Franco-Nevada is a diamond in the mining industry, as a steady and profitable royalty and streaming company. In a world of low yields and interest rates, investors are hard-pressed to find the kind of returns that will make them look at their RRSP with pride. Chasing returns also carries significant risk, which Franco-Nevada controls for by not operating mines, developing projects, or conducting exploration.

Low-Risk, Reponsible Management

The company instead focuses on managing and growing the company’s portfolio and streams, giving them exposure to commodity price optionality and a perpetual discovery option over large areas of profitable and geologically prospective real estate. This low-risk, steady, and high-reward business model is a counterbalance to the hit-and-miss strategies of many other mining companies. The company has limited exposure to many of the risks associated with operating companies because of its capital-light business model. This nimble operation strategy allows it to pivot to new projects, mines, and even supporting the industry when needed. The company engages in exploration efforts as part of advancing a property in advance of taking on an investment. This due diligence is necessary as the company relies on the industry operating responsibly to both reduce risk, and honour the royalty and streaming agreements they make.

By The Numbers

With the stock price sitting at over $109, the company is more expensive than many of its peers, but this is an investment that gives more than it takes, just as it should be. Their portfolio of precious metals like gold, silver, and platinum group metals, oil, gas, and natural gas liquids allows them to give investors a dividend yield of 0.90%. With an operating margin of 28.18% and a return on equity of 5.18%, this is one of the rare mining companies that consistently turns out results investors can be pleased with. With zero debt, and a fully equity-funded balance sheet, not only are the paper stats solid, but the bottom line fundamentals are strong enough to keep buying the stock as it gains.

Their recent announcement of a US$0.26 per share dividend to be paid on March 25th, 2021 to shareholders of record on March 11th, 2021 was welcomed warmly by investors. Analysts are estimating 15% growth for 2021, and as the company gears up to report 4Q2020 earnings on March 10th, investors eagerly await a sign that all is well with this steady performer. Whether 2021 will shape up to be as good a year for Franco-Nevada as 2020 was is still yet to be seen, but with restrictions lifting, business activity picking up, and an optimism in the air, new projects and mines will continue to need the company’s services, bringing more dividends for shareholders quarter after quarter.

Dividends Keep Padding Portfolios

We will continue to watch the dividend payout ratio, as the company must balance paying out less in dividends than it earns; the opposite would make the dividend unstable. Franco-Nevada paid out 74% of its earnings to investors last year, an average level for most businesses, and nothing they need to worry about adjusting. Dividends also used just 27% of the free cash flow it generated, leaving a comfortable margin to continue paying a dividend throughout 2021. As long as earnings don’t drop precipitously, the dividend looks to be stable and is covered by both profit and cash flow.

*This story will be updated on March 10th after the earnings report.

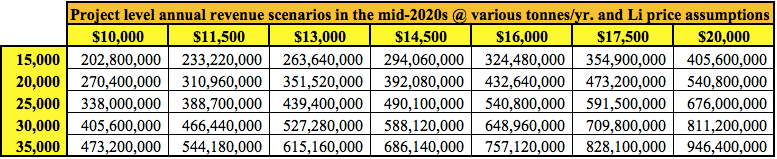

On August 29, Cypress Development Corp. (TSX-V: CYP) / (OTCQB: CYDVF) announced the successful completion of slurry rheology & filtration studies that are an integral part of the Pre-Feasibility Study (PFS) for the Clayton Valley clay-hosted lithium project, located immediately adjacent to Albemarle Corp.’s Silver Peak brine processing facilities in Nevada.

Management believes its U.S. location will become an increasingly valuable attribute. While many junior lithium companies like to name drop “Albemarle” and “Silver Peak,” Cypress owns 100% of one of just a few projects in Nevada that Albemarle might actually be interested in.

More promising results from Cypress’ expert technical team

Back to the latest news…. the outcome was the result of months of testing by laboratories and a detailed review with consultants & equipment vendors. This news represents a major milestone in the project because the results simplify the process flow sheet.

Cypress CEO Dr. Bill Willoughby commented in the press release,

“A critical step for us at Clayton Valley is the separation of solids & liquids. A viable process is dependent upon the ability to separate the process leach solution (PLS) from the leached residue whether by thickeners, filters, or other means. Significant test work has allowed Cypress to identify a commercially viable process, based on filtration, to take the solid-liquid separation from the laboratory benchtop to the operational scale.”

Readers may recall that Cypress released positive results from the first & second phases of its PFS metallurgical program in February & July. Since then, work has continued on other aspects of the PFS, including recovery & concentration of lithium from solution through mechanical evaporation, membrane filtration, and ion-exchange processes.

CEO Willoughby continued,

“The Cypress technical team discovered the Clayton Valley clays behave differently at varying leach conditions. By looking at the electro-kinetic potential of the clays we can select the optimal reagents & equipment. We also know under what conditions the rheology of the slurries becomes a limitation, and can design the flow sheet accordingly. With this new knowledge, we are confident we can simplify a significant portion of the leaching flow sheet.”

Cypress is looking at additional steps to simplify plant design with the goal to further streamline the production process and lower costs. With metallurgical & materials handling studies completed, Cypress expects to publish a PFS during the fourth quarter.

Next major milestone is a PFS in 4th quarter

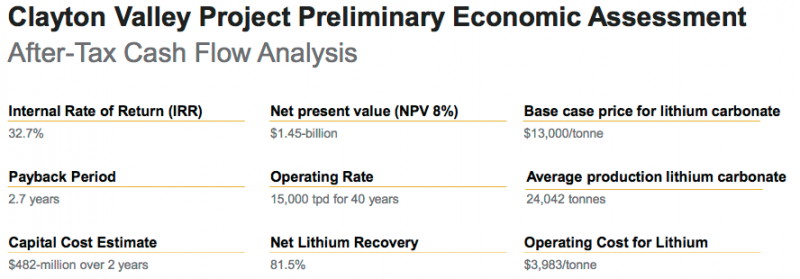

It appears the PFS has been pushed back a few months. After a recent capital raise the company is comfortably funded through delivery of a PFS later this year. Come to think of it, what’s the rush? Investor sentiment remains very weak for lithium, cobalt, vanadium & graphite juniors. As long as Cypress is funded, let them keep carrying out studies to improve the PFS! Below are some highlights from the PEA.

It’s important at this point to reiterate the considerable strength of management, the Board, technical advisers & retained consultants. All of these impressive people and groups are being effectively led by CEO Willoughby, who has a Doctorate in Mining Engineering & Metallurgy from the Univ. of Idaho.

Who on earth could possibly be better to run this show than a PhD in engineering & metallurgy!?! He knows what he’s doing, and he’s a driving force behind the very good results and progress his technical team is delivering.

I asked Dr. Willoughby about last week’s news, he said,

“It’s a major technical problem to separate ultrafine clays particles < 5 microns from a leach solution. Our solution could put us in the forefront of clay-hosted lithium projects globally.”

Demand keeps increasing, supply increasingly uncertain

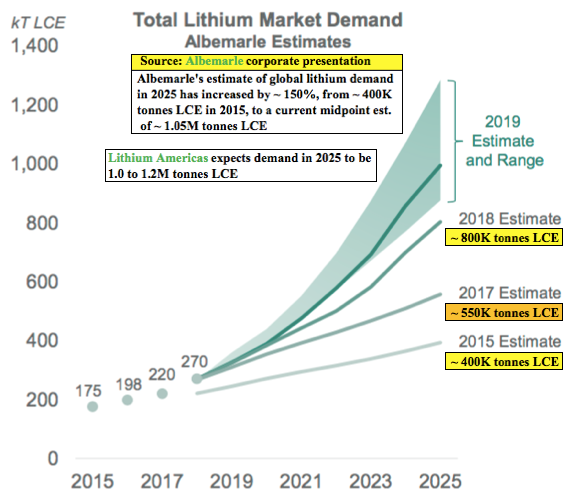

There’s a massive disconnect in the lithium world. For years, demand forecasts have been going up. The demand side of the equation — driven by both energy storage & the electrification of passenger & commercial vehicles — is likely to increase at a Compound Annual Growth Rate (CAGR) of at least 15%, perhaps 20% or more. For example, at a 20% CAGR from Albemarle’s 270K tonne figure in 2018, demand would reach 967K tonnes in 2025.

Albemarle has a particularly good graphic depicting this unmistakable trend. Four years ago they expected ~400K tonnes LCE demand in 2025. Now, Albemarle is forecasting demand of about 1 million tonnes in 2025. Likewise, Lithium Americas is forecasting between 1.0 to 1.2 million tonnes LCE demand in 2025, a range it says comes from industry producers & publicly reported forecasts.

, Finally, Fastmarkets expects LCE demand to grow from ~300K tonnes in 2019 to “at least” 1.1 million tonnes in 2025. So, a lot of forecasts in and around the one million tonne mark, but even if it turns out to be less, I think it will be a major challenge for supply to approach that level in the next six years.

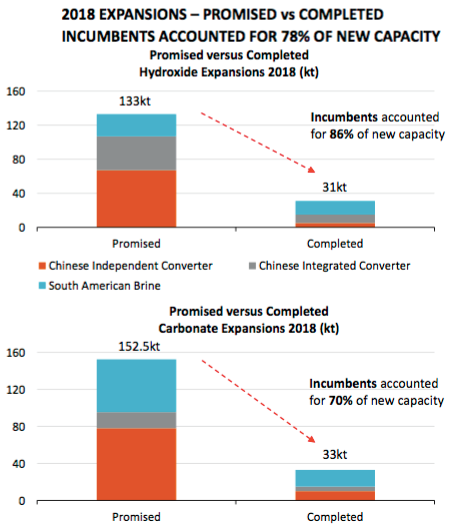

The longer the project delays in Argentina / Chile brine projects, and the more project mishaps like at Nemaska, the more room there is for unconventional projects such as Cypress Development’s Clayton Valley. The market will take every battery-grade tonne of lithium chemicals produced by any company that can supply them. Lithium juniors who can make it across the production finish line will be richly rewarded.

Despite significant fiscal & political challenges in Argentina that could further delay brine projects there, and continued slow movement in project development & production expansions in Chile, unconventional projects are still meaningfully undervalued compared to brine projects.

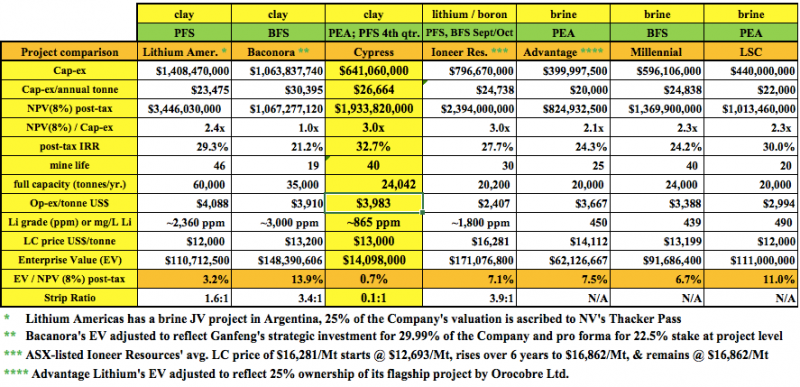

For example, Cypress Development Corp.’s enterprise value (“EV“) is less than 1% of the after-tax NPV found in its PEA. Compare that to the average 8.2% EV/NPV on the chart below. Cypress’ EV/cap-ex ratio of 3.0 times (3.0x) is 40% better than the 2.1x average of the other unconventional projects.

Cypress has the highest after-tax IRR on the chart at 32.7%, compared to an average of 26.1% among the others. And, the company’s cap-ex at C$641 million is 21% lower than the peer average.

Finally, readers should note that the Clayton Valley project has a strip ratio of 0.1 to 1. The other three projects with strip ratios average 3.0 to 1. Cypress has 1/30th the strip ratio of its unconventional peers!

That’s a big reason why the company has attractive op-ex & cap-ex, despite having lower grade Li to work with. Another reason is the mineralogy; the Clayton Valley project’s lithium abundance is hosted in a friendlier clay than that at some of the other projects. Friendlier meaning easier and less costly to liberate the lithium into solution.

The extreme weakness in the vast majority of lithium juniors is actually great news. Great news for any lithium company hopeful that can produce lithium next decade. Great news for investors who may want to average down in their favorite battery metals names.

Brine projects have gone from, “can’t go wrong,” to “can’t fund”

A funny thing happened over the past two years. Brine projects went from no-brainers; (lowest cost, best understood, most reliable) — to the exact opposite. Solar evaporation ponds are getting less and less popular by the week, day, hour! And, unusually rainy weather in the Puna region of Argentina has negatively impacted pond yields. Speaking of Argentina….. well just read the headlines, it’s not pretty.

Chile imposed an onerous sliding-scale royalty on realized lithium prices from production in the Atacama salar. Albemarle’s & SQM’s best, lowest cost lithium brine operations…. the world’s best, may no longer the world’s lowest cost.

Brine projects were sure things and clay-hosted lithium projects were, “maybe in 10 years.” Now? Most brine projects are dead in the water, some of them never coming back to life. Even the top-quartile, most advanced projects are not getting funded. By contrast, the prospects for clay-hosted lithium projects are better than they were two years ago, albeit also difficult to fund.

Investors would be crazy not to consider unconventional assets. Brine projects, with evaporation ponds attached, will themselves be unconventional at some point in the future. The only question is when.

In early August, Glencore announced it was shutting a major cobalt / copper mine in Africa at the end of the year. Three weeks later, cobalt prices are up 30-35%. It might not take that much to get lithium prices back on an upswing. If prices were to improve, juniors like Cypress Development Corp., trading at under 1% of third-party derived after-tax NPVs, could do quite well.

Peter Epstein

September 13, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker / dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this interview was posted, Peter Epstein owned shares of Cypress Development Corp., and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any future events & news, or write about any particular company, sector or topic. [ER] is not an expert in any company, sector or investment topic.

Royal Road Minerals has released results from its recently completed diamond drilling program at the Luna Roja gold project in Nicaragua.

The Luna Roja project is part of a strategic alliance agreement with Hemco Mineros Nicaragua and is located in the highly prospective Golden Triangle region of northeastern Nicaragua. Mines in the region have been operating since the early 1900s.

The first drilling program to be completed on the project returned significant intersections including, 40.65 meters at 2.5 grams per tonne, 23.5 meters at 5.1 grams per tonne, 12.0 meters at 7.1 grams per tonne and 5.5 meters at 12.2 grams per tonne gold.

The drilling results indicate that gold mineralization remains open at depth (down to 150m vertical depth) and management believe that potential exists for further gold mineralization in a downthrown block concealed structurally below mapped marbles and skarnoids to the southeast.

Samples of the drill core have been shipped to Bureau Veritas Vancouver for preliminary metallurgical testing.

“These drilling results are a great start at Luna Roja,” said Royal Road president and CEO Dr. Tim Coughlin. “This discovery is a product of great teamwork and of an exemplary collaboration with our partners, Hemco Mineros Nicaragua. The possibility of extensions to gold mineralization at depth and under faulted cover to the southeast at Luna Roja is enticing. We are also excited to have established our first Designated Project Area and look forward to advancing the Luna Roja project with our partners Hemco Mineros Nicaragua and with the local community, local authorities and other valuable regional stakeholders.”

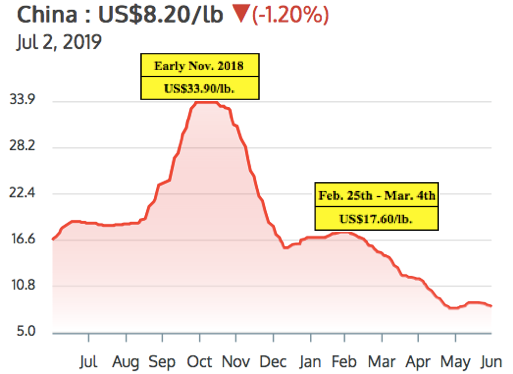

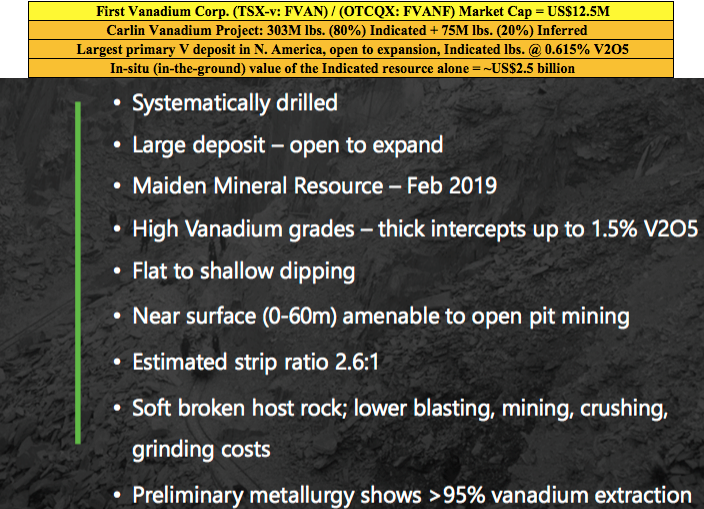

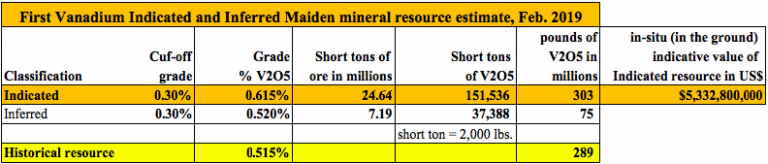

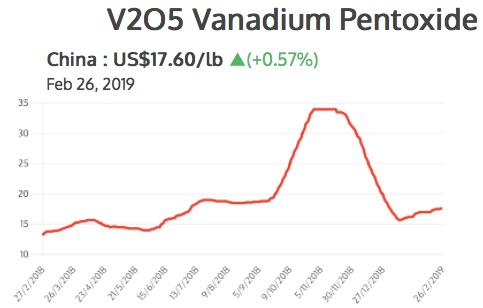

First Vanadium Corp. (TSX-V: FVAN) / (OTCQX: FVANF) has been under pressure, along with hundreds of battery metal juniors and the underlying metals including vanadium, cobalt, lithium. Even vanadium giant Largo Resources is down 61% from its 52-week high. Yet, if one believes in vanadium, it’s hard to ignore First Vanadium’s shares at C$0.44, down 78%! The pro forma Enterprise Value [market cap + debt – cash] is just US$12.8M. The Company has C$1.9M in cash.

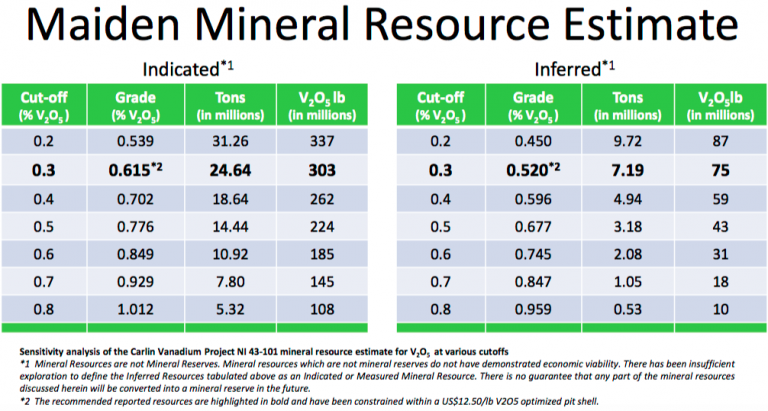

Yet, even at current vanadium pentoxide (“V2O5“) prices, the in-situ value of the Indicated-only portion (303 million pounds) of the Company’s estimated resource is ~US$2.5 billion. Management believes it has the largest high-grade primary vanadium resource in North America.

There has been a lot of weeping and gnashing of teeth over the V2O5 (China) price falling from a 2019 high of US$17.6 to its current US$8.2 per pound. But, as the saying goes, the cure to low prices is…. low prices. Few new projects make sense at today’s levels. I believe that V2O5 (China) between US$10-US$15 per pound might be a sweet spot, good for both producers and end users.

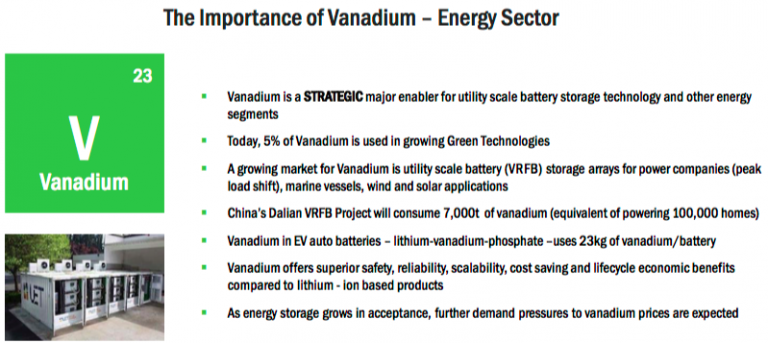

Steel companies can afford to pay higher prices for V2O5, but grid-scale, Vanadium Redox Flow Battery (“VRBs“) Energy Storage Systems (outside of China) might need prices below US$10/lb. to go mainstream. Importantly though, VRB plant costs are coming down. Vincent Sprenkle, a lead researcher at the U.S. Department of Energy’s Pacific Northwest National Laboratory, (“PNNL“) recently said, “VRB costs could be lowered by another 50%.” That would be very bullish for vanadium prices, it would allow for widespread adoption of VRBs even with V2O5 prices above US$10/lb.

First Vanadium has a sizable resource, a good grade, in a great jurisdiction. A Preliminary Economic Assessment (“PEA”) is expected by year end. The following interview of Paul Cowley, P.Geo., President, CEO & Director of First Vanadium, was conducted by phone & email between June 24th & July 2nd.

Please tell us about yourself and your team.

I’m an exploration geologist with 40 years’ experience in the discovery & evaluation of mineral deposits around the world. About half of my career was with a Major, BHP Minerals. I was involved in leading the team in the Canadian arctic that made 4 gold deposit discoveries that generated about 6 million ounces of gold. I also worked at Escondida and BHP’s Ekati diamond mine during their exploration days.

I’m a senior guy, but I’m the youngest of our group. The others have even more years of experience. We have two mining engineers that held mine general manager positions of very significant mines at Majors. We have four metallurgists that have worked for Majors, in senior roles. We have a construction engineer who’s built 20 mines in North & South America, he’s currently building Lundin’s mine in Ecuador.

What do you make of the recent volatility in the vanadium price?

Since early March 2019 the vanadium price has taken an unexpected turn lower. Prices are not responding to the bigger picture demand and supply imbalance. Chinese steel plants did not recharge their vanadium inventories in this period, as many expected they would, putting pressure on traders to liquidate at undercutting prices, but they will have to restock. The U.S.-China trade wars, and some shortfall of enforcement of new Chinese rebar standards, appear to have exacerbated the situation in the short term.

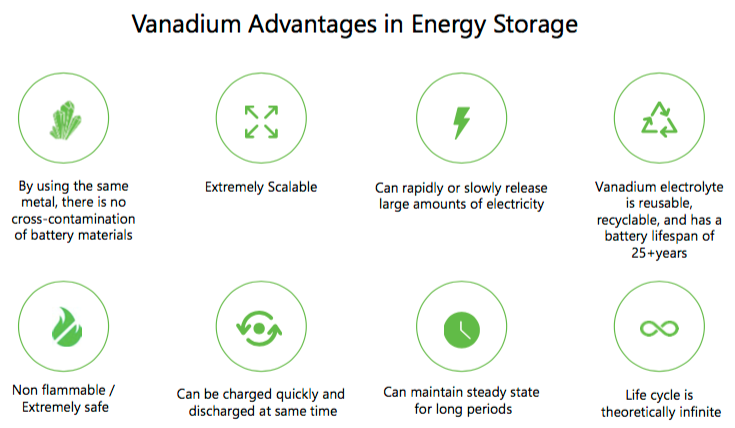

It’s our view that the fundamentals of demand in global steel applications will outstrip supply and should push vanadium prices higher again in the second half of the year, and beyond. Adding to the demand side is the exciting boom in solar & wind projects, all of which require battery storage. This is happening on so many levels around the world that we expect to see the vanadium battery carve out a healthy market share in this expanding renewable space. Some are calling the 2020’s, the Solar Decade.

Please explain the significance of the historical data you recently received, that extended the strike length by 300 meters to the south.

It means more potential than we had expected. From our drilling, the deposit appears to be open to expansion in several areas, but we did not expect the deposit to be open to the south. The newly acquired data demonstrates a 15% strike length increase to the south and it’s still open in that direction. This is exciting news as this data was not included in the resource estimate we put out in February.

You already have a 303 million pound vanadium resource (in-situ value of ~US$2.5 billion) in the Indicated category alone. Does the resource need to get any bigger?

That’s a good question. But it needs to be answered through an economic study. In our view, the resource is sizable. It’s currently the largest, highest-grade primary vanadium resource in North America. Our immediate priority is to demonstrate potential economic viability with what we have, knowing that we believe we could always make it bigger if and when we need to.

Several readers may assume that First Vanadium will need an expensive roaster in its operating flow sheet. What are your latest thoughts?

Not true. The path we are on with our metallurgical flow sheet does not include, or require, a roaster.

Although Nevada is the #1 global mining jurisdiction in the latest Fraser Institute Mining Survey, some complain that it takes a long time to get permits. What does your team expect in this regard?

In general, in the U.S. that is true, but not in Nevada. Nevada has a responsible review and process, but it’s a mining state. And, even more so for us now that vanadium is on the critical minerals list. The U.S. has unveiled its strategy in an effort to rebuild struggling domestic supply chains for metals & minerals it deems “critical” to the country’s manufacturing & defense sectors. Recently this was reiterated when President Trump & Prime Minister Trudeau announced a plan for the U.S. & Canada to collaborate on critical minerals.

What are the latest developments on the metallurgical front?

We continue to make strides on the metallurgical front. In April we announced an average of 95% vanadium extraction from the rock across the deposit, into solution. We do not know what ultimate recoveries will look like just yet, but we are making good progress. And, we’re making strides in the area of pre-concentration, with the aim to reduce the plant size, which would lower the capital intensity of the project.

What are First Vanadium’s plans for a Preliminary Economic Assessment (“PEA”)? Might that be a 1H 2020 event?

No, we think that we can move faster, our aim is to initiate a PEA in the 3rd quarter, with results to be reported before the end of the year.

Why should readers consider buying shares of First Vanadium?

I see very good value and upside; an exceptional senior technical team, a good share structure and a great project. We now have C$1.9 million in cash with the recent private placement closing, and 42.4 million shares. Our share price now is where it was at the beginning of 2018! Yet, we have delivered two successful drill campaigns, a mineral resource with considerably higher grades, and more metal in the ground than our historical resource, and 80% (303 million pounds) of it is in the Indicated category.

That, plus positive metallurgical test work and environmental baseline studies to advance permitting. If one is bullish on the vanadium price, currently at US$8.20/lb., then First Vanadium’s (TSX-V: FVAN) / (OTCQX: FVANF) project in the #1 of 84 ranked global jurisdiction of Nevada should be high on the list of projects to consider investing in.

Thank you Paul, very interesting and timely commentary on the vanadium market and on First Vanadium. I look forward to seeing a PEA later this year!

Peter Epstein

Epstein Research

July 9, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Vanadium Corp., including, but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Vanadium Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of First Vanadium Corp. and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

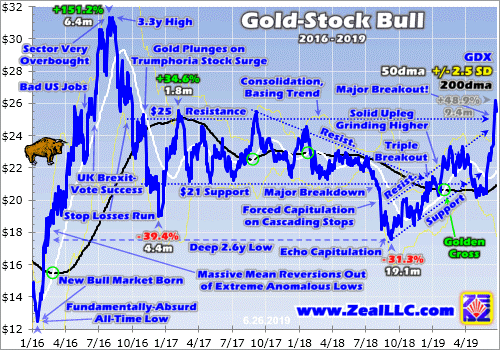

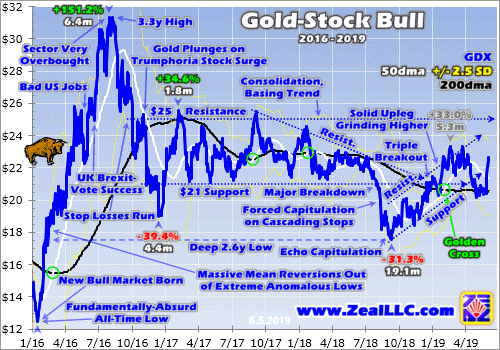

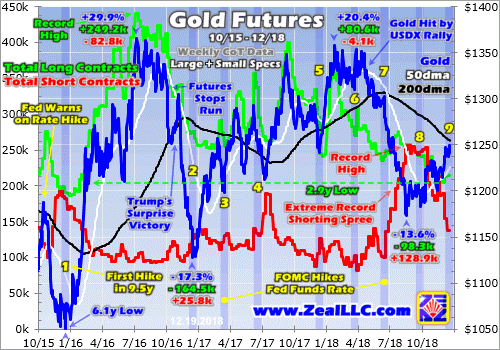

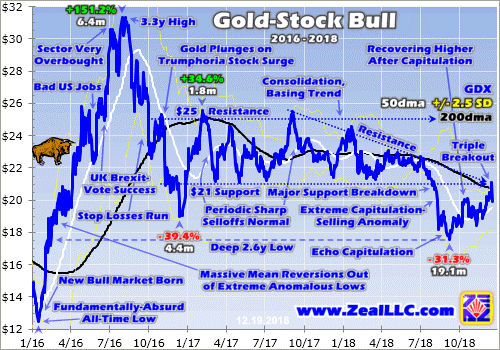

The gold miners’ stocks just blasted higher to a major decisive breakout this week! Driven by gold’s own huge bull-market breakout, the gold stocks surged well above vexing years-old upper resistance. The resulting new multi-year highs are a game changer, starting to shift long-apathetic sector sentiment back towards bullish. This will increasingly attract back traders, with their buying unleashing a virtuous circle of gains.

Traders usually track gold-stock fortunes with this sector’s most-popular exchange-traded fund, the GDX VanEck Vectors Gold Miners ETF. Launched in May 2006, this was the original gold-stock ETF. That big first-mover advantage has helped propel GDX to sector dominance. This week its net assets of $10.5b ran 44.6x larger than the next-biggest 1x-long major-gold-miners ETF! GDX is this sector’s leading benchmark.

And as recently as late May, neither speculators nor investors wanted anything to do with gold stocks. GDX slumped to $20.42 on May 29th, down 3.2% year-to-date. That was much worse than gold’s own slight 0.2% YTD decline then warranted. The gold stocks were really out of favor, largely ignored by apathetic traders. What a difference a month makes though, as their fortunes changed radically in June.

The gold miners started reanimating on May 31st, after Trump unleashed a bombshell warning to Mexico the evening before. He said tariffs would be imposed on all of its exports to the US if it didn’t seriously clamp down on illegal immigration across the US southern border. While Trump subsequently suspended those tariffs on Mexico’s promises to take action, that was the catalyzing event that awoke gold from its slumber.

A couple weeks ago I wrote an essay on the resulting mounting gold-stock upleg, explaining what was going on. But the developments since have been stunning, a colossal bullish surprise. Long neglected, GDX kept on marching higher mid-month leading into last week’s highly-anticipated Federal Open Market Committee decision. GDX closed at $23.67 the day before, already 15.9% higher in only several weeks.

The Fed kowtowed to stock traders’ hyper-dovish expectations and shifted its future rate bias from tightening to cutting, lighting a fire under gold. In last week’s essay I analyzed the gold bull breaking out, which was a momentous sea-change event. Gold rallied 1.0% to $1360 that day with top Fed officials forecasting a new rate cut next year. Gold-stock traders just shrugged at gold’s best close in 2.9 years.

They only bid GDX 1.4% higher to $24.00 after the Fed’s dovish shift. That only amplified gold’s gains by 1.4x, far short of the major gold stocks’ normal upside leverage to gold of 2x to 3x. While gold was high, it had tried and failed for years to break out above its $1350 resistance zone. And gold stocks suffered big and sharp selloffs after those previous forays proved unsuccessful. Traders didn’t expect this time to be different.

That Fed-Day evening New York time, Asian markets reopened as their Thursday morning rolled around. The Asian cultures have a deep cultural affinity for gold, and aggressively piled on in early trading. All that buying catapulted gold from $1358 to $1383 in about an hour! Partially thanks to Iran shooting down a big and sophisticated US surveillance drone overnight, gold’s Asia gains held in last Thursday’s U.S. trading.

Gold closed 2.1% higher that day at $1389, a decisive breakout 1%+ beyond its previous bull-market high of $1365 from way back in early July 2016! That also happened to be a 5.8-year closing high, so gold-stock traders realized big changes were afoot. They poured capital into gold stocks with a vengeance, catapulting GDX 4.4% higher on 3.5x its 3-month-average daily volume! That propelled it to $25.05 on close.

That was a critical technical level, as this GDX chart shows. It looks at the gold-stock price action of the last several years or so during gold’s own parallel bull market. GDX is rendered in blue, its key 50-day and 200-day moving averages in white and black, and 2.5-standard-deviation bands in light yellow. This leading gold-stock ETF had to decisively best years-old upper resistance at $25 to prove this time is different.

Since late 2016, GDX has largely been trapped in a giant consolidation basing trend running from $21 support to $25 resistance. $25 had proven a graveyard in the sky for gold stocks since November 2016, and needed to be overcome to change bearish psychology. GDX’s $25.05 close last Thursday on that new secular gold high was right there. But $25 resistance had to be broken decisively to impress traders.

Last Friday gold climbed another 0.7% to $1399 on pure momentum, yet gold-stock traders were worrying again. So GDX’s resulting 0.6% rally was pathetic, actually lagging gold. While not a decisive breakout over $25.25, or 1% above that long-vexing resistance line, GDX’s $25.21 close was darned close. The major gold stocks as measured by this ETF hadn’t been higher in 21.4 months. That was certainly bullish.

Last Friday and this Monday it was becoming evident that new-high psychology was taking root in gold. That is a powerful force motivating speculators and investors to buy. GDX $25 finally being materially surpassed has long been the key to unleashing this self-reinforcing sentiment in gold stocks. A couple weeks ago when GDX had merely climbed to $23.33 at best, I wrote about this coming critical breakout.

“The higher gold stocks climb, the more traders will want to buy them to ride that momentum. The more capital they deploy, the more gold stocks will rally. This normal virtuous circle of improving psychology and buying will become even more exaggerated as GDX $25 is surpassed. Seeing the highest gold-stock levels in several years will work wonders to improve sector sentiment, unleashing widespread bullishness.”

“This gold-stock upleg’s potential gains are massive spanning such a major upside breakout. Remember speculators and investors love chasing winners, so the higher gold stocks rally the more attractive they’ll look.” Nothing drives trader interest and thus capital inflows like major new highs. And GDX was right on the verge of entering that excitement-fueling zone decisively over $25 as markets opened for trading this week.

This Monday gold surged another 1.4% higher to a dazzling $1419 close! That new 6.1-year high was fueled by sheer momentum, there was little gold-moving news that day. Gold’s new-high psychology was already feeding on itself. And that enthusiasm spilled into gold stocks, with traders bidding GDX another 3.8% higher to $26.17. That was the long-awaited decisive $25 breakout, with GDX blasting 4.7% beyond!

The importance of gold stocks powering through to new 2.7-year highs cannot be overstated. Major new highs act like magnets attracting traders’ attention, interest, and capital. They prove that the long-ignored gold stocks are in bull-market-rallying mode again, portending massive gains to come. They also garner media coverage, which greatly increases the number of traders looking to ride the breakout momentum.

Since late May’s depressing low, GDX had rocketed a huge 28.2% higher in just 18 trading days! Stock traders would kill for those kinds of fast gains. And the major gold stocks’ upleg-to-date advance per this ETF had grown to 48.9% over 9.4 months. That would be impressive for any sector, but is actually still on the smaller side for the high-potential gold stocks. Their uplegs have tended to grow much larger in the past.

The last time gold was hitting new bull-market highs was in the first half of 2016. That was the maiden upleg of this bull, where gold soared 29.9% higher in just 6.7 months. The resulting excitement fueled a deluge of capital roaring into gold stocks, which skyrocketed GDX an incredible 151.2% higher in roughly that same span! While that upleg was exceptionally large, the last major gold-stock bull’s uplegs were big.

Before GDX came along, the primary gold-stock benchmark was the classic HUI NYSE Arca Gold BUGS Index. Like GDX it tracks most of the same major gold stocks, so HUI and GDX price action are usually indistinguishable. The last gold-stock bull straddling GDX’s birth saw the HUI soar 1664.4% higher over 10.8 years between November 2000 to September 2011! Those gains accrued over 12 separate uplegs.

One was an anomaly, the epic mean-reversion rebound after late 2008’s first-in-a-century stock panic. Excluding it, the other 11 normal gold-stock uplegs in that last bull averaged 80.7% gains over 7.9 months per the HUI! So GDX’s 48.9% upleg-to-date advance as of early this week remains well below precedent to be mature. Odds are it will grow much larger in line with past major uplegs before giving up its ghost.

Gold stocks paid a terrible price as gold drifted sideways over the last several years, trapped under that $1350 resistance zone which masked its in-progress bull. That’s why GDX mostly meandered between those $21 support and $25 resistance lines since late 2016. That chronic inability to break out to new highs gradually scared away the great majority of traders, leaving gold stocks incredibly undervalued.

Gold-stock prices are ultimately determined by gold, because it overwhelmingly drives their earnings. So one way to measure gold-stock “valuations” is looking at them relative to gold. This can be done using the GDX/GLD Ratio, the leading gold-stock ETF’s price divided by the flagship gold ETF’s price. That of course is the GLD SPDR Gold Shares. I last wrote about and analyzed the GGR in an early-February essay.

This Monday as GDX finally decisively broke above $25 to close at $26.17, GLD’s shares closed way up at $133.94. That made for a GGR of just 0.195x at the best gold-stock levels in several years. Yet that was still really low by historical standards. The last normal years for the gold market were arguably 2009 to 2012. That stretch was sandwiched between 2008’s stock panic and the Fed’s QE3 stock-market levitation.

The resulting extreme and irrational stock euphoria had a devastating impact on gold. But from 2009 to 2012 before markets became wildly central-bank-distorted and fake, the GDX/GLD ratio averaged 0.381x. That encompassed all kinds of gold environments, from strong bull to budding bear. So there’s no better recent span to approximate gold stocks’ “fair value” relative to gold. Applying that today is super-bullish.

At Monday’s $133.94 GLD close, that historical-average fair-value GGR would put GDX at $51.03. That is a whopping 95.0% higher than its actual close that day! Gold stocks are literally trading at just half of where they ought to be at today’s gold prices, meaning they still need to double just to catch up. And that doesn’t account for higher future gold prices or the GGR overshooting proportionally higher after mean reverting!

At best GDX has powered 151.2% higher within gold’s current bull. But during gold’s last secular bull, the HUI skyrocketed an astounding 1664.4% higher over 10.8 years! Gold stocks are one of the highest-potential sectors in the entire stock markets. When they really start running the resulting gains can truly generate life-changing wealth. That’s why contrarians are willing to suffer between their mighty bull runs.

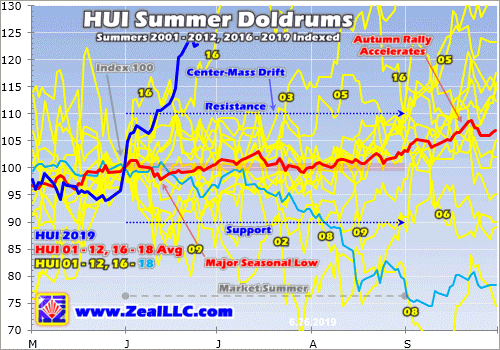

This week’s long-awaited GDX $25 breakout is a critical technical milestone that is likely signaling much-bigger gains to come. The gold-stock surge this month is really special, actually the strongest early-summer performance for this sector in modern gold-bull history! Normally this time of year I’d be updating my gold-summer-doldrums research, highlighting the weakest time of the year seasonally for gold stocks.

Hopefully I can find time next week. This chart looks at the HUI’s average summer performances in all modern gold-bull-market years. Each summer is individually indexed to its final close in May, keeping gold-stock price action perfectly comparable regardless of prevailing gold levels. The yellow lines show 2001 to 2012 and 2016 to 2017. Last year’s summer gold-stock action is rendered in light blue for comparison.

All these lines averaged together form the red one, revealing the center-mass drift trend of gold stocks in market summers. Gold stocks’ current 2019 summer action is superimposed over all that in dark blue. As you can see, this past month’s action is the best summer start gold stocks have seen since at least 2001! They are even tracking better than the summer of 2016 in this gold bull’s mighty maiden upleg.

This chart really illuminates how unique gold stocks’ powerful June rally has been. This is more evidence that a sea-change sentiment shift is underway in this long-neglected sector. That sure implies the gains to come will be much larger than traders expect, driving GDX towards its own new bull highs on balance. In early August 2016, GDX hit its bull-to-date high of $31.32. That’s 19.7% higher than Monday’s breakout close.

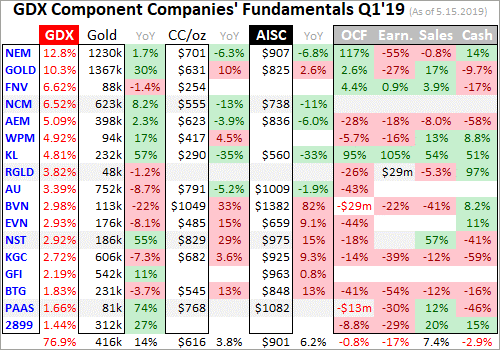

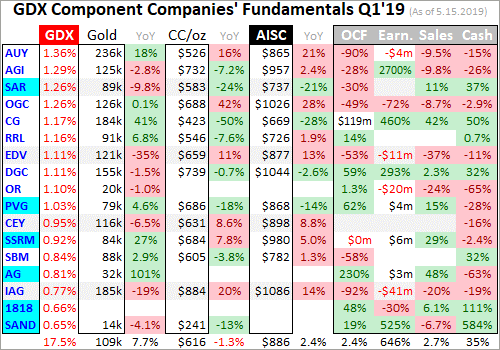

The major gold miners’ fundamentals remain strong and bullish too, supporting much-higher stock prices. After every quarterly earnings season, I dig deep into the GDX gold miners’ fundamentals. They finished reporting their latest Q1’19 results about 6 weeks ago, and I wrote a comprehensive essay analyzing them. At that point GDX was still really out of favor, languishing under its $21 multi-year support line.

Stock prices are ultimately determined by underlying corporate earnings, and for the gold miners that is totally dependent on prevailing gold prices. Gold-mining costs are best measured in all-in-sustaining-cost terms. In Q1’19 the GDX gold miners’ AISCs averaged $893 per ounce. That’s right in line with the prior four quarters’ trend of $884, $856, $877, and $889. Gold-mining profits are going to soar with higher gold.

Gold averaged $1303 in Q1 when the major gold miners were producing it for $893. That implies they were earning $410 per ounce mined. $1400 and $1500 gold are only 7.4% and 15.1% higher from there. As the GDX gold miners’ AISCs reveal, gold-mining costs are largely fixed from quarter to quarter and don’t follow gold higher. So assuming flat AISCs, gold-mining profits surge to $507 at $1400 and $607 at $1500.

That’s 23.7% and 48.0% higher from Q1’19 levels on mere 7.4% and 15.1% gold gains from that quarter’s average price! And as of earlier this week, gold had already climbed 9.2% of that. The major gold miners’ fundamentals are already bullish, but improve greatly at higher prevailing gold prices. With earnings growth hard to come by in general stock markets this year, the gold stocks will be even more alluring.

All the stars are aligning for big gold-stock gains in coming months, with their technicals, sentiment, and fundamentals all looking very bullish. This breaking-out gold-stock upleg has excellent potential to grow much larger later this year, greatly rewarding contrarians buying in early. More and more traders are becoming aware of this sector’s huge potential, and their buying will push the gold stocks much higher.

This is not the summer to check out, but to do your homework and get deployed in great gold stocks. All portfolios need a 10% allocation in gold and its miners’ stocks! Many smaller mid-tier and junior miners have superior fundamentals and upside potential to the majors of GDX. And by the time gold stocks get really exciting again hitting their own new bull highs, much of the easy gains will have already been won.

One of my core missions at Zeal is relentlessly studying the gold-stock world to uncover the stocks with superior fundamentals and upside potential. The trading books in both our popular weekly and monthly newsletters are currently full of these better gold and silver miners. Mostly added in recent months as gold stocks recovered from selloffs, their unrealized gains were already running as high as +109% this week!

If you want to multiply your capital in the markets, you have to stay informed. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q1 we’ve recommended and realized 1089 newsletter stock trades since 2001, averaging annualized realized gains of +15.8%! That’s nearly double the long-term stock-market average. Subscribe today and take advantage of our 20%-off summer-doldrums sale!

The bottom line is gold stocks have joined gold with their own decisive breakout! GDX finally burst back above its long-oppressing $25 upper-resistance line this week. These multi-year highs are a game changer for gold stocks, ushering back long-absent bullish psychology enticing traders to return. They’ve been gone for so long that this entire gold-mining sector is deeply undervalued relative to prevailing gold prices.

That portends huge upside potential as gold and its miners’ stocks return to the limelight on their major breakouts. Traders love chasing winners to ride their upside momentum, and buying begets buying. Of course gold-stock uplegs don’t power higher in straight lines, periodic selloffs to rebalance sentiment are normal and healthy. So any material gold-stock weakness should be used to accumulate sizable positions.

Adam Hamilton, CPA

June 28, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com

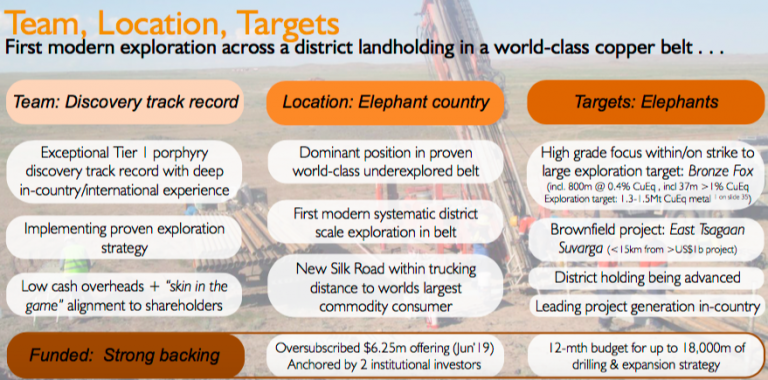

Kincora Copper [TSX-V: KCC] fell off investor’s radar screens due to an extended period of inactivity in 2018, but now the Company is cashed up, team in place, and ready for extensive drilling at 5 independent, large-scale porphyry targets with a 12-month funded budget for up to 18,000 m of drilling.

Kincora has been operating in Mongolia for > 8 years. In 2016, the Company secured unencumbered access to its promising Bronze Fox project and consolidated the dominant landholding in the Southern Gobi copper-gold belt, between and on strike with Rio Tinto’s Oyu Tolgoi (“OT“) copper-gold mine, and the Tsagaan Suvarga porphyry project, via the merger with IBEX, a private vehicle indirectly controlled by Robert Friedland.

This attracted a world-class technical team, credited with multiple discoveries of Tier 1 copper deposits, looking to repeat such successes. Since then, the Company has been executing the first modern systematic exploration program across a district-scale landholding in a highly mineralized, but vastly under-explored copper-gold porphyry belt. Now, drilling is just days away.

These are exciting times for Kincora, the most exciting in the Company’s history. The Company is in a prime position in the copper sector where new discoveries are being well rewarded and successful juniors acquired at significant premiums. For example, just this week Australian-listed MOD Resources was taken out by a billion-dollar market cap Sandfire Resources.

A new cornerstone investor, HK-based New Prospect, now the 2nd largest shareholder with about 12% of the Company, is a natural resource specialist fund with an extensive global network. LIM Advisors remains the largest investor, one of the longest operating alternative investment managers in Asia, they invest across the capital structure in deep value & special situations.

Investors in small cap natural resource stocks know that the best time to be in a junior is right before a BIG discovery. That’s the time we could be at right now with Kincora. Management just raised $6.25M. Will there be a new discovery! More than one!! None!!! Yes, there could definitively be zero new discoveries…. This is a highly speculative situation, but backed by a team that has an excellent track record of large discoveries.

Even without blockbuster discoveries, the Company has planned a very detailed and well thought-out drill program that’s sure to cover a lot of bases and provide a pipeline of news flow over the next 12 months. Raising $6.25M in a very tough market at a $7M pre-money valuation was a BIG success in and of itself, demonstrating the strength of management, the projects / targets and the massive opportunity.

The de-risking capital raise is strong evidence of the belief by cornerstone investors & seasoned management that Mongolia is a great place to, potentially, make the newest globally significant copper discovery since 2014. To learn more, please continue reading this Interview of Sam Spring, President & CEO of Kincora Copper [TSX-V: KCC].

Can you talk about how we got to the point of a substantial drill program starting very soon?

After 2018 being a transitional year of setting the right corporate foundations for success, we are entering an exciting period where the drill bit will drive Kincora’s valuation once again. This month we will commence an aggressive, multiple rig, fully-funded drill program. The focus is discoveries on 5 large, independent copper porphyry targets on our 100%-owned Bronze Fox and East Tsagaan Suvarga (“East TS”) projects.

This will be the first drill program conducted by our industry-leading technical team, who have found multiple Tier 1 copper assets. For the last 3 years, we have undertaken the first modern, district-scale, exploration across this vastly mineralized, but significantly under-explored Southern Gobi copper-gold belt.

As readers may know, there are 2 large-scale porphyry projects in this region. Rio Tinto / Turquoise Hill Resources’ Oyu Tolgoi open pit mine and underground development project, and a privately-held open pit development project called Tsagaan Suvarga. We believe there are more globally significant copper discoveries to be found.

Limited drilling supports our Bronze Fox project potentially hosting an independently defined, conceptual exploration target of 1.3 to 1.5 M tonnes (midpoint = 3.086 billion Cu Eq. pounds). That would be an in-situ value of $11 billion (1.32 CAD/USD, US$2.70/lb. Cu).

The first hole of the program will, for the first time, correctly test a very large zone (previously drilled in the wrong direction). However, prior drilling still managed to intersect 37 m at > 1% Cu Eq., within 864 m of 0.38% Cu Eq.

Our East TS project sits in the shadows of a billion-dollar open pit construction project at Tsagaan Suvarga (“TS”). Within this brownfield setting, we’re drilling 3 separate targets that are the closet analogues to the high-grade ore bodies at OT…. since OT! While just targets, readers should understand that what we’re exploring for is large and in a very favorable location and geological setting. OT’s ongoing underground expansion is the largest hard rock mining project in the world. It could become the 3rd largest copper mine on the planet, with a 100-year+ mine life.

Kincora was formed in 2011, but we are in the strongest position today that the Company has ever been in. Yet, our current market cap of $12M, (with $6M cash!) is a fraction of our peak valuation of nearly $50M. At that time, we had attracted a buyout offer for the Company and had signed 14 NDA’s with interested parties.

While naturally I’m biased, I think it would be hard to find many juniors with similar risk/return profiles and multiple near-term catalysts, backed by a world-class management, Board, Technical team, Advisors and key shareholders, trading at such a low valuation.

With the Company shortly ramping up drilling of our existing exploration portfolio, and focused on ongoing expansion opportunities, Kincora is the most active foreign-listed junior seeking to make the next Tier 1 discovery in Mongolia.

You just closed on a $6.25M capital raise in a very difficult market. Who were the key investors in this very important round?

~60% was taken up by 2 large natural resource funds and associated groups, who will represent > 40% of Kincora’s shares going forward. These groups, LIM Advisors & New Prospect Capital are both Hong Kong based funds and have a track record investing in Mongolia.

In total, there were > 30 investors in the deal, with strong Board / management participation and good support from high-quality sophisticated investors. As you can imagine, given current market conditions, a lot of work went into this raise. We truly appreciate the vote of confidence from those who invested.

How much of that $6.25M will go towards exploration? Please describe the upcoming drill program.

The vast majority will support Kincora undertaking the most aggressive exploration & discovery drill program anywhere in Mongolia this year. ~$5M will cover up to 18,000 m of drilling at Bronze Fox & East TS, plus project generation activities and advancing earlier-stage exploration targets.

Mongolia has unique geological potential to host globally significant discoveries, and that is what we are focusing on. This raising, with the accompanying warrant package, aligns our capital markets strategy with our exploration & expansion plans and gives us a good shot (but no certainty) at making new discoveries.

We are on record stating that these drill targets are, ‘as good as you get within a global setting for their respective stages’. The key driver in the next 12 months is proof of high-grade & our geological concepts, to confirm our models & interpretations with positive drill results.

In addition to your management team & Board, please describe recent due diligence done by independent advisors, consultants & analysts. Didn’t your largest shareholder also commission a study?

Our drill strategy is the culmination of almost 30 years’ copper exploration experience in this belt by senior members of our team, 5 years of exploration work and model refinements by ourselves and previous owners (including Ivanhoe Mines and IBEX) that provide us with strong conviction to focus on the selected 5 targets.

Kincora has been through 5 technical reviews since mid-2017, including from 1) a leading natural resource private equity group, 2) the EBRD, 3/4) LIM Advisors (twice) and 5) New Prospect Capital, all of which have resulted in capital being invested.

As you have picked up on Peter, our largest shareholder commissioned an independent technical review of our targets, work programs and strategy before becoming a cornerstone investor in our latest offering. This review suggested a, ‘discovery’ had already been made at Bronze Fox within the under-explored target zone to the west of a key regional fault in an area we are calling West West Kasulu. This is where the first drill hole will go. In the independent consultant’s opinion, this target area has been significantly upgraded by recent exploration activities.

While we are optimistic, and management participated in the recent raising, and have undertaken detailed systematic exploration, there’s nothing left to do but drill these targets. Please let me reiterate that Kincora is a high-risk, exploration play. Hence, there are high rewards for success.

A risk is that it might cost tens of millions to delineate an attractive NI 43-101 compliant resource. What is your team’s goal for the upcoming drill program, can you articulate what success might look like?

Absolutely. We appreciate the fact that porphyries are capital intensive, and that exploration is very risky. More meters of drilling provide us a better chance of confirming our geological concepts and riding the value creation curve for shareholders.

The best recent example of a large-scale copper porphyry discovery is that of SolGold at its Alpala project in Ecuador. The deposit at Alpala is deep, so drilling costs there are significantly more than in Mongolia. In March 2016, SolGold raised A$5.7 million at 2.3p/share, having drilled 13 promising holes and seeking to confirm its discovery. An equivalent drill program to what Kincora is now looking to complete at our 2 projects. They had fantastic results…. Over the course of 31 months, SolGold drilled a further 54 holes, attracted both Newcrest and BHP as strategic investors, and re-rated 20x for shareholders.

That’s what success at the target-testing phase of drilling can result in, even in difficult capital markets and a flat/decreasing copper price environment, which we believe is temporary.

At Bronze Fox, our drill campaign is designed to advance the strike potential away from the fault to the west, demonstrate the interpreted, significant increase in tonnage & grade potential, and confirm a new discovery. Prior higher-grade intersections include 3 of 4 holes drilled by Kincora that returned > 1% Cu and/or Cu Eq., incl. the best hole, F62, which hosted 13 m of 1.15% Cu / 1.41% Cu Eq., within 37 m at 0.83% Cu / 1.04% Cu Eq. and 864 m at 0.38% Cu Eq.

At our East TS, the geological concept we are seeking to confirm is that OT-style mineralization is present. Each of the 3 targets at East TS have large-scale potential, with individual coincident geophysical anomalies equivalent in size to ore bodies at OT and SolGold’s Alpala project.

While more conceptual and risky than the 2 targets at Bronze Fox, such a setting and scale of targets is unique – if located in more established copper districts around the world — it’s likely the area around TS & East TS would have already seen extensive drilling.

A rule of thumb for porphyry discoveries is that ~50,000 m of drilling generally provides visibility for ~5M tonnes Cu Eq. metal. Exercise of the warrants that were part of the recent offering would bring in an additional $15M (2.5x the recent raising), and enable another 100,000 meters of drilling.

There are many Copper bulls, yet the price at US$2.70/pound is half of what some bulls think is coming. Do you have a view on the Copper price?

A good question, we get asked that a lot. I will leave the forecasting to the experts, but we’re noticing that most investors see the writing on the wall. Like us, they believe the supply side will at some point (perhaps soon?) struggle to meet even average-trend demand growth, let alone any acceleration from increasing global electrification. This theme is being picked up by generalist investors as well, who have noticed what an unexpected supply shock has done to the iron ore price this year.

Regarding the industry players (mid-tiers & Majors), there has been a notable, but quiet, shift towards looking at new growth projects again over the last 18 months. BHP & Rio Tinto are even talking about organic exploration success stories, focusing on copper as a preferred commodity for expansion. That said, we are just starting to see more of the traditional miners expand into earlier stage projects to rebuild their pipelines.

Time will tell, but I certainly think that even at current copper prices, if we find what we’re looking for, there will be significant interest in Kincora. A tailwind from rising copper prices would of course be welcomed, but given the lack of exploration success industry-wide, globally, for many years now, the project pipeline is in great need of new, sizable discoveries. That is what we believe Mongolia and our targets offer investors.

Please talk about Mongolia, some readers probably won’t invest there. What do you tell investors, shareholders, prospective investors — about Mongolia country risk?

At the time I joined Kincora in 2012, Mongolia was the fastest growing economy in the world. This was driven by the first phase emergence of delivering previously untapped resources to international markets.

This emergence meant that at the time it was almost mandatory for coal & copper Majors to be seeking entry into the southern Gobi regions, with product trucked to the world’s largest consumer of both commodities. We are 5 Prime Ministers, 2 governments, a number of high profile disputes and reversals to unfavorable investment laws later, but the rocks and big picture potential remain unchanged.

In a landscape of few significant greenfield projects recently being commissioned, OT is proof of concept that Mongolia is a mature mining jurisdiction. OT is the largest development project in Mongolia’s history. It’s expected to account for up to a third of Mongolia’s GDP by the mid 2020s. It paves the way for companies like ours by lowering barriers to entry and we and others greatly benefit from newly built regional infrastructure.

When one looks at other copper jurisdictions, it’s becoming harder and more expensive to operate. Chile’s 2018 copper output was greater than the 2nd, 3rd & 4th largest country producers combined. The multi-billion-dollar cap-ex profile for Chile’s Codelco, just to keep production flat, shows the increasing challenges regarding water, community relations & high altitude, not to mention a declining copper grade!

Many other large copper supply regions are also difficult and/or increasingly difficult to operate in; look at recent developments in the DRC, China, Panama, Russia, Zambia, Indonesia, PNG, etc.

Given the team and operational track record we have at Kincora Copper [TSX-V: KCC] we are eyes wide open to the risk/reward scenario in Mongolia, which we find compelling, exploring for the next globally significant copper discovery.

Your readers should stay tuned for drill results, which should start arriving in 5-6 weeks’ time. We expect results to be ongoing for the rest of the year.

Thank you Sam, I think we covered a lot of ground. Bottom line, drill results will define Kincora Copper going forward, and a lot of smart money is betting on good drill results between now and year end.

Peter Epstein

Epstein Research

June 27, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Kincora Copper including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Kincora Copper are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owns shares in Kincora Copper, and it was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

- A lot of Americans getting a myriad of government entitlements thought that President Trump would recreate the 1950s for them.

- If Trump had eliminated the PIT (personal income tax), capital gains tax, and corporate income tax, I’ve estimated that around $100 trillion in capital would have surged into America.

- That would have created a super-sized version of what Switzerland achieved at its peak.

- Sadly, Trump and his team didn’t do that, mainly because they are giving the citizens what they want; bigger government, more debt, and more storytelling.

- To understand what is likely coming next for America, please click here now. Mike Wilson does a near-perfect job of outlining what I believe is in store for H2 of 2019.

- Yesterday, Goldman Sachs’ chief economist was quite adamant that the consensus prediction of three rate cuts in the second half of this year would go awry, and the Fed will not cut at all.

- The risks are clearly rising for U.S. stock market investors.

- My biggest concern is that many Americans sold a lot of their gold stocks into the lows and are now aggressively buying the US stock market. The size of their buying is quite large.

- Unfortunately, their buying appears to be based mostly on Trump’s frequent “Let’s make America great!” pump-up tweets, rather than prudent study of the business cycle.

- The U.S. business cycle is very late stage now, and that’s when investors must reduce stock market exposure and increase exposure to gold!

- Having said that, please click here now. Double-click to enlarge this TQQQ triple-leveraged Nasdaq ETF chart.

- Almost 80% of mainstream stock market analysts predict the Fed will cut in July. If they are correct, the stock market will likely soar to new highs. If they are wrong, the market likely begins crashing at the start of August.

- A lot of stocks in the Dow Jones Industrials index are already at new highs, and that’s usually a sign that the indexes will make new highs too, regardless of whether a crash follows soon after that. I think new highs for the indexes occurs ahead of the July Fed meeting. That meeting also likely marks the final bull market peak for the U.S. stock market.

- At my https://guswinger.com swing trade service, we are long the stock market via TQQQ. My system is mechanical; I am always either long or short the Nasdaq via TQQQ/SQQQ. I’m also always long or short gold stocks via NUGT/DUST.

- Even if the Fed doesn’t cut rates at the July 31 meeting, the market has about six weeks to keep rallying before getting disappointed by the Fed’s decision.

- Also, I would not rule out a rate cut, because the Fed has tended to support the stock market whenever it gets into trouble. The Fed has also tended to support the U.S. government with lower rates when the government wants to borrow a lot of money.

- What about gold? Well, I suggested that investors should brace themselves for a pullback from $1350. That’s clearly in play this week as the stock market rallies. Also, Indian dealers have reduced their buying after the big gold price surge.

- Please click here now. Double-click to enlarge this daily gold chart. The most impressive event in the rally from the $1272 area is the creation of a new up channel!

- A range trade for gold is likely now. I think it will be in the $1310-$1350 area, although a wider range of $1292-$1350 is also possible. I’m happily short gold stocks at my swing trade service via DUST/JDST after a big NUGT/JNUG win, but I do expect some gold stocks to keep rallying even as gold consolidates in the trading range.

- On that note, please click here now. Double-click to enlarge this Kirkland Lake chart. My swing trade subscribers and I hold call options on this great company. The stock is trading above its February high while most gold stocks are not. This kind of outperformance is what I look for when considering a call options position.

- As GDX tumbled yesterday, Kirkland rallied higher!

- Speaking of GDX, please click here now. Double-click to enlarge. The entire pullback from February is starting to look like a giant flag pattern. The price target of the pattern is about $29.

- Please click here now. Double-click to enlarge. That’s a second look at the GDX chart. Any consolidation that occurs now will build a H&S bull continuation pattern as well as more flag-like price action.

- The July Fed meeting (which occurs as the gold love trade strong demand season begins) could create a stock market inferno and a gold stocks “Rally to the stars”. The bottom line: Investors who pare their stock market exposure as the US business cycle matures and increase their exposure to gold stocks are clearly acting with professionalism and prudence!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Golden Junior Giants!” report. I highlight key junior miners that are outperforming in this gold price consolidation zone, with key buy and sell tactics for each stock!

Thanks!!

Cheers

Stewart Thomson

Graceland Updates written daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

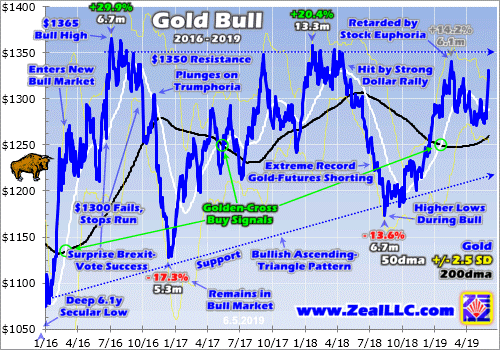

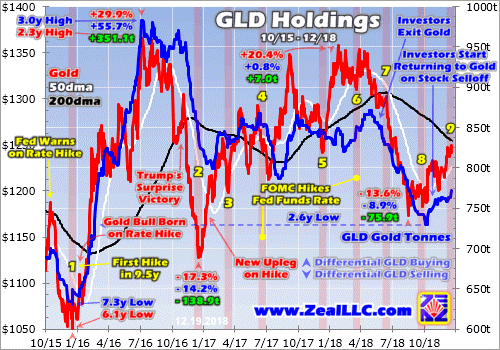

Gold surged sharply over the past week or so, nearing a major bull-market breakout! Nearly everyone was surprised by this violent awakening, which erupted suddenly as gold languished around year-to-date lows. If this dramatic rally has staying power, gold has good odds of achieving decisive new bull-market highs. That would change everything psychologically, ushering gold and its miners’ stocks back into favor.

Gold has largely flown under traders’ radars this year, mostly drowning in apathy. Actually this unique asset had a strong start, climbing 4.6% year-to-date by mid-February to hit $1341. While merely a 10.1-month high, gold was close to a major bull-market breakout. For several years now, gold has faced stiff resistance around $1350. It has repelled gold multiple times, looking like an impregnable Maginot Line.

But gold’s promising ascent was short-circuited from there, unleashing a disheartening slump over the next 10 weeks or so. By early May, gold had retreated 5.2% to $1271. The primary culprit was resurgent euphoria in the US stock markets. Equity exuberance has long proven gold’s mortal nemesis. When stock markets are high and expected to continue climbing on balance, gold investment demand often withers.

The recent gold action can’t be understood without the context of the US stock markets as represented by their flagship S&P 500 index (SPX). Heading into last September, the SPX was marching to a series of new all-time record highs. Since gold tends to climb when stock markets sell off, there was little demand for this essential portfolio diversifier. Why buy gold when stocks seem to do nothing but rally indefinitely?

That who-cares sentiment helped fuel all-time-record short selling in gold futures, hammering gold down to $1174 in mid-August for a 19.3-month low. Stuck in the shadows of euphoric stock markets, gold largely drifted sideways from there averaging $1197 until early October. But on October 10th, hyper-complacent stock traders were finally confronted with a serious selloff as the SPX plunged 3.3% that day alone.

Earlier hawkish comments from the Fed chairman were to blame. With stock markets bleeding, traders remembered gold. The world’s leading and dominant gold exchange-traded fund is the GLD SPDR Gold Shares. According to the latest data from the venerable World Gold Council, GLD’s 784.3 metric tons of gold bullion held in trust for its shareholders at the end of Q1’19 represented 31.6% of global gold ETFs’ total.

In early October with the SPX just fractionally under its recent record peak, GLD’s holdings slumped to a deep 2.6-year secular low of 730.2t. But a few trading days later as the SPX’s sudden and sharp plunge started to kill complacency, GLD enjoyed a big 1.2% holdings build. When stock traders buy GLD shares at a faster pace than gold itself is being bought, GLD’s managers equalize that excess demand by buying gold.

That SPX selloff snowballed into a severe near-bear correction, down 19.8% by Christmas Eve. With the stock markets burning, investors remembered the timeless wisdom of prudently diversifying their stock-heavy portfolios with counter-moving gold. It had rallied 8.1% in 4.3 months by the time a super-oversold SPX was ready to bounce. That gold upleg kept growing, ultimately extending to 14.2% gains by mid-February.

But as gold neared that major $1350 bull-market breakout then, stock euphoria came roaring back with a vengeance. The SPX had rocketed 18.2% higher out of its correction low by then, fueled by a radical shift back to dovishness by the Fed! It completely capitulated and caved to the stock markets, declaring that its quantitative-tightening monetary policy was open for adjustment in contrast to earlier statements on QT.

By that point the SPX had regained nearly 3/4ths of its total correction losses, so exuberant-again traders started to forget gold. Gold investment demand peaked in late January the day before the Fed gave in on QT, capping a 12.8% GLD-holdings build over 3.8 months. The higher the SPX rallied in recent months, the greater stock euphoria grew and the more gold was forgotten. Yet again stock euphoria stunted gold.

The SPX peaked at the end of April at another new all-time-record high. That extended its total monster-bounce rebound rally since late December to a colossal 25.3% in 4.2 months! A couple days later in early May with the SPX still near records, gold fell to that $1271 YTD low. Euphoric stock investors’ exodus from gold persisted another week, when GLD’s holdings slumped to 733.2t. That was down 11.0% in 3.3 months.

Gold failed to break out above its years-old $1350 resistance zone in mid-February because skyrocketing stock markets forced it back out of favor. Between late January and mid-May, fully 97% of GLD’s holdings build fueled by the SPX’s severe near-bear correction largely in Q4 had been erased! Just like late last summer, gold was again hostage to lofty euphoric stock markets. Investors wanted nothing to do with it.

But the SPX started rolling over again in May, slowly at first. It was shoved after Trump got fed up with China backtracking on nearly a year’s worth of trade negotiations with the US. On May 5th he warned that tariffs on $200b of annual Chinese imports would blast from 10% to 25% going effective the following Friday. That gradually drove the SPX lower into mid-May, including serious 1.7% and 2.4% down days.

So once again just like in October the last time the SPX rolled over hard, gold caught a bid. It rallied back up to $1299 in mid-May as investors again remembered stock markets can also fall. GLD’s holdings began modestly recovering as stock-market capital started slowly migrating back into gold. But that nascent trend reversed again in mid-May as stock markets bounced sharply higher, unleashing surging euphoria.

The primary driver of gold in recent years has been stock-market fortunes. Gold often falls out of favor when stock markets are high and rallying, then starts returning to favor when they sell off again. In a very real sense gold is the anti-stock trade. While it doesn’t only climb when stock markets weaken, that’s what mainstream investors remember gold for. Its investment demand is rarely strong near stock-market highs.

So gold again slumped back near $1273 by late May as the SPX rebounded, further demoralizing the few remaining contrarians. This metal felt pretty hopeless heading into its summer doldrums, its weakest time of the year seasonally. Then a Trump bombshell shocked stock traders out of their complacency. He warned the US was levying escalating tariffs on all Mexican imports to force Mexico to fight illegal immigration!

Last Friday May 31 was the first trading day after that surprise, and the SPX fell 1.3% to its lowest close since its all-time-record peak a month earlier. That extended its total recent selloff to 6.6%, so worries mounted. Gold had closed at $1288 in the prior day’s US trading session. Overnight after Trump’s tweet on Mexico tariffs gold rallied to $1297. That upside continued in the U.S., with gold closing 1.3% higher at $1305.

$1300 is a critical psychological line, heavily coloring sentiment especially among hyper-leveraged gold-futures speculators. They tend to buy aggressively when gold regains $1300 from below, and sell hard when gold breaks under $1300 from above. But while gold-futures trading heavily influences short-term gold price action, only sustained investment buying can ultimately grow gold uplegs to major status.

GLD’s holdings are the best daily proxy available of gold investment demand. And last Friday when gold surged, GLD merely saw a small 0.3% holdings build. American stock investors weren’t buying gold, it was the gold-futures speculators. These traders control far-less capital than investors, so their available buying firepower to push gold higher is limited. Gold uplegs never reach potential without investment demand.

The Asian markets were closed last Friday as gold rallied back over $1300 in the States. So when they opened again this past Monday June 3, Asian traders piled on to the gold buying. By the time the U.S. stock markets neared opening that day, gold was already up to $1317 in overnight trading. Once again that global momentum carried into the U.S. session, helping gold surge another 1.5% higher to $1325!

While great to see, that was still just a 3.2-month high. Without investment demand, gold’s new surge was unlikely to last very long on gold-futures buying alone. But something big changed that day in the U.S. markets. American stock traders, which had mostly shunned gold since late January, took notice. They started shifting capital back into gold via GLD shares in a major way, driving a huge 2.2% build in its holdings!

That was the biggest single-day percentage jump in this leading gold ETF’s holdings in 2.9 years, since early July 2016. That happened to be soon after the UK’s surprise pro-Brexit vote, when gold soared on the resulting uncertainty. While one day doesn’t make a trend, such a massive shift in gold investment buying is definitely attention-grabbing. If investors continue returning on balance, gold is heading way higher.

As this chart shows, gold is now within easy striking distance of a major bull-market breakout! It is not only nearing that vexing $1350 resistance zone, but has a high base from which to launch an assault. If gold-investment demand persists, gold doesn’t have far to run to hit new bull-to-date highs. Of course further stock-market weakness on balance would greatly help, but it’s not necessary with new-high psychology.

Blinded by apathy, not many traders realize gold still remains in a secular bull market. It was born from deep 6.1-year secular lows in mid-December 2015, the day after the Fed’s first rate hike in its latest tightening cycle. Over the next 6.7 months gold soared 29.9% higher in a massive upleg, entering new-bull-market territory at 20%+ gains. That left gold very overbought, so it crested at $1365 in early July 2016.

After strong bull-market uplegs big corrections are totally normal to rebalance sentiment, bleeding off the excessive greed at preceding highs. Gold consolidated high just under $1350 after that initial upleg, then fell to its 200-day moving average. It had resumed rallying in October 2016, but reversed sharply after Trump’s surprise election victory in early November. That pivotal event indirectly forced gold into a nosedive.

Gold plummeting in that election’s wake was the result of incredible euphoria, or Trumphoria at that time. Trump not only won the presidency, but Republicans controlled both chambers of Congress. So stock markets soared on hopes for big tax cuts soon. The SPX surged dramatically higher on truly-epic levels of euphoria, which in turn battered gold. Most investors shun gold when stock markets look awesome.