China’s output data has put some pep in the step of iron ore prices as low inventory levels around the world could potentially contribute to a supply dearth.

The most-traded iron ore contract by volume for September delivery was up 5.5% to $195.26 per tonne at one point on the Dalian Commodity Exchange. As construction ramps up on projects around the world, steel demand is likely to keep rising over the coming months.

The demand could push iron ore prices higher for the foreseeable future until a more balanced supply is established and inventories are refilled. Analysts with Huatai Future wrote in a note that, “Steel consumption is still at seasonal peak in the short term…mills are actively producing, driven by high profits, which support raw materials.”

China’s reopening from the pandemic has been a significant driver of both supply and demand, and the country’s output hit a record high even though the government has pledged to curb annual production in a bid to reduce pollution and keep costs high for raw materials. The global steel output continues to inch up, rising to 97.9 million tonnes. This crossed month and daily run-rate records.

Analysts at Morgan Stanley agree that China will continue to drive the market in the short term, writing, “As China’s steel production still continues to expand, its steel margins remain elevated and seaborne iron ore supply remains constrained, we think that the iron ore price can stay around the current level through 2Q, but is likely to remain highly volatile.”

5% daily moves may not be a regular occurrence, but risks loom as demand from Latin America remains low, and supply from Brazil could pick up in the coming months to supply local needs. Global iron production growth is expected to accelerate this year with Brazil driving much of that growth.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

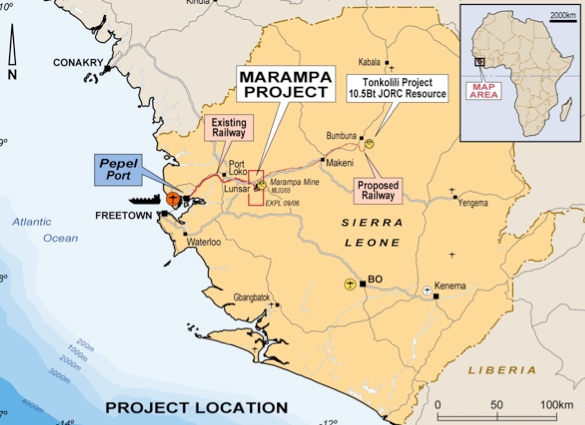

I wrote last week about ongoing concerns around the management of the Marampa mine, a massive iron-ore deposit in East Sierra Leone. After Gerald Metals failed to restart production since taking ownership of the mine in 2016 through their ‘SL Mining’ subsidiary, fears that the company’s creditors would cut their losses began to circulate. Now, it seems the situation is far worse than first thought. Troubling lawsuits, fleeing investors and some deep-seated concerns around the corporate social responsibility obligations may leave Gerald Metals’ top team of Craig Dean, Brendan Lynch, Pat Crepeault and Gary Lerner exposed as we head towards the new year.

Last week the Government of Sierra Leone, which had been dissolved for the Christmas break since early December, rushed through the ratification of legislation that renewed Gerald Metals’ mining licence at Marampa [1]. After weeks of scrutiny and claims that Gerald Metals were days from having their licence revoked, the news will have come as a great relief to the company’s management team. However, this has proven to be something of a false dawn.

Since my last article for Mining Feeds, reports have now reached me that the Revolving Credit Facility, on which Gerald Metals relies to run its Marampa project, is undersubscribed.

In 2014, the last time the Revolving Credit Facility was renewed, appetite from investors was such that the facility had to be upsized by $50m to account for interest [2]. That confidence is now in short supply. Earlier this year, Gerald’s equity partners, Pengxin International Mining Co., jumped ship, which was worrying enough [3]. But now that several lead investors in the RCF, two Lloyds of London syndicates and a pair of Israeli and French banks, have completely pulled out of renewing their credit lines, serious questions must not only be asked over Gerald Metals’ continuing ability to guide Marampa through care and maintenance; they must be asked of their credit worthiness full stop.

So, what has gone so wrong for Gerald Metals, a veteran commodities house with 50 uneventful and profitable years of business, in their dealings in Sierra Leone?

For a start, investors know more than anyone that when it comes to a faltering business, the fish rots from the head. It is easy to point the finger at the disastrous iron ore price crash that shook the global industry in 2014; but whilst plenty of firms were rattled by the drop, very few are still yet to recover. Allegations of inexperience have been levelled at Craig Dean, the CEO of Gerald Metals, since he unexpectedly took the top job, joining the firm from Deloitte in 2013. Since then, it hasn’t been the easiest of tenures for Craig Dean: between fighting allegations of sexual harassment from his former General Counsel, Roxanne Khazarian [4], and being sued by Australian commodities giant, Cape Lambert Resources, for breach of contract [5], it’s hardly surprising the embattled CEO hasn’t kept his eye on the ball.

But in truth, the issues go far beyond management. Anger on the ground in Lunsar has grown since Gerald Metals has failed to make good on pledges to support local community projects around the Marampa site. Tensions were also raised last month when Ibrahim Alusine Kamara, an investigative journalist with the Sierra Express who had been routinely reporting on management issues at Marampa, ended up in hospital after a brutal assault.

With a Presidential election around the corner in Sierra Leone, foreign investors will be keeping a very close eye on things, paying particular attention to the current business environment. Sierra Leone relies on a vibrant mining sector both as its economic base and golden ticket to the global marketplace. So, the Bai Koroma administration must make sure that the sorts of issues we are seeing at Marampa are identified and addressed before investor confidence is damaged. After all, the fish rots from the head in government too.

[1] http://www.miningglobal.com/

ANGLO American’s (LSE:AAL) recent corporate maneouvres have really caught the eye, especially the sale of its 24.5% stake in Anglo American Sur, its Chile base metals company, to Mitsubishi.

Analysts have described it as ‘fancy footwork’ and ‘corporate theater’; another, in martial terms as Anglo having ‘outflanked’ Codelco. Codelco is Chile’s state-owned mining company that last month announced its intention to exercise its option agreement over Anglo American Sur in January.

For me, I can only wonder, again, at the power of the team. In rejecting Xstrata’s (LSE:XTA) merger of equals proposal two years ago, Anglo CEO Cynthia Carroll not only saved her job but got herself a steely board of directors.

As a colleague of mine once said, the softest part of Sir John Parker, the industrialist drafted into Anglo at the time of the Xstrata bid, is his tooth enamel. The swiftness of the Mitsubishi move has the paws of a sly fox all over it. I’d love to know how this plan was hatched, when, and by whom.

In any event, Anglo has at a stroke achieved a few things. It has increased the valuation of 100% of Anglo American Sur 10% to $22 billion against the $19.9 billion value attached to the company by Codelco (and financier, Mitsui).

Secondly, Anglo seems confident it has reduced the amount of the stake over which Codelco has its lower value option agreement. So if Codelco exercises its option, the company will be shared as follows: Anglo American (51%), Mitsubishi (24.5%) and Codelco (24.5%).

Thirdly, Anglo also has the optionality of dispensing the remaining 24.5% Codelco still has rights over which the government can only do in January. An Anglo spokesperson confirmed the group could have sold 50% of Anglo Sur if it had wanted.

Assuming Anglo doesn’t do this, and waits for Codelco to exercise its option, it will stand to bag some $8.4 billion (before capital gains tax on the Mitsubishi sale which is a whopping $1 billion). This fourth element of Anglo’s coup raises the question again: what will Anglo do with the cash?

One analyst, who asked not to be named, said there would be enough cash left over to build a balance sheet robust enough to buy out the Oppenheimer family’s stake in De Beers – the other corporate manoeuvre which earned Carroll kudos earlier this month – and take out Kumba Iron Ore minority shareholders, equal to 35% of total shares in issue valued at some $7 billion.

Shares in Kumba Iron Ore (JSE:KIO) have increased 11.5% since November 1. It’s worth noting that the volatility in iron ore prices didn’t much affect the company given the niche value of its product suggesting the possibility of a takeout might be getting priced into the share, perhaps.

From the article entitled, “Anglo may line up Kumba Iron Ore” by David McKay of Miningmx. Miningmx is a leading online publication providing news, editorial and analysis on the African resources sector. The information provided herein has been provided to MiningFeeds.com by the author and, as such, is subject to our disclaimer: CLICK HERE.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |