volatility.” He went on to say, “We believe, however, that the combination of performance to date in the ramp-up of the Brazilian mining operations, the company’s adequate liquidity, and the experience of the management team will partially offset those weaknesses. In addition, we expect performance and profitability to improve during 2011, provided nickel prices are maintained at current levels and the company is able to deliver its remaining capital expenditure on time and budget.”

In response to improving performance at the Santa Rita mine in 2010, Argonaut Securities analyst Troy Irvin said, “…the improved plant recoveries demonstrate that the ramp-up challenges presented by the transitional ore can be overcome, with the longer-term prize intact, that is, a low-cost, long-life, large disseminated nickel sulphide asset.” While BMO Capital Markets analyst David Radclyffe was a little less optimistic, saying that Mirabela’s improved operational performance was encouraging but that consistency really needs to be demonstrated over several quarters.

4. Rathdowney Resources Ltd. (TSXV:RTH)

Are we on the cusp of a zinc shortage? Around the world, almost 2.4 million tonnes per year of zinc mine production will close between 2011 and 2016. The Skorpion mine in Namibia, the Tara and Lisheen mines in Ireland, the Perseverance and Brunswick mines in Canada and the Cerro Lindo operation in Peru, and several others, are soon to be exhausted and closed. With increasing demand projected by many industry experts, some think the zinc market profile may become very tight, particularly from 2012-2016.

Hunter Dickinson (HDI), the largest private mining group in Canada, shares that opinion. HDI, based in Vancouver, is a diverse operation with experience around the world. Over its quarter-century of existence the group has explored for mines, developed them, and has gained expertise in project engineering, project financing and partnering.

In 2007 HDI subtly shifted its corporate development strategy. The new strategy focused on building and maintaining a value-added interest in a portfolio of mineral companies. After the briefest of pauses during the economic downturn, the strategy was fully implemented last year. From the top down, Hunter Dickinson is bullish on base metals. HDI President & CEO Ronald Thiessen recently noted, “While many continue to temper optimistic views on the global economy with a sense of caution, it is hard to argue that copper and other base metal commodity prices are strengthening at a surprisingly fast rate – exceeding predictions of pundits and investors alike.”

HDI now has five companies under management, including a 30% interest in Heatherdale Resources (TSXV: HTR); a 23% interest in Curis Resources (TSXV: CUV); a 41% interest in Northcliff Resources (private); a 41% interest in Constantia Resources (private); and, an 11% interest in Rathdowney Resources. In 2007 Hunter Dickinson invested $7 million privately in Rathdowney which, at the time, had secured a large prospective lead-zinc land package in Ireland.

When the economic crisis hit in 2008, Rathdowney’s management team realized that a pure exploration play would likely not attract much attention from the investment community. Instead, the company set out to secure a more senior project. Already established in Europe, Rathdowney turned its attention to Poland, and its well know Upper Silesian lead-zinc bearing zone. The company was able to secure in mid-2010, after considerable effort over a two year period, the concessions for an advanced stage project with substantial historical resources of lead and zinc from the Polish government.

On March 17, 2011 Rathdowney completed its reverse takeover of Coreland Capital, a shell company (CPC) listed on the TSX Venture Exchange. Concurrent with the takeover and in association with HDI, Rathdowney raised just over $34 million privately at $1.00 per share to develop their projects. The company has drill targets ready in Ireland and a work program established in Poland to maximize conversion of historical resources into NI 43-101 compliance. MiningFeeds.com connected with Rathdowney President & CEO John Barry from his office in Ireland to find out more about their projects – CLICK HERE – for the exclusive interview.

5. Western Copper Corporation (TSX:WRN)

When, on April 25th, Barrick announced an all cash offer of $8.15 for Equinox Minerals many, including Barrick’s shareholders, were more than surprised. In the two trading days following the announcement Barrick’s shares lost over five dollars, falling from $53 to $47.75, an amount that equaled $5.3 billion in valuation. Investors and analysts alike have expressed concerns about the Equinox acquisition. Some fear that adding copper will dilute the premium investors pay for gold stocks. Analyst David Christie at Scotia Capital, however, believes that Barrick will not lose its premium if the deal goes through. “We do not view 30 percent non-precious metals as an issue for a gold producer to retain its gold multiple.” The market still remains nervous since Equinox, on the surface, is primarily a pure copper deal and, if completed, the acquisition doubles Barrick’s anuually copper production to about 600 million pounds.

So why is the world’s biggest gold mining company interested in copper? Barrick cited scarcity of opportunities of this size and quality (Equinox’s Lumwana Copper mine contains 4.5 billion pounds of copper reserves and another 5.5 billion pounds of inferred copper resources); and, the acquisition maintains the company’s gold exposure per share when factoring in Equinox’s Jabal Sayid copper-gold project which has estimated grades of 2.3% copper and 0.3 grams per tonne gold.

Apparently size does matter in mining. One company with a big asset is Western Copper with its Casino deposit in the Yukon Territories. The Casino deposit hosts 4.7 billion pounds of copper (M + I) and another 5.2 billion pounds of inferred copper resource; 7.9 million ounces of gold (M + I) and another 8.7 million ounces of inferred gold resource; along with substantial amounts of silver and molybdenum. In addition to the Casino Project, Western Copper has two other projects of merit in the Yukon and one in British Columbia.

CIBC World Markets analyst Ian Parkinson did an extensive review of TSX & TSX-V listed junior copper producers looking at 160 companies and more than 200 projects. The aim was to determine which players are most likely to draw the attention of large mining companies from China, India, Brazil and other developing economies. Mr. Parkinson ranked Western Copper 3rd on his list citing, “It holds significant gold, copper and molybdenum resources and reserves”.

F. Dale Corman, Western Copper’s chief executive officer is banging the same big drum. In an article by Bloomberg Businessweek last September Mr. Corman stated, “There’s a limited number of large deposits that are in the range the big mining companies are interested in. I expect to see a lot of people walking through our doors.”

Well the world’s largest gold producer certainly walked through Equinox’s door – more accurately crashed through it – some believe this is only the start of merger and acquisitions activity in 2011 and that this year will be another record-setting year for mining M&A.

For 10 Base Metal Stocks to Watch in 2011 – Part 3 – CLICK HERE.

Iron is the most commonly used of all metals and accounts for the majority (est. 95%) of the world’s total annual metal production. China continues to be the main importer of the mineral and driver of global demand. China’s daily crude steel output rose to a record 1.945 million tonnes in mid-March, as steel mills banked on a pickup in demand when construction activity generally picks-up in April. In July last year India banned iron ore exports from Karnataka state, which supplies 1/4 of India’s iron ore, in a move to preserve supplies for domestic steelmakers. Recently, however, the move was recently overturned by India’s top court. Brazil, Australia and India are the world’s three biggest iron ore exporting nations.

Mining and steel analyst Rafael Weber, from brokerage firm Geraçao Futuro in Brazil, believes iron ore prices could increase by approximately 22% in the first half of 2011. He noted that Brazilian miner Vale, the world’s largest iron ore producer and exporter, has already set a price hike of 7-8% for the first quarter. The world’s top three iron ore miners: Vale, BHP Billiton and Rio Tinto, switched to a quarterly iron pricing system in 2010 replacing the benchmark arrangement in which iron prices were negotiated each year. Higher spot iron ore prices this February, which recently approached the record levels set in 2008 (just over $200 per tonne), have prompted some miners including BHP Billiton to advocate a monthly pricing scheme. With increasing market transparency and increasing prices, 2011 is certainly shaping up to be another interesting year for iron producers.

6. Labrador Iron Mines Holdings Limited (TSX:LIM)

Along with having the longest name on our list, Labrador Iron Mines is set to become Canada’s next iron miner. The company has a collection of iron ore properties in western Labrador and North-Eastern Quebec within close geographical proximity. The properties collectively contain approximately 150 million tonnes of iron ore resources (historical estimate of which 40 million tonnes has now received NI 43-101 compliant status) grading between 56% and 58% iron. The ore will be processed for shipping (crushing-screening-washing) at the companies centralized Silver Yard plant which is currently in development.

On April 26th, 2011 the company completed a $110 million offering ($12.50 per common share and $15 per flow-through share). The intended use of the financing is to upgrade and expand the Silver Yard plant, payments under the company’s rail transportation agreements, exploration and development and general working capital. When talking with MiningFeeds.com, analyst Geordie Mark notes, “Labrador Iron Mines is set to become Canada’s next iron ore producer coming into production this month. The company intends to deploy the cash from its recent financing and cash-flow from operations to expand output over the next few years so the timing looks perfect to take advantage of elevated iron ore prices.” The Haywood analyst has a 12 month price target of $17.70 per share. His firm, Haywood Securities (or an Affiliate), managed or co-managed or participated as selling group in a public offering of securities for Labrador Iron Mines in the past 12 months. Shares of Labrador Iron Mines have been recently trading between $12.50 and $13.50 per share.

Consolidated Thompson Iron Mines (TSX: CLM) was the last Canadian iron ore company to reach production. On January 11th, 2011 the company announced that it was to be acquired by Cliffs Natural Resources for $17.25 per share in cash representing a transaction value of approximately $4.9 billion.

7. Copper Mountain Mining Corp. (TSX:CUM)

What does an experimental electronic music band from the UK called The Shamen have to do with Copper Mountain? Admittedly, that is a very difficult question. The Shamen’s first (and only) top 40 hit in the U.S. was released during the summer of 1991 and could very well be the perfect theme song for Copper Mountain. That song was “Move Any Mountain” and that’s what Copper Mountain is about to do – all the way to Japan.

The company owns 75% of the Copper Mountain mine, and their Japanese partner, Mitsubishi Materials Corporation, owns the other 25%. The 18,000 acre mine site is located 20 km south of the town of Princeton in southern British Columbia. The mine has a resource of approximately 5 billion pounds of copper and the project is fully financed and nearing completion. Pre production mining activities are underway and the mine is set to enter production next month to produce approximately 100 million pounds of copper each year. Shares of Copper Mountain have performed well over the past 12 months moving from $2.70 last May to $6.78 per share today.

The mine will utilize conventional crushing, grinding and flotation processes and equipment. Once the copper concentrate is produced, it will be shipped to one of Mitsubishi Materials’ existing copper smelters in Japan. First, by rail to the port of Vancouver, and then by ship across the Pacific Ocean. B.C. Minister of Transportation and infrastructure Shirley Bond recently stated, “This really shows how the Pacific Gateway is the best transportation route for Asian businesses.” And, “Mitsubishi Materials Corporation invests in the B.C. Copper Mountain Mine to get the copper concentrate they need, knowing that the best way to ship it is through the Port of Vancouver.”

MiningFeeds.com connected with Jim O’Rourke, Copper Mountain’s President & CEO and 2005 recipient of the Edgar A. Scholz Medal for Excellence In Mine Development in British Columbia and the Yukon to find out more about the company as it nears production. For the exclusive interview – CLICK HERE.

For 10 Base Metal Stocks to Watch in 2011 – Part 4 – CLICK HERE.

8. Invernia Inc. (TSX:IVW)

April showers do not always bring May flowers. On April 5th, 2011 Ivernia’s shares were halted and the company announced that its wholly owned subsidiary, Magellan Metals, discovered mud on the bottom of a shipping container that was transported from the company’s Magellan mine to the Port of Fremantle. Mud on the bottom of a shipping container doesn’t sound like such a big deal – right?

Not so. The results of isotope testing found the presence of lead. And confirmed there was a high probability that the lead came from the Magellan mine. The company did suggest that the source of the lead was likely not from the bagged lead carbonate concentrate within the shipping container. However, during the transport process, shipping containers rest on the ground both at the Magellan mine site and at a rail yard in Leonora. Recent heavy rainfall in Australia has produced wet ground conditions at both locations and is considered to be the likely source of mud.

The company regarded the discovery of Magellan lead in the mud sample as unacceptable and initiated a full investigation and steps to cleanup the lead-bearing mud, regardless of its origin. Magellan Metals immediately informed Western Australia’s Office of the Environmental Protection Authority (OEPA) and voluntarily stopped the transport of lead concentrate from the mine site and halt operations to undertake a comprehensive end-to-end review of all its activities related to the Magellan mine.

Ivenria’s shares lost six and a half cents on the day of the announcement to close at $0.325 and have since fallen to $0.24 on the heels of more troubling news. On April 7th Invernia announced it was putting the mine site under full care and maintenance and could not provide any further guidance on when the company will restart operations at the Magellan mine.

Lead is toxic to everyone, but unborn babies and young children are at greatest risk for health problems from lead poisoning – their smaller, growing bodies make them more susceptible to absorbing and retaining lead. It is distributed throughout the body just like helpful minerals such as iron, calcium, and zinc. Most ingested lead ends up in the bone where it can interfere with the production of blood cells and the absorption of calcium that bones need to grow. Symptoms are widespread and treatment is with a medication called a chelating agent, which chemically binds with lead, making it easier for the body to get rid of it naturally. Contaminated soil is of particular concern because it can result in lead dust in the air.

In 2008 it was originally reported that a Queensland metal mine owned by mining giant Xstrata could face lawsuits over lead poisoning. Xstrata’s Mount Isa mine was cited as Australia’s biggest emitter of several heavy metals and that testing showed one tenth of local children had high levels of lead in their blood. On February, 20th, 2011 a $1 million lawsuit was launched on behalf of a 6 year old boy who is reportedly suffering from “severe lead poisoning”. If successful, the case may open the floodgates for additional lawsuits from other children in the area who are also allegedly suffering from lead poisoning.

For shareholders of Invernia the news of the mystery lead-containing mud and subsequent shutdown was undoubtedly very disappointing since the death of thousands of birds from lead poisoning at the port of Esperance in March 2007 resulted in a two and a half year halt in exports from the Magellan mine. Not to mention Invernia just delivered a record year in 2010 resulting in revenue of $100.8-million compared with $25.2-million in 2009 and net income of $17.1-million (eight cents per common share) compared with a net loss of $3.3-million in 2009.

9. Copper Fox Metals Inc. (TSXV:CUU)

You’ve probably heard or peak oil but have you heard of peak copper? The difference between peak oil and peak copper is that copper is recycled and reused. It has been estimated that at least 80% of all copper ever mined is still available above ground. Peak copper, in theory, is the point in time when the maximum global copper production rate is reached. Since copper is a finite resource, at some point in the future new production from the earth will diminish. When this will occur is very much a matter under dispute but, lately, the debate over peak copper has been adding fuel to the copper frenzy. One Canadian listed company that plans on adding to the global supply of copper is Copper Fox Metals.

Copper Fox listed on the TSX Venture Exchange in June 2004 to explore the potential of the Schaft Creek deposit in Northern British Columbia, Canada. Schaft Creek deposit is an undeveloped copper-gold-molybdenum-silver that was owned by Teck-Cominico (now Teck Resources) that was optioned by Guillermo Salazar, the company’s founding president and CEO, in 2002. Pursuant to the option agreement, Copper Fox can earn a 78% interest (23.4 % of the deposit) in Liard Copper Mines Limited by completing a “positive” feasibility study. Teck maintains certain earn-back rights on receipt of a “positive” bankable feasibility study.

The recent approval of the Northwest Power Line by B.C.’s Provincial government was always considered a key component of the projects viability. BC Hydro performed technical studies on the project for years and advocated the new line would provide a reliable supply of clean power to potential industrial developments in the area. But, as is often the case with such mega-projects, environmental opponents were vocal.

Finally, on February 23rd, 2011 the BC Environmental Assessment Office announced that the Northwest Transmission Line was finally granted an Environmental Assessment Certificate. Copper Fox put out a press release applauding the decision and the company’s shares made a dramatic move from $.96 cents on February 11th to $2.70 a few months later. Shares of Copper Fox have subsequently pulled back from their April highs to the $2.00 range. MiningFeeds.com recently connected with Copper Fox boss Elmer Stewart to discuss the significance of the Northwest Power Line and the company’s future – CLICK HERE – for the exclusive interview.

10. First Quantum Minerals Ltd. (TSX:FM)

Winston Churchill once said, “Those that fail to learn from history, are doomed to repeat it.” Perhaps First Quantum’s Chairman and CEO, Philip Pascall is a student of Mr. Churchill.

On April 29th, First Quantum held a groundbreaking ceremony for their Trident project in Kalumbila, Northwestern Province, Zambia. The ceremony was attended by Zambia’s President Rupiah Banda, traditional leaders led by Senior Chief Musele, government officials, and local residents. In his speech, Mr. Pascall reaffirmed First Quantum’s long-term commitment to the Government and people of Zambia and the project’s positive impact to the country’s economy through the creation of more than 2,000 direct jobs and by providing a catalyst for large-scale infrastructure development in the region.

Zambian President Banda was also given the floor and during his speech highlighted First Quantum’s status as the country’s largest single taxpayer, its investment in several social projects, and the positive impact of the mining industry on the country’s economy. President Banda also reiterated his government’s commitment to making Zambia a preferred destination for capital investments by international investors.

This ceremony marks the one year anniversary of the Congolese Supreme Court decision to annul First Quantum’s rights to two copper mines (Frontier and Lonshi mines) in the south of the country. Less than a year earlier, in 2009, the Government of the Democratic Republic of Congo closed First Quantum’s Kingamyambo Musonoi Tailings mining project. First Quantum is seeking international arbitration on these disputes that put, collectively, $1 billion of investments are under legal action.

Despite the company’s issues in the Congo, on January 25th, 2011, First Quantum provided a development update and expects to hit production of 470,000 tonnes of copper per year by 2015 from the addition of new projects like Trident in Zambia. Following the production update, BMO analyst David Radclyffe called the company “one of the strongest mid-term growth stories in copper, albeit this assumes delivery of one new project each year.” In a TD client note, analyst Greg Barnes referred to First Quantum as “the next copper major” stating the company’s “copper growth profile is one of the most attractive in the global mining sector – both for investors and potential acquirers.” Shares of First Quantum closed today, Friday, May 6th at $123.72 a share.

For 10 Base Metal Stocks to Watch in 2011 – Part 1 – CLICK HERE.

Today, after twenty-four hours of speculation, Equinox Minerals launched a hostile bid for Lundin Mining. The move temporarily leaves Symterra blowing in the wind. What is Symterra you ask? That is the proposed name of a new entity resulting from the friendly merger of Lundin Mining and Inmet Mining – a transaction valued at $9 billion.

Yesterday, the Globe and Mail reported that an unsolicited offer was in the works. Equinox then requested its shares be halted on the Australian Stock Exchange before that market opened on Monday, “pending the release of an announcement by the company”. This morning, Lundin Mining confirmed that Equinox Minerals had indeed made an offer to acquire Lundin for approximately $4.8-billion in cash and shares of Equinox. The consideration per common share of Lundin Mining was offered at $8.10 in cash or 1.2903 shares of Equinox plus one cent for each Lundin Mining common share. The offer would be subject to a proration maximum cash consideration of approximately $2.4-billion and maximum Equinox share consideration of 380 million.

The rival bid effectively puts both Lundin and Inmet in play and has the potential of sparking a memorable takeover battle in the base metals sector. The bid from Equinox comes just two weeks before Lundin and Inmet shareholders are set to vote on their proposed deal.

A takeover offer from Equinox is likely to renew the debate concerning foreign corporate takeovers of Canadian-based mining companies. In mid-November 2010 BHP Billiton announced it had withdrawn its $38.6 billion unsolicited takeover offer for the Potash Corporation of Saskatchewan, the world’s biggest producers of a crucial fertilizer ingredient, after the Canadian government stone-walled the potential deal. Both Potash and the Saskatchewan government fiercely lobbied Canada’s Conservative government to block the deal, citing what amounted to national security concerns. Potash produces about half of the world’s supply of the eponymous material and generates significant revenue for the Saskatchewan government.

On November 3, 2010 when the Canadian federal government formally scuttled the Potash deal for not representing a “net benefit” for Canada. The decision was made under the Investment Canada Act, which vests authority under the industry minister and requires only that companies show a “net benefit” to Canada – a somewhat subjective assessment. Industry Minister Tony Clement gave the Australian mining giant a 30 day window to restate its case and make any additional representations to Ottawa but BHP Billiton elected to terminate the offer and forgo the red tape.

With the Equinox offer today yet another Australian company is taking a run at a high profile Canadian mining company. Investors clearly think this takeover has a better chance of succeeding. Shares of Lundin Mining closed at $7.65 today, up $1.20, or nearly nineteen percent.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |