Galway Metals (GWM.V, GAYMF) is a Canadian exploration stock with two prospective projects located in strategic locations. Fundamentally, some things stand out.

1. Insiders

Over 30% of outstanding shares are in the hands of management and insiders. High quality management as both CEO and Chief Geo come from Kirkland Lake Gold (KL.TO) where they also held management positions. Another reputable insider is Wesdome’s (WDO.TO) CEO Duncan Middlemiss, who has an advising role at Galway Metals. Connections like these could be important in a later stage should

exploration continue in the current direction.

In the past year, 5 insiders have been buying their own stock, of which CEO Robert Hinchcliffe invested the highest amount. Through 2018, he bought $285,000 worth of stock in the open market and another $100,000 in a private placement. Other insiders put in between $25,000 and $88,000 of their own money into Galway Metals.

Insiders are dedicated as well. When looking at their personal holdings, the biggest part of this is held in GWM shares. Data like this can be retrieved on marketscreener.com. Management in this business usually has seats on more than one company’s board, which means they hold more than just one stock. Therefore, it’s interesting to see the weight of these. Allocations at Galway Metals show conviction: CEO 89%, VP 73%

and Chief Geo 47%.

2. History

Galway Metals was spun out of the Galway Resources takeover by AUX in 2012. At the time, Galway Resources was sold for $340M. Management is largely the same since then, so they’re experienced in growing an exploration stage company to one that’s prepared for production. Galway Resources (GWY) shareholders received a 47% premium in that deal.

3. Projects

Galway Metals has 2 projects in Eastern Canada in mine friendly jurisdictions in areas where infrastructure such as roads, railways and mills are closeby. Both projects have an existing resource for both gold and industrial metals. One million ounces of gold have been mapped to date and if we add the other metals, there’s 1.8 million gold equivalent ounces. These past years there has been a resource upgrade yearly, and this year as well, they will upgrade their existing resources on both projects

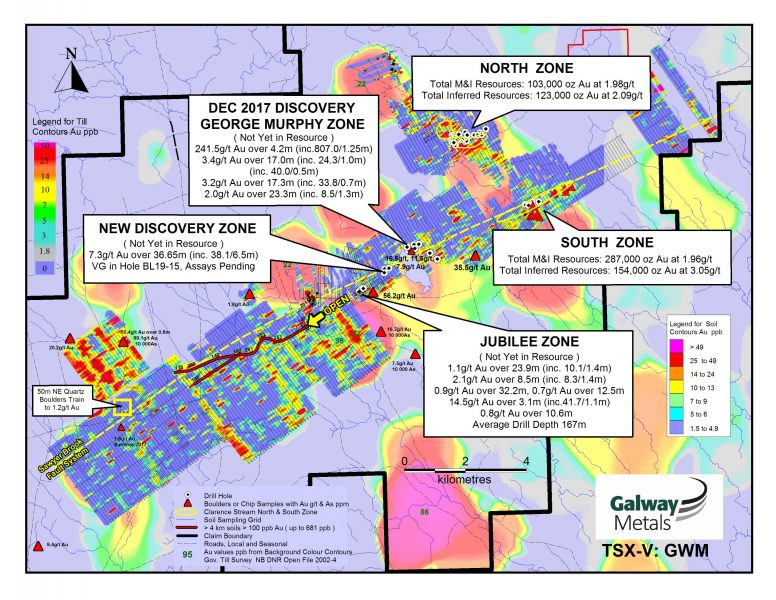

Clarence Stream

Located in mining friendly New Brunswick and in the proximity of a processing mill and (rail)roads nearby. Management hints that this project can represent a new gold district in Canada. Findings to date continue to prove this out: This project has 5 discovered zones thus

far on the main NE-SW trend with high possibility for new discoveries going by soil anomalies. Galway just announced assays from their fifth and new discovered zone: 7.3g/t over 36.7m (38.1g/t over 6.5m). A 50m stepout has been drilled which intersected visual gold twice. Results from this are pending.

This new discovery is in the middle of two known zones (Jubilee and George Murphy) that are 2km apart. Galway controls 65km of this main NE-SW trend and management believes this shares the same structure and has similar geology as Marathon’s (MOZ.TO) Valentine Lake project. Only 5km have been drilled and all zones are open in every direction. Wide mineralization at shallow depths with grades which would make this suitable for open pit mining.

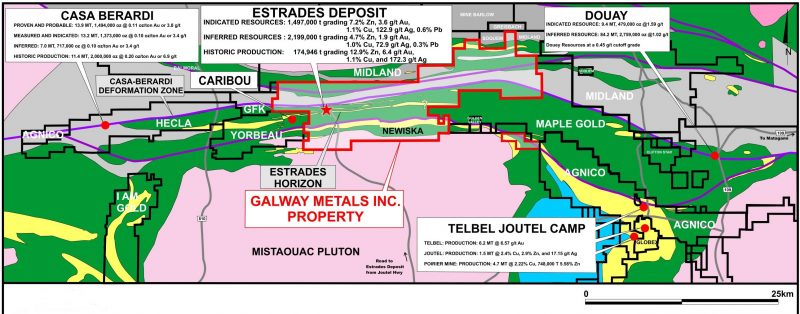

Estrades

Polymetallic project that saw production in 1990-1991:174,946 tonnes grading 6.4 g/t Au, 172.3 g/t Ag, 12.9% Zn and 1.1% Cu. Previous owner stopped production when metals prices dropped in 1991. Since then this former mine has been dormant for over 25 years. Located in mining friendly Québec with multiple deposits, active and historic mines in

the proximity. 31km of strike hosting 3 mineralized trends which hold a resource that’s high in Zinc (20.75% ZnEq) and Gold (11.28g/t AuEq).

Just like the Clarence Stream project, this is currently being drilled so news from here should flow in coming weeks.

4. Cashed up

All that drilling costs money. Therefore, it’s interesting to know that Galway has about $7M in the bank after a recently closed private placement (in which 4 insiders participated), which means they can continue this aggressive exploration. Galway Metals doesn’t have any debt. Also of importance is that chief geo and vice president bought warrants with an execution price of $0.50, which -when executed- will add $750,000 to the treasury.

5. Catalysts 2019

Two catalysts this year for a revaluation. Catalyst # 1: Exploration success and new discoveries on Clarence Stream and Estrades. On Clarence stream, investors have a couple of pending results to look

forward to from drill cores that showed visual gold as well as future step-out holes from current zones. Catalyst # 2: Resource upgrade 2019 including the new zones. Management pointed at a resource upgrade this year that will – for the first time- include 2 new zones at Clarence Stream.

6. Comparables and valuation

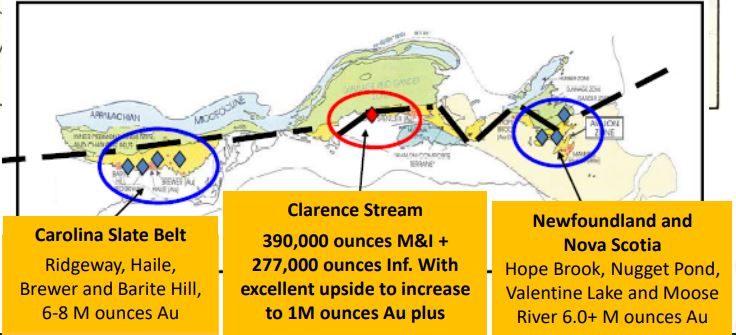

When looking at other Eastern Canadian companies that share this continent scale trend, it’s easy to see their Clarence Stream project is favourably located in between known multi million ounce gold camps.

Similarities with Oceanagold’s Haile mine, which is an open pit mine that shares shallow depth in combination with high grades. Another similar case is Atlantic Gold over in Nova Scotia. This has the same

widespread gold occurrences on their property and built a central processing facility that’s currently being fed by the surrounding deposits.

Galway is not yet at this stage and management may not have the intention to mine it themselves. Just going by similar geological features and challenges, it’s positive to see nearby succeeded projects.

As valuation goes, when looking at the only metric we can currently apply – which is the enterprise value on a proven gold ounce basis- we’re sitting at $17.4/oz whereas this sector’s (pre feasibility) average is $52/oz. Noteworthy that this number is based on the current resource, that only holds 2 of the 5 zones at Clarence Stream.

7. In Closing

As said in the intro, Galway has a lot going for it. Two catalysts this year that will continue to get fed from multiple fronts. Galway has a rather tight share float (107M) and they don’t need to collect funds any

time soon, meaning that their share price will benefit with a leverage effect when exploration continues to deliver. Management is experienced, respected, committed and on the buying side. Not to be taken for granted in any sector. Eastern Canadian gold deposits are on the rise and going by the fundamentals there’s good potential that this too will turn out to be a multi million ounce deposit, eyed by producing mining companies. Going by the EV/oz metric, there should be plenty of room for upside.

Jonas De Roose

February 22, 2019

Author Jonas De Roose is a Belgian retail investor in precious and base metals stocks with a drive for research and learning. He has a background in business development and marketing. He owns shares in Galway Metals and his article is not intended as investment advice. This article is based on his findings and based on his personal opinion. If you have suggestions regarding this company feel free to contact him at jonasderoose@hotmail.com.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |