Everyone has different reasons for investing or speculating in the resource sector. I believe, for the majority of the participants, it’s the allure of 10 baggers that attract them to the juniors.

While the appeal to windfall profits is attractive to almost anyone, I believe it’s exactly this mindset that keeps many investors from actually realizing the gains they are given in the market.

Too many times, I have spoken to fellow investors who haven’t taken money off the table when it’s there, and are left holding the bag until the market turns or the company successfully answers the next unanswered question.

First, if you are an investor who can stomach the ebb and flow of the market then taking a long-term position in juniors can work. Secondly, and key to the first point, it can only work if you are right about the junior company in which you are invested. Will they continue to get ‘yes’ answers as they pursue the development of their mineral deposit?

The juniors draw much of the attention in the resource market, however, I think that there are larger companies that have big upside potential, pay a dividend, and are actual investment-grade companies.

Let’s take a look at one of them!

Altius Minerals Corporation

I’m very bullish on both precious and base metals moving forward. However, the pragmatist in me is especially drawn to the base metals, as their value proposition in today’s society is so easily understood.

Today, I have for you an interview with Chad Wells, VP of Corporate Development of Altius Minerals Corporation (ALS:TSX). Altius is the sector’s only diversified base metal royalty and project generation company.

Currently, Altius has 15 producing royalties in copper, zinc, nickel, potash, iron, thermal and metallurgical coal. In addition, the project generation side of their business has drastically grown in overall equity value since 2016, moving from roughly $22 million to $68 million at September 30.

There are 54 new projects since Q1 2016 within Altius’ project generator portfolio and these will not only be the source of cash through equity sales in the future, but more importantly, will be the source of new cash flow by way of the royalties that are associated with most of the projects in their portfolio.

In my opinion, Altius is the best example of intellectual capital and how people are, by far, the most important commodity in any business.

As Wells mentions in our conversation,

“We’re a group that sticks to our guns, and believes in our own reasoning and rationale. At the end of the day, it’s about relying upon your own technical expertise and surrounding yourself with the right people that are willing to give you the right opinion that is unbiased, genuine and legit.”

I have long been an Altius shareholder and, in my opinion, would say that if I could only own one company in the sector, it would be Altius Minerals, hands down.

Altius Minerals (ALS:TSX)

MCAP – $556 M (at the time of writing)

Shares – 43.0 million

Annual Dividend – $0.16 / share

Outstanding Debt – $120 million

Cash and Public Equity Holdings – $180 million ($33.8 million cash)

2018 Royalty Revenue Guidance – $64M to $69M

Brian: In my conversation with Brian (referring to CEO Brian Dalton) last November, he was super bullish on iron ore and, over the course of the year, Altius has taken big steps to capitalize on the iron ore market. First in March, by increasing your position in Alderon Iron Ore and, most recently in Q3, increasing your position in Labrador Iron Ore Royalty Corporation.

Can you please explain the opportunity you see in the iron ore market?

Chad: We’ve been a mainstay player in the Labrador Trough since 2004 and 2005. Originally, it was from an exploration perspective where we generated projects and sold them on to third parties. Alderon Iron Ore was created during that time, as a part of that strategy, and lead to us becoming very intimate with the iron markets. The Labrador Trough iron ore fits a niche portion of the global marketplace.

Brian (referring to Altius CEO Brian Dalton) has an innate ability to see around corners so he’s been predicting a bifurcation happening in the broader iron ore market this past few years for high grade iron ore with low impurities, compared to the lower grade, higher impurity stock coming out of the Pilbara. A lot of it’s being driven by Chinese pollution standards and emissions targets through their steel mills. You’ve seen the Chinese cut significant volumes of steel production last year because mills were burning lower purity met coal and iron ore.

That’s led to a premium for the high grade, low impurity products. While the quoted price for iron ore, let’s say is at $70 per ton, the high grade Trough products are getting better than $100 per ton, while low grade is trading at a discount.

Brian recognized the separation that was coming in the market between high and low grade long before the broader market did. For us, it spawned an investment thesis to buy a substantial share position in Labrador Iron Ore Royalty Company (LIORC) mainly accumulated with the Fairfax preferred money starting in early 2017. LIORC has a 7% gross revenue royalty on Iron Ore Company of Canada’s (IOC) Carol Lake operations, as well as a 15% equity stake. LIORC is a passive type issuer, taking the money that they get from the royalty and then dividending most of it straight to shareholders.

For us it was the opportunity to have exposure to a royalty on a premier iron asset in Labrador, at a time when we thought the market was going to start to take recognition of that.

Over the last year, we increased our Labrador Iron Ore Royalty Corporation holdings substantially. If you look at our average price, which was around $17 a share before we bought the most recent addition of another .4%, LIORC stock traded last week as high as $31. At the same time, the yield of the dividends that we’ve realized off the asset are quite pronounced. And of course, we treat it as royalty income, effectively, in our per annum royalty revenue. So it fills out some of that diversified commodity exposure. So it’s been really good.

Alderon was much more strategic. We were a founder, having discovered the underlying Kami deposit way back in 2005-06. Our recent doubling up, if you will, on Alderon, goes back to this bifurcation in the iron ore market thesis, which we believe is a real thing and that’s going to last. It’s also worth mentioning that we bought the additional $5 million stake from Liberty when we agreed to a friendly transaction buying out the balance of the potash royalties that we’d held together in a JV.

With that comes the reality that you’re playing Carol Lake, through LIORC. Also, we have a convertible debenture with Champion Iron. Champion is the company that bought the Bloom Lake assets for $10 million in cash plus assumed liabilities of around $43 million from Cliffs, who had sunk nearly US$3 billion of capital into the project during the last iron bull.

The way we see things playing out in the Trough, we believe IOC brings a lot of transparency and reality to the broader marketplace, of the niche, that Labrador iron fits. We think that spills over into Champion, which is a very high margin operation right now, but is flying under the radar. We think the market will take credence and recognition there.

And as this market continues to want more high grade, low impurity iron ore, the next shovel ready project in that district is Kami. For us to buy that stake, on favourable terms, in Alderon from Liberty, brings us back to being that major shareholder with a big stick , it makes a lot of sense for us strategically.

If you reflect back to the last cycle, it was the asset that would have tore the lid off the can for Altius as a royalty generative business. The thing that most of the marketplace doesn’t realize today is that Altius is a different type of royalty company. It’s not a Franco or a Wheaton, who grows through acquisition. We actually grow our royalty portfolio organically and Alderon is one example of that.

In the past bull market in iron, around 2011, when we thought that Kami was going to get built, Alderon raised a bunch of money with the Chinese partner, Hebei Group. It almost got through the window in the sense of raising the capital to build a new mine. If that had to have happened, not only would we made a couple hundred million on the equity, but we would have had an underlying royalty on that asset at 3% gross royalty that based on the feasibility numbers of the assessment at the time, it would have generated about $25 million per year of royalty revenue for Altius for 20+ years. The reason it didn’t happen is because the iron ore bull market ended so quickly when prices dropped from around $130 per tonne to levels less than half that. If you add the premiums to the current spot, we’re edging closer to $100+ again.

Alderon is an extraordinary opportunity of optionality and because of what’s happened in the bigger iron ore market and because of the strategic significance of Labrador iron product in general, I think it happens this cycle.

Kami still needs a billion dollars in capital to get it done, but consider what’s going on with Rio Tinto and IOC and the rumors of them IPO-ing their IOC stake, and, again, the success of Champion in restarting Bloom, and it seems a reasonable bet that Alderon will raise the capital this time around. It might get built. If it does, it will differentiate Altius from all of the others because the net asset value just from the royalty aspect that gets created from nothing, is profound.

Brian: That leads into my next question, generally speaking, in your opinion, how difficult is it to raise $1 billion to develop a mine, today?

Chad: Very difficult and, in saying that, today’s market is probably not the one to do it in. Will that market come? Of course it will. One thing that’s going to be very apparent in what I’ll call the pending bull cycle in commodities, is that the story is going to be about supply this time around, not demand.

What we’ve seen happen is the world has not developed enough copper, nickel and high grade iron ore mines to sustain just the static needs of society. So ultimately, it’s going to be a supply crunch and there’s just not going to be enough supply out there.

So that will incentivize commodity pricing, and incentivize capital, and more mines will get built. So will it happen? It will. The iron ore business is a bit different, because there is a lot of iron ore that came on through the last cycle through investment. But most of it is in this low grade or medium grade stuff. So it doesn’t have the strategic niche of this high grade, low impurity ore, which quite frankly, the Chinese need.

So is the capital there today? Probably not. Will it come? It will. Also, I’d say you don’t necessarily have to think that these things are going to be built by the market. There’s a lot of diversified miners out there that have good balance sheets, have made a lot of money here in the last few years, again, and are going to be looking for shovel-ready assets to acquire to develop themselves. Maybe some of these things get built in different ways, not necessarily going to be through the capital market conventions of a bull market, if you will.

Brian: Earlier this year, Altius entered the lithium market with the investment in a closed end limited partnership with Lithium Royalties Corporation. The deal gives Altius the rights to buy up to 10% of selected royalty direct investments.

Generally speaking, what criteria is Altius looking for in terms of the ideal investment in the lithium space? For example, does the lithium deposit type or jurisdiction matter?

Chad: We’ve always been a group that has focused on exploration and investment in bread and butter commodities, which lithium would not fit. We’ve seen a lot of these specialty themes over the years and we haven’t invested in them because their supply and demand fundamentals have been so wonky that we just weren’t comfortable with the volatility.

In the case of lithium and the battery metal craze in general, I’d say we missed it with lithium. We didn’t necessarily believe that it was going to be one of these bread and butter commodities. I think we’ve come to realize that it is something that we should have spent more time investing in earlier through our exploration business, but we didn’t. Because regardless of how much we try to minimize the forecasts of different battery chemistries in the EV build-out scenario, you just can’t ignore lithium. And the big correction in the pricing this year gives us a more comfortable entry point to be buying when prices are not so near the top. So it is a bit of a catch up game.

What we did do this year is we partnered with expertise. The guys at Lithium Royalty Corp., especially Ernie Ortiz, the CEO of that ship, he’s a specialist in the lithium world. He’s been an authority in lithium for many years starting as one of the first sell side analysts to take apart the EV forecasts as the story was unfolding for the future demand of lithium.

So, again, what Altius decided, in this case, is to partner with some really smart people who had the groundwork laid and had the best-in-class assets sized up and deals templated. We are investing basically side by side with them through an equity position into that company and our royalty co-vestment rights are pro rata with our equity ownership. But we can pick and choose which ones we actually fund – we don’t have to participate in every one of them, and in fact, haven’t participated in every one so far.It is a different way for us to do it, as typically we’ve always been the front men running our own ship, whether it’s a particular jurisdiction or a particular commodity or a particular idea. In this case, we weren’t the first men running, so we partnered with the first man running.

Brian: Warren Buffett is famous for saying, “You must learn from mistakes, but they don’t have to be your own.” I was wondering if you could parlay that into the 20-year history of Altius.

Are there any lessons in particular that stand out to you?

Chad: Absolutely. It’s all lessons. I’ll focus on my side of the business, exploration and project generation. In the last bull cycle, we made $200 million plus through our project generation efforts. How did we do that?

We took geological real estate that we had generated with boot and hammer prospecting and came up with big context and big ideas. Then, we effectively sold it on to a third party. In the case of where we made the money selling on to a third party, it was a market participant. What we did is we exchanged geological real estate which is generally illiquid for shares in a fairly liquid company on a stock exchange, versus up until that point in time, let’s say the first 10 years of Altius, we spent a lot of our time doing exploration deals with major miners.

Though that gave us a lot of technical credibility in the product that we generated and we were able to attract those third party endorsements, it was an illiquid business. What I mean is that even though you did a deal, you weren’t able to monetize your minority residual stake in the assets.

So the big learning experiment that we had when we look back at the last bull cycle is related to the way that we made money, it was actually trading geological real estate for shares. So when we enter this bull cycle, I don’t know that I’d call it a bull cycle yet, the phone started to ring. All of a sudden, here we were as an exploration group, we had assembled projects in nine jurisdictions globally from 2012 to 2016, when nobody gave a crap about the mining resources business, and certainly weren’t doing exploration. We were able to waltz into world-class jurisdictions, build meaningful land positions, generated a lot of geological real estate, and basically we sat on it and waited for the market to turn.

Since that time, we’ve sold 54 (working on 57!) projects and 17 different agreements in less than 24 months. It’s been extraordinary. I didn’t think it could get so good for us. Every deal we’ve done, except for one that we haven’t announced yet, is that we took our geological real estate, we’d trade it for shares in a third party junior company, or in special circumstances, we even facilitated the IPO of new entities.

Where at the same time, though, where did we end up? We ended up with a big share position in a company that now held the assets that we generated, while at the same time we retained blanket royalties to the underlying projects. Long term sewed up in terms of the mining operations, we get kicked back on our royalties, while at the same time, we’re so early into the cycle we’re effectively getting seed stock in juniors that go to explore our projects.

So these positions expose us to discovery opportunity off of our balance sheet, on somebody else’s balance sheet, at the seed level. It’s beautiful! So if you look at our juniors portfolio today, we’re sitting on 27 juniors with a value of about $65 million at the end of September.

I can’t make a promise, but I’ll say to you I have extraordinary belief that that $65 million will be worth the market capitalization value of the entirety of Altius, roughly $600 million, through the cycle.

We’re seeded up on the right deals, at the right time, in the right commodities and right projects that those things are going to deliver value.

It’s a cyclical business, you need to be able to, to some degree, trade those cycles. We’ve been able to create fundamentally long-term royalties that punch through the cycles, that we can realize on over 10, 20, 30 year increments. At the same time, we’re getting seeded up on equity that we can monetize and put a big surplus of cash into the bank, so when the market rolls over again, we can put it to work.

So, really, it was about realizing it’s all about liquidity and timing.

Brian: That’s a great answer.

The ramifications of confirmation bias should be a major concern for all investors, as human nature dictates that we love to reaffirm our beliefs with confirming evidence. As a manager, the same concern can be said for “yes” men; people who continually support the boss regardless of whether they think they are right.

Personally, in my career as a manager in steel manufacturing, I quickly learned how important it was to surround myself with people who weren’t afraid to tell me what they thought about the projects that were being proposed or the direction that I wanted to take.

In your experience, how important is it to find or listen to disconfirming information?

Chad: The resources sector more than in any other, you shouldn’t run with the herd. You have to go against it. The reality is that this business in general – exploring, mine development, mine construction, mine production – is extremely tough and tedious.

Additionally, you’ve got to realize that there’s a lot of different tiers and categories of humans that benefit from a story advancing versus not advancing. So, a lot of times, you’re always encouraged to keep spending and spending and spending, because to some degree it’s the mentality to keep things going.

We don’t get into that type of philosophy. We’re a group that sticks to our guns, and believes in our own reasoning and rational. At the end of the day, it’s about relying upon your own technical expertise and surrounding yourself with the right people that are willing to give you the right opinion that is unbiased, genuine and legit.

The resource sector is like no other, it is feast or famine, it’s a herd mentality. To succeed you have to genuinely and truly be a contrarian. You have to be a no man versus a yes man.

Concluding Remarks

Altius Minerals is the cornerstone of my personal portfolio and will remain that way for the foreseeable future. In Altius, I see minimal downside risk outside of a broader market crash, which, in reality, would negatively affect just about every company’s share price.

Further, the upside potential from their project generation business looks very promising. First, looking at their development stage royalties projects: Excelsior Mining’s Gunnison copper project, Alderon Iron Ore’s Kami project or Evrim’s Cuale project, there is a lot of potential cash flow that could be soon flowing in Altius’ direction.

On the exploration side of their equity portfolio, you have Adventus Zinc Corporation (ADZN:TSXV), Aethon Minerals (AET:TSXV), Antler Gold (ANTL:TSXV), and Sokomon Iron (SIC:TSXV) to name just a few. Additionally, you have their latest spin out, Adia Resources, which is partnered with De Beers in the exploration for diamonds in Manitoba.

There are no guarantees in life, however, I believe that if you look at the short and long-term prospects of Altius, I think you will agree that they look tremendously bright.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I do own shares in Altius Minerals, Adventus Zinc Corporation, Aethon Minerals, and LIORC. All Altius Minerals analytics were taken from their website and press releases. I have NO business relationship with Altius Minerals or any of the other companies mentioned in this article.

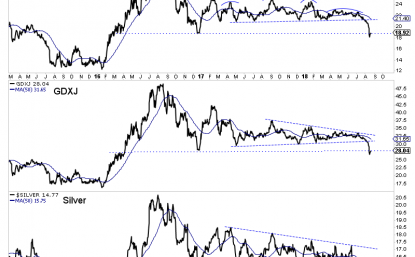

The major silver miners’ stocks have been largely abandoned this year, spiraling to brutal multi-year lows. Such miserable technicals have exacerbated the extreme bearishness plaguing this tiny contrarian sector. While profitable silver mining is challenging at today’s exceedingly-low silver prices, these miners are chugging along. Their recently-reported Q3’18 results show their earnings are ready to soar as silver recovers.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the US Securities and Exchange Commission by 40 calendar days after quarter-ends. Canadian companies have similar requirements at 45 days. In other countries with half-year reporting, many companies still partially report quarterly.

Unfortunately the universe of major silver miners to analyze and invest in is pretty small. Silver mining is a tough business both geologically and economically. Primary silver deposits, those with enough silver to generate over half their revenues when mined, are quite rare. Most of the world’s silver ore formed alongside base metals or gold. Their value usually well outweighs silver’s, relegating it to byproduct status.

The Silver Institute has long been the authority on world silver supply-and-demand trends. It published its latest annual World Silver Survey covering 2017 in mid-April. Last year only 28% of the silver mined around the globe came from primary silver mines! 36% came from primary lead/zinc mines, 23% copper, and 12% gold. That’s nothing new, the silver miners have long produced less than a third of world mined supply.

It’s very challenging to find and develop the scarce silver-heavy deposits supporting primary silver mines. And it’s even harder forging them into primary-silver-mining businesses. Since silver isn’t very valuable, most silver miners need multiple mines in order to generate sufficient cash flows. Traditional major silver miners are increasingly diversifying into gold production at silver’s expense, chasing its superior economics.

So there aren’t many major silver miners left out there, and their purity is shrinking. The definitive list of these companies to analyze comes from the most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. In mid-November at the end of Q3’s earnings season, SIL’s net assets were running 6.6x greater than its next-largest competitor’s. So SIL continues to dominate this tiny niche contrarian sector.

While SIL has its flaws, it’s the closest thing we have to a silver-stock index. As ETF investing continues to eclipse individual-stock picking, SIL inclusion is very important for silver miners. It grants them better access to the vast pools of stock-market capital. Differential SIL-share buying by investors requires this ETF’s managers to buy more shares in its underlying component companies, bidding their stock prices higher.

In mid-November as the silver miners were finishing reporting their Q3’18 results, SIL included 23 “Silver Miners”. Unfortunately the great majority aren’t primary silver miners, most generate well under half their revenues from silver. That’s not necessarily an indictment against SIL’s stock picking, but a reflection of the state of this industry. There aren’t enough significant primary silver miners left to fully flesh out an ETF.

This disappointing reality makes SIL somewhat problematic. The only reason investors would buy SIL is they want silver-stock exposure. But if SIL’s underlying component companies generate just over a third of their sales from silver mining, they aren’t going to be very responsive to silver price moves. And most of that ETF capital intended to go into primary silver miners is instead diverted into byproduct silver miners.

So silver-mining ETFs sucking in capital investors thought they were allocating to real primary silver miners effectively starves them. Their stock prices aren’t bid high enough to attract in more investors, so they can’t issue sufficient new shares to finance big silver-mining expansions. This is exacerbating the silver-as-a-byproduct trend. Only sustained much-higher silver prices for years to come could reverse this.

Silver miners’ woes are really exacerbated by silver’s worst performance in decades. In mid-November silver sunk to a 2.8-year low of $13.99. That naturally dragged down SIL to a similar 2.7-year low. But relative to gold which usually drives it, silver was faring far worse. The Silver/Gold Ratiosunk to 85.9x in mid-November, meaning it took almost 86 ounces of silver to equal the value of a single ounce of gold.

The SGR hadn’t been lower, or silver hadn’t been more undervalued relative to gold, since all the way back in March 1995! That’s pretty much forever from a markets perspective. With silver languishing at an exceedingly-extreme 23.7-year low relative to gold, it’s hard to imagine it doing much worse. So the silver miners are weathering one of the toughest environments they’ve ever seen, which we have to keep in mind.

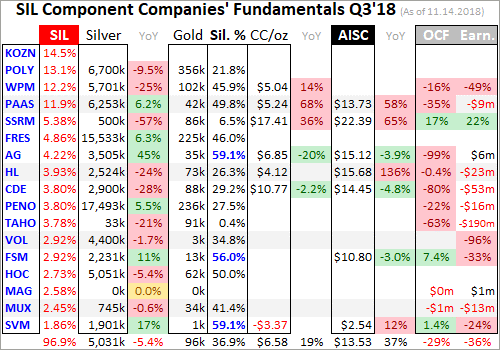

Every quarter I dig into the latest results from the major silver miners of SIL to get a better understanding of how they and this industry are faring fundamentally. I feed a bunch of data into a big spreadsheet, some of which made it into the table below. It includes key data for the top 17 SIL component companies, an arbitrary number that fits in this table. That’s a commanding sample at 96.9% of SIL’s total weighting!

While most of these top 17 SIL components had reported on Q3’18 by mid-November, not all had. Some of these major silver miners trade in the UK or Mexico, where financial results are only required in half-year increments. If a field is left blank in this table, it means that data wasn’t available by the end of Q3’s earnings season. Some of SIL’s components also report in gold-centric terms, excluding silver-specific data.

The first couple columns of this table show each SIL component’s symbol and weighting within this ETF as of mid-November. While most of these stocks trade on US exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each miner’s Q3’18 silver production in ounces, along with its absolute year-over-year change. Next comes this same quarter’s gold production.

Nearly all the major silver miners in SIL also produce significant-to-large amounts of gold! That’s truly a double-edged sword. While gold really stabilizes and boosts silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. So the next column reveals how pure these elite silver miners are, approximating their percentages of Q3’18 revenues actually derived from silver. This is calculated two ways.

The large majority of these top SIL silver miners reported total Q3 revenues. Quarterly silver production multiplied by silver’s average price in Q3 can be divided by these sales to yield an accurate relative-purity gauge. When Q3 sales weren’t reported, I estimated them by adding silver sales to gold sales based on their production and average quarterly prices. But that’s less optimal, as it ignores any base-metals byproducts.

Next comes the major silver miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated and hard GAAP earnings, with a couple exceptions necessary.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. This whole dataset together offers a fantastic high-level read on how the major silver miners are faring fundamentally as an industry. They are hanging in there quite well.

Production is naturally the lifeblood of the silver-mining sector. The more silver and increasingly gold that these elite miners can wrest from the bowels of the earth, the stronger their fundamental positions and outlooks. These top 17 SIL miners’ overall silver production slipped 2.2% YoY to 75.5m ounces in Q3’18. But their shift into more-profitable gold mining continued, with aggregate production up 1.6% YoY to 1.4m ounces.

According to the Silver Institute’s latest WSS, total world silver mine production averaged 213.0m ounces per quarter in 2017. So at 75.5m in Q3, these top 17 SIL components were responsible for 35.4% of that rate. There is one unusual situation that slightly skewed this result. SSR Mining, which used to be known as Silver Standard Resources, saw its silver production plummet 57% YoY as its lone silver mine is depleting.

The winding down of SSRM’s old Pirquitas silver mine is proceeding as forecast and has been going on for some time. This once major silver miner is morphing into a primary gold miner, which accounted for a record 94% of its revenue in Q3. Excluding SSRM, the rest of these top SIL silver miners saw their silver production retreat an immaterial 1.3% YoY. That’s pretty impressive given this year’s collapse in silver prices.

Q3’s average silver price was just $14.96, down a major 11.2% YoY. That was far-worse performance than gold, with its quarterly average merely sliding 5.3% lower between Q3’17 to Q3’18. Considering how miserable this silver-price environment is with the worst relative performance to gold in decades, the major silver miners are doing well on production. They continue to hold out for silver mean reverting higher.

Silver is likely so down in the dumps because it effectively acts like a gold sentiment gauge. Generally big silver uplegs only happen after gold has rallied long enough and high enough to convince traders its gains are sustainable. Then the way-smaller silver market tends to start leveraging and amplifying gold’s moves by 2x to 3x. But gold sentiment was so insipid over this past year that no excitement was sparked for silver.

Unfortunately at these bombed-out silver prices the economics of silver mining are way inferior to gold mining. The traditional major silver miners are painfully aware of this, and have spent years actively diversifying into gold. In Q3’18, the average percentage of revenues that these top 17 SIL miners derived from silver was just 36.9%. That’s right in line with the prior 4 quarters’ 39.3%, 35.3%, 36.8%, and 36.3%.

Silver mining is every bit as capital-intensive as gold mining, requiring similar large expenses for planning, permitting, and constructing mines and mills. It needs similar heavy excavators and haul trucks to dig and move the silver-bearing ore. Similar levels of employees are necessary to run these mines. But silver generates much lower cash flows due to its lower price. Consider hypothetical mid-sized silver and gold mines.

They might produce 10m and 300k ounces annually. At last quarter’s average prices, these silver and gold mines would yield $150m and $363m of yearly sales. Thus regrettably it is far easier to pay the bills mining gold these days. So primary silver miners are increasingly becoming a dying breed, which is sad. The traditional major silver miners are adapting by ramping their gold production often at silver’s expense.

With major silver miners so rare, SIL’s managers are really struggling to find components for their leading ETF. So in Q3’17 they added Korea Zinc, which is now SIL’s largest component at over 1/7th of its total weighting. In my decades of studying and trading this tiny sector, I’d never heard of it. So I looked into Korea Zinc and found it was merely a smelter, not even a miner. It really needs to be kicked out of SIL.

Every quarter since I’ve tried to dig up information on Korea Zinc, but its English-language disclosures are literally the worst I’ve ever seen for any company. Its homepage gives an idea of what to expect, declaring “We are Korea Zinc, the world’s one of the best smelting company”. I’ve looked and looked and the latest production data I can find in English remains 2015’s. I can’t find it from third-party sources either.

That year Korea Zinc “produced” 63.3m ozs of silver, which averages to 15.8m quarterly. That is largely a byproduct from its main businesses of smelting zinc, lead, copper, and gold. Korea Zinc certainly isn’t a major silver miner, and has no place in a “Silver Miners ETF”. No silver-stock investor wants to own a base-metals smelter! Korea Zinc should be removed, its overweighting reallocated to the rest of SIL’s holdings.

SIL investors ought to contact Global X to ask them to stop tainting their ETF’s utility and desirability with Korea Zinc. If they want it to be successful and grow, they need to stick with their mission of owning the major silver miners exclusively. Silver-stock exposure is the only reason investors would buy SIL. There is another situation investors need to be aware of with Tahoe Resources and its held-hostage Escobal mine.

Tahoe was originally spun off by Goldcorp to develop the incredible high-grade Escobal silver mine in Guatemala, which went live in Q4’13. Everything went well for its first few years. By Q1’17, Escobal was a well-oiled machine producing 5700k ounces of silver. That provided 1000+ great high-paying jobs to locals and contributed big taxes to Guatemala’s economy. Escobal was a great economic boon for this country.

But a radical group of anti-mining activists managed to spoil everything, cruelly casting their fellow countrymen out of work. They filed a frivolous and baseless lawsuit against Guatemala’s Ministry of Energy and Mines, Tahoe wasn’t even the target! It alleged this regulator hadn’t sufficiently consulted with the indigenous Xinca people before granting Escobal’s permits. They don’t even live around this mine site.

Only in a third-world country plagued with rampant government corruption would a regulator apparently not holding enough meetings be a company’s problem. Instead of resolving this, a high Guatemalan court inexplicably actually suspended Escobal’s mining license in early Q3’17! Tahoe was forced to temporarily mothball its crown-jewel silver mine, and thus eventually lay off its Guatemalan employees.

That license was technically reinstated a couple months later, but the activists appealed to a higher court. It required the regulator to study the indigenous people in surrounding areas and report back, and then needs to make a decision. The government also needs to clear out an illegal roadblock to the mine site by violent anti-mine militants, who have blockaded Escobal supplies and physically attacked trucks and drivers!

So Escobal has been dead in the water with zero production for 5 quarters now, an unthinkable outcome. This whole thing is a farce, a gross miscarriage of justice. I hope this isn’t a stealth expropriation, that Guatemalan bureaucrats will get their useless paperwork done sooner or later and let Escobal come back online. Within a year, Escobal’s silver production should return to pre-fiasco levels of 5700k ounces a quarter.

At that rate, Escobal would retake the throne of being the world’s largest primary silver mine! It would boost overall SIL-top-17 production by a massive 7.6%. Last year no one expected this unprecedented Escobal debacle to last very long, as the economic damage to Guatemala was too great. But as it drags on and on, TAHO stock has been decimated. It slumped to a brutal all-time record low in mid-November.

Sadly for long-suffering TAHO shareholders, management capitulated. In mid-November they agreed to sell the company to Pan American Silver at rock-bottom prices despite a 55% premium over that all-time low. That’s devastating for TAHO investors but a steal for PAAS, which is SIL’s 4th-largest component at 11.9% of its total weighting. That keeps Escobal’s huge production in SIL if PAAS can finesse its reopening.

Unfortunately SIL’s mid-November composition was such that there wasn’t a lot of Q3 cost data reported by its top component miners. A half-dozen of these top SIL companies trade in South Korea, the UK, Mexico, and Peru, where reporting only comes in half-year increments. There are also primary gold miners that don’t report silver costs, and a silver explorer with no production. So silver cost data remains scarce.

Nevertheless it’s always useful to look at what we have. Industrywide silver-mining costs are one of the most-critical fundamental data points for silver-stock investors. As long as the miners can produce silver for well under prevailing silver prices, they remain fundamentally sound. Cost knowledge helps traders weather this sector’s left-for-dead unpopularity without succumbing to selling low like the rest of the herd.

There are two major ways to measure silver-mining costs, classic cash costs per ounce and the superior all-in sustaining costs. Both are useful metrics. Cash costs are the acid test of silver-miner survivability in lower-silver-price environments, revealing the worst-case silver levels necessary to keep the mines running. All-in sustaining costs show where silver needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of silver, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q3’18, these top 17 SIL-component silver miners that reported cash costs averaged $6.58 per ounce. While that surged 35.3% YoY, it still remains far below today’s anomalously-low silver prices.

There are a couple of extreme cash-cost outliers that are skewing this average, but offsetting each other. SSRM’s depleting silver mine is producing less with each passing quarter, forcing fewer ounces to bear the fixed costs of mining. Its crazy-high $17.41 per ounce in Q3 isn’t normal. But on the other side of this is Silvercorp Metals, which produces silver in Chinese mines yielding enormous base-metals byproducts.

Selling those and crediting their value across the silver ounces mined dragged down SVM’s cash costs to an unbelievable negative $3.37 in Q3! Excluding these extreme outliers, the rest of the SIL top 17 saw average cash costs of $6.40. That’s not too far above the past 4 quarters’ $4.86, $4.66, $5.05, and $3.95. As long as silver prices remain over those low levels, the silver miners can keep the lights on at their mines.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain silver mines as ongoing concerns. AISCs include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current silver-production levels.

These additional expenses include exploration for new silver to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee silver mines. All-in sustaining costs are the most-important silver-mining cost metric by far for investors, revealing silver miners’ true operating profitability.

In Q3’18 these top 17 SIL miners reporting AISCs averaged $13.53 per ounce, which also surged 39.0% YoY. Again that was skewed in both directions by SSRM’s extremely-high $22.39 on Pirquitas’ depletion and SVM’s exceedingly-low $2.54 on those huge base-metals byproducts. Without them, the rest of the top 17 averaged $13.96 AISCs. That was much higher than the past 4 quarters’ $9.73, $10.16, $10.92, and $10.93.

The lower production was definitely a factor, which is inversely proportional to per-ounce costs. Silver-mining costs are largely fixed quarter after quarter, with actual mining requiring roughly the same levels of infrastructure, equipment, and employees. So the lower production, the fewer ounces to spread mining’s big fixed costs across. The major silver miners also reported lower ore grades, exacerbating the decline.

Nevertheless, the top 17 SIL miners’ AISCs both with and without the outliers still remained under silver’s weak average $14.96 price in Q3. So even with silver faring its worst relative to gold in decades thanks to devastated sentiment, the silver mines were profitable. And interestingly the closer AISCs crowd the prevailing silver prices, the more profits leverage the miners have to silver mean reverting much higher.

In mid-November silver and SIL slumped to their lowest levels since back in January and March 2016. That was early in a new silver bull which emerged from conditions like today’s where silver was despised. Over 7.6 months between December 2015 and August 2016, silver soared 50.2% higher as gold surged in its own new bull. And with silver moving again, investors eagerly started returning to the battered silver stocks.

Thanks to that silver-bull upleg, SIL skyrocketed 247.8% higher in just 6.9 months in essentially that first half of 2016! That ought to give embattled silver-stock investors some hope. All it will take to turn silver stocks around is a typical gold-driven silver upleg, and then they will soar again. The reason that silver miners’ stocks blast dramatically higher with silver is their high inherent profits leverage to silver prices.

Assume another 50% silver upleg, which is pathetically small by historical standards, from silver’s recent secular low in mid-November. That would catapult silver back up to $21 per ounce for the first time since July 2014. At Q3’18’s top-17-SIL-stock average AISCs of $13.53, profits were just $0.47 per ounce at $14 silver. But at $21 assuming stable AISCs, they would soar an astounding 1489% higher to $7.47 per ounce!

You better believe silver-stock prices would skyrocket with that kind of earnings growth. The higher their AISCs, the greater their upside profits leverage. Now consider this same 50% silver upleg using the rolling-past-4-quarter top-17-SIL-stock average AISCs of $10.43 per ounce. That implies the $3.57 profit seen at $14 silver would only balloon 196% to $10.57 per ounce at $21 silver. So higher costs aren’t necessarily bad.

As long as AISCs are below prevailing silver prices, the major silver miners can weather anything. The closer their AISCs creep to silver, the greater their earnings growth when silver mean reverts higher. So the major silver miners’ upside from here is truly explosive as silver recovers, just like back in early 2016. And silver will power much higher soon as the record silver-futures shorts of early September continue to be covered.

While all-in sustaining costs are the single-most-important fundamental measure that investors need to keep an eye on, other metrics offer peripheral reads on the major silver miners’ fundamental health. The more important ones include cash flows generated from operations, GAAP accounting profits, revenues, and cash on hand. As you’d expect given the miserably-low silver prices, they were on the weak side in Q3.

Operating cash flows among these SIL top 17 reporting them fell 23.0% YoY to $830m, which is totally reasonable given the 2.2%-lower silver production and 11.2%-lower average silver prices. Sales fell 9.5% YoY to $2717m, with some of the silver-side weakness offset by the 1.6%-higher gold production. And cash on hand fell 9.8% YoY to a still-hefty $2419m, giving these silver miners plenty of capital to weather this storm.

The hard GAAP accounting profits looked pretty ugly though, plunging to a $243m loss from being $88m in the black in Q3’17. But most of those losses didn’t reflect operations. TAHO alone wrote off a massive $170m for the impairment of Escobal, which reflected an estimated restart date of the end of 2019. Coeur Mining reported a smaller $19m writedown for one of its mines. These two non-cash charges alone were $189m.

Without them GAAP profits would’ve sunk from $88m in Q3’17 to a milder $54m loss in Q3’18. That’s still poor, but not unexpected given the lowest silver prices seen in almost several years. Again silver-mining earnings will soar if not skyrocket as silver inevitably mean reverts higher from here. All it takes for silver to surge in major bull-market uplegs is for gold itself to power higher, and huge gold upleg fuel abounds now.

The silver-mining stocks are doing way better fundamentally than they’ve been given credit for. Their higher Q3’18 mining costs still remained below the recent deep silver lows. And the compressed gap between their AISCs and low prevailing silver prices guarantees epic profits upside as silver recovers and mean reverts higher. That will attract back investors fast, catapulting silver stocks up sharply like in early 2016.

While traders can play that in SIL, this ETF has problems. Its largest component is now a base-metals smelter of all things! And the great majority of its stocks are primary gold miners with byproduct silver production. The best gains by far will be won in smaller purer mid-tier and junior silver miners with superior fundamentals. A carefully-handpicked portfolio of these miners will generate much-greater wealth creation.

The key to riding any silver-stock bull to multiplying your fortune is staying informed, both about broader markets and individual stocks. That’s long been our specialty at Zeal. My decades of experience both intensely studying the markets and actively trading them as a contrarian is priceless and impossible to replicate. I share my vast experience, knowledge, wisdom, and ongoing research through our popular newsletters.

Published weekly and monthly, they explain what’s going on in the markets, why, and how to trade them with specific stocks. They are a great way to stay abreast, easy to read and affordable. Walking the contrarian walk is very profitable. As of Q3, we’ve recommended and realized 1045 newsletter stock trades since 2001. Their average annualized realized gains including all losers is +17.7%! That’s double the long-term stock-market average. Subscribe today and take advantage of our 20%-off holidays sale!

The bottom line is the major silver miners’ fundamentals remain solid based on their recently-reported Q3’18 results. They continue to mine silver at all-in sustaining costs below even mid-November’s deep silver lows. Their profits will multiply dramatically as silver rebounds higher driven by gold’s own upleg and record silver-futures short covering. Investment capital will flood back in, catapulting silver stocks up violently.

So traders need to look through the recent forsaken herd sentiment to understand the silver miners’ hard fundamentals. These left-for-dead stocks are seriously undervalued even at today’s low silver prices, let alone where silver heads during the next major gold upleg. Silver can’t languish at extreme anomalous multi-decade lows relative to gold for long. And once it catches a bid, silver stocks will really amplify its upside.

The major gold miners’ stocks remain mired in universal bearishness, largely left for dead. They are just wrapping up their third-quarter earnings season, which proved challenging. Lower gold prices cut deeply into cash flows and profits, and production-growth struggles persisted. But these elite companies did hold the line on costs, portending soaring earnings as gold recovers. Their absurdly-cheap stock prices aren’t justified. Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the U.S. Securities and Exchange Commission by 40 calendar days after quarter-ends. Canadian companies have similar requirements at 45 days. In other countries with half-year reporting, many companies still partially report quarterly.

These quarterlies offer the best fundamental data available for individual major gold miners, showing how their operations are really faring. That helps dispel the thick obscuring fogs of sentiment that billow up the rest of the time. While I always eagerly anticipate perusing these key reports, I worried what this Q3’18 earnings season would reveal. Lower gold prices, flagging production, and weak sentiment are a witches’ brew.

The definitive list of major gold-mining stocks to analyze comes from the world’s most-popular gold-stock investment vehicle, the GDX VanEck Vectors Gold Miners ETF. Its composition and performance are similar to the benchmark HUI gold-stock index. GDX utterly dominates this sector, with no meaningful competition. This week GDX’s net assets are 50.5x larger than the next-biggest 1x-long major-gold-miners ETF!

GDX is effectively the gold-mining industry’s blue-chip index, including the biggest and best publicly-traded gold miners from around the globe. GDX inclusion is not only prestigious, but grants gold miners better access to the vast pools of stock-market capital. As ETF investing continues to rise, capital inflows into leading sector ETFs require their managers to buy more shares in underlying component companies.

My earnings-season trepidation soared on October 25th. The gold stocks were doing fairly well then, with GDX rallying 14.4% out of mid-September’s deep forced-capitulation lows . Sentiment was slowly improving. But that day GDX plunged 4.4% out of the blue, and the flat gold price at upleg highs certainly wasn’t the driver. The most-loved major gold miner had plummeted after reporting shockingly-bad Q3 results. Goldcorp has always been one of GDX’s top components. It reported mining just 503k ounces of gold last quarter, which plunged 11.9% sequentially quarter-on-quarter and 20.5% year-over-year! That forced its all-in sustaining costs a proportional 20.8% higher YoY to $999 per ounce. Investors panicked and fled, hammering GG stock 18.7% lower. That was the worst down day in the 24.6-year history of this company.

That left it at an extreme 16.2-year low! GG hadn’t been lower since August 2002 when gold was still in the low $300s, it was apocalyptic. That really torpedoed still-fragile sentiment in this sector, even though GG’s woes looked short-lived. It was bringing a new expansion online at one of its big mines, which was what caused the shortfall. Now in Q4’18 Goldcorp expects production to rebound to 620k ounces at $750 AISCs.

After GG’s Q3 disaster, I worried frayed investors would dump other gold stocks on any hints of less-than-optimal quarterly results. But GDX has ground sideways on balance since that GG shock, weathering this risky earnings season with sentiment so fragile. Ever since I’ve been anxious to analyze the collective Q3 results of the major gold miners as a whole, to see if GG’s travails were unique to it or more systemic.

GDX’s component list this week ran 48 “Gold Miners” long. While the great majority of GDX stocks do fit that bill, it also contains gold-royalty companies and major silver miners. All the world’s big primary gold miners publicly traded in major markets are included. Every quarter I look into the latest operating and financial results of the top 34 GDX companies, which is just an arbitrary number fitting neatly into these tables.

That’s a commanding sample, as GDX’s 34 largest components now account for a whopping 93.5% of its total weighting! These elite miners that reported Q3’18 results produced 296.4 metric tons of gold, which accounts for fully 33.9% of last quarter’s total global gold production. That ran 875.3t per the recently-released Q3’18 Gold Demand Trends report from the World Gold Council. I’ll discuss production more below.

Most of these top 34 GDX gold miners trade in the U.S. and Canada where comprehensive quarterly reporting is required by regulators. But some trade in Australia and the U.K., where companies just need to report in half-year increments. Fortunately those gold miners do still tend to issue production reports without financial statements each quarter. There are still wide variations in reporting styles and data offered.

Every quarter I wade through a ton of data from these major gold miners’ latest results and dump it into a big spreadsheet for analysis. The highlights make it into these tables. Blank fields mean a company had not reported that data for Q3’18 as of this Wednesday. Looking at the major gold miners’ latest results in aggregate offers valuable insights on this industry’s current fundamental health unrivaled anywhere else.

The first couple columns of these tables show each GDX component’s symbol and weighting within this ETF as of this week. While most of these stocks trade on US exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each gold miner’s Q3’18 production in ounces, which is mostly in pure-gold terms. That excludes byproduct metals often present in gold ore. Those are usually silver and base metals like copper, which are valuable. They are sold to offset some of the considerable costs of gold mining, lowering per- ounce costs and thus raising overall profitability. In cases where companies didn’t separate out gold and lumped all production into gold-equivalent ounces, those GEOs are included instead. Then production’s absolute year-over-year change from Q3’17 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, revenues, and cash on hand with a couple exceptions. Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. This whole dataset together offers a fantastic high-level read on how the major gold miners are faring fundamentally as an industry. Was Goldcorp’s disaster systemic?

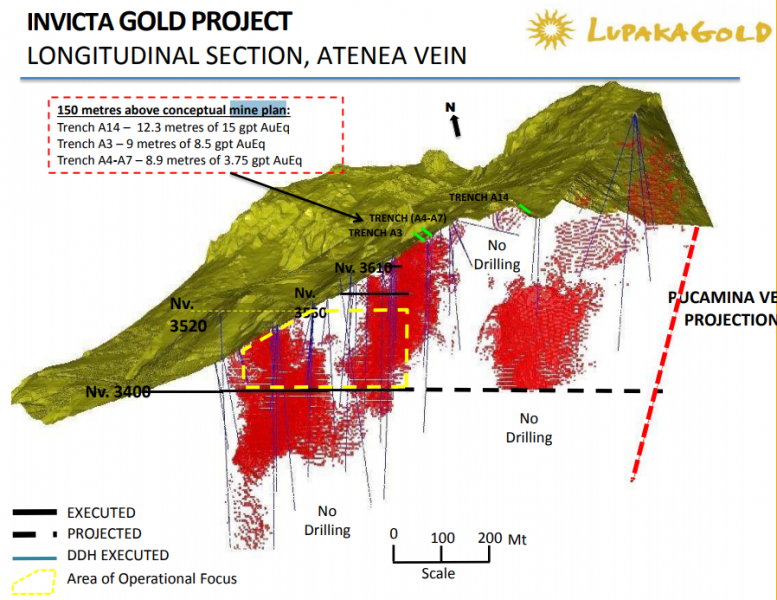

Lupaka Gold’s (TSX-V: LPK) Invicta Gold Project is on the brink of production, set to become Peru’s next producing gold mine.

However, everything is not going to plan…for the better.

What has been quietly observed is that (1) the grades are coming in higher than the PEA and (2) the company is already making plans to increase production above the PEA throughout rate of 350 tpd. All this means higher levels of production and cash flow once the actual mining commences later this year.

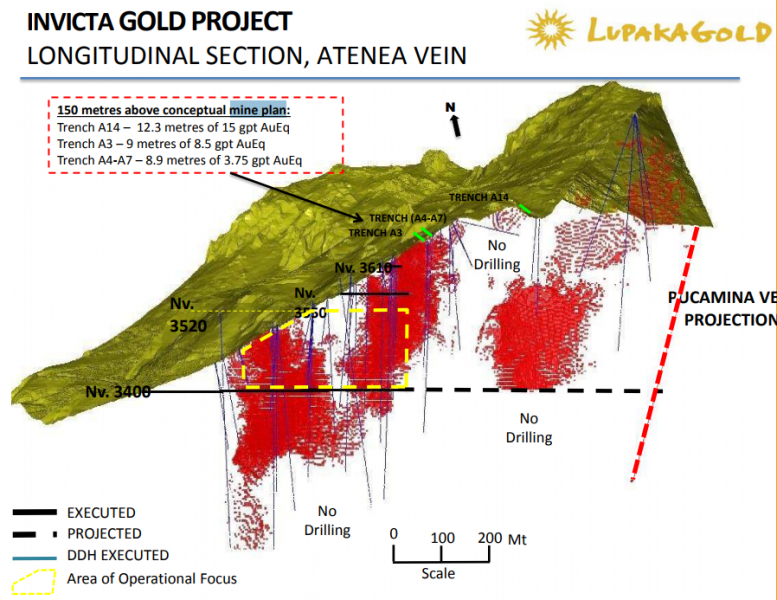

Recent underground sampling of mineralization is revealing an asset that offers more than originally outlined in the company’s April 2018 Preliminary Economic Assessment (“PEA”) which gives investors additional upside for any increases in mine output, improvement of grade and additional ounces to the overall resource.

The April 2018 PEA for the Invicta Mine outlined a mineral resource of 3 million tonnes of Indicated Mineral Resources at 5.78 grams per tonne (“g/t”) gold equivalent (“AuEq”) ounces using a 3.5-g/t cut-off grade (“COG”), and 600,000 tonnes of Inferred Mineral Resources at 5.49 g/t AuEq.

Within that resource the Company has a PEA that outlines an initial 6-year mine life that will produce produce a total of 669,813 tonnes of mineralized material processing 350 tonnes per day (“tpd”) at an average grade of 8.6 g/t Au-Eq. Lupaka’s grades included estimated metallurgical recoveries, and the true grade will likely be even higher than 8.5 g/t AuEq.

Just to highlight, with an all in sustaining cost (“ASIC”) of $575 per gold ounce equivalent, Lupaka Gold will be one of the lowest cost junior producers.

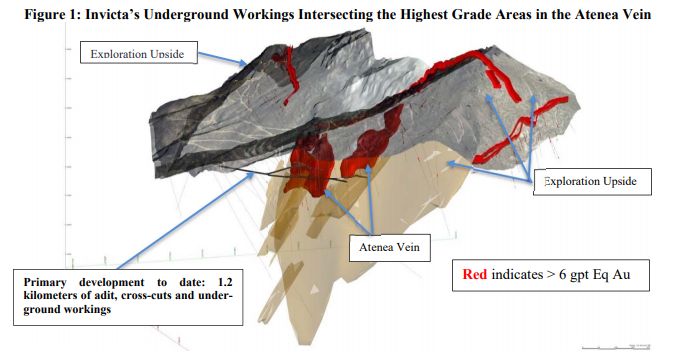

As part of the development work to put Invicta into production, Lupaka has been conducting channel sampling every 5 metres on all workings during development.

The results have demonstrated continuity of the high grade mineralization and additional potential that the Aetnea vein hosts.

In March 2018, the company released preliminary sample results:

Sample assay values over the footwall vein averaged 9.86 g/t AuEq over 130 metres, with an average width of 6.1 metres (“m”);

Sample assay values over the hanging wall split averaged 7.00 g/t AuEq over 70 m, with an average width of 6 m.

In June, Lupaka released further results from a underground sampling program on the newly developed 3430 production sublevel.

9.22 g/tAuEq over a strike length of 130 m, with an average sample width of 4.2 m.

The company provided additional results in July:

Channel sample assay values from across the strike of the Atenea vein, within the raise development, returned an average of 23.45 g/t AuEq over a vertical height of approximately 30 m;

Sampling returned significant grades such as sample number 2606E which returned 227.77 g/t AuEq over a width of 1.2 m.

In addition to the sampling, development and rehabilitation of the Invicta mine has provided ~6,500 tonnes of mineralized material from the 3400 Level and when sampled on surface returned an average grade of 7.21 g/t AuEq.

Grade consistency is always a problem with mining. However, it is appearing that the Invicta PEA outlined a muted gold grade on a smaller area of the known mineralization which does not highlight the potential for higher grade zones and the prospectivity of the area.

Higher grades could improve the bottom line as mining proceeds through the Aetnea vein and into the other zones around the current area of operational focus.

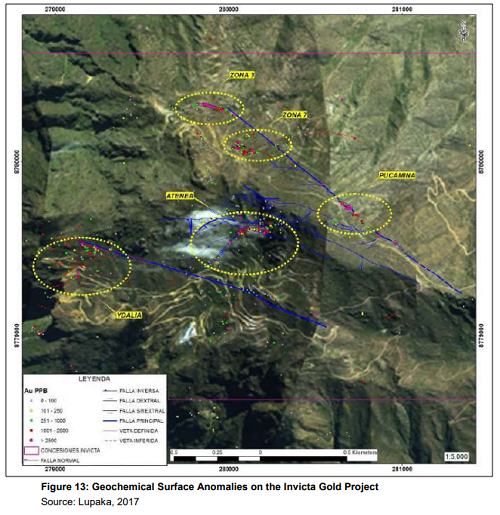

Past exploration at the Invicta mine property indicates that the property has considerable potential for mineral resource expansion through exploration.

Structural studies, geophysical and geochemical work conducted to date strongly suggest the potential for mineral resource expansion along existing mineralized structures.

Past sampling around Invicta revealed the exploration potential with many areas reporting grades greater than 6 g/t AuEq. mine

All in all, the focus on a smaller area for the PEA and initial mine plan reveals that the company’s plan has been to bring production online with a well defined resource with the Aetnea vein through underground mining with minimal capital expenditures, rather than trying to finance and build a large scale operation off the back.

With the commencement of limited toll mining in September, and the beginning of full scale production hopefully in October, Lupaka will have the necessary cash flow to conduct exploration and prove up more ounces in the ground and significantly alter the assumptions of the April 2018 PEA to extend the life of mine.

The next milestone is the final mining exploitation licence, which requires an inspection by the Peruvian Ministry of Mines and Energy.

The inspection will be performed before the end of October and upon receipt of the exploitation licence, the company will have the go ahead to produce at a rate of 400 tonnes per day, or 12,000 tonnes per month.

However, with the permit to operate at 400 tpd, the company could see its potential production increase by 14% from the 350 tpd production assumption outlined in the PEA, boosting the project’s cash flow.

Currently, shares in Lupaka gold are trading near year-lows which discounts a years’ worth of work and development that has improved access to the mine, defined a PEA, divestment of non primary assets, cash flow from initial toll mining and on the cusp of full scale mining.

The company laid out a plan to bring into production the Invicta mine with a small area of operational focus and a humble gold grade in comparison to recent sampling.

The plan is working and it is starting to reveal that there is more to the story than initially outlined…a good thing for investors.

*The author of this article was compensated for the creation of this article in cash. The author picked up shares in the public market, ranging from prices of 14 cents to 20 cents over the past year. This article is meant to serve informational and marketing purposes only and not a technical report and does not constitute a buy recommendation. As always, please do your own diligence.

*The Mineral Resource Statement for the Invicta Project is tabulated to a cut-off grade of 3.0 g/t Au-Eq. Cut-off grades are based on a price of US$1,250 per ounce of gold, US$17.00 per ounce of silver, US$3.00 per pound of copper, US$1.05 per pound of lead and US$1.20 per pound of zinc. The equivalent gold calculation assumes mill recoveries of 85 percent for gold, 80 percent for silver, 82 percent for copper and lead and 77 percent for zinc

The major silver miners’ stocks have been thrashed, pummeled to brutal multi-year lows. They suffered serious collateral damage as silver plunged on gold’s breakdown, driven by crazy-extreme all-time-record silver-futures short selling. All this technical carnage left investors reeling, devastating sentiment. The silver miners’ recently-reported Q2’18 results reveal whether their anomalous plunge was justified fundamentally.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the US Securities and Exchange Commission by 45 calendar days after quarter-ends. Canadian companies have similar requirements. In other countries with half-year reporting, many companies still partially report quarterly.

Unfortunately the universe of major silver miners to analyze and invest in is pretty small. Silver mining is a tough business both geologically and economically. Primary silver deposits, those with enough silver to generate over half their revenues when mined, are quite rare. Most of the world’s silver ore formed alongside base metals or gold. Their value usually well outweighs silver’s, relegating it to byproduct status.

The Silver Institute has long been the authority on world silver supply-and-demand trends. It published its latest annual World Silver Survey covering 2017 in mid-April. Last year only 28% of the silver mined around the globe came from primary silver mines! 36% came from primary lead/zinc mines, 23% copper, and 12% gold. That’s nothing new, the silver miners have long supplied less than a third of world mined supply.

It’s very challenging to find and develop the scarce silver-heavy deposits supporting primary silver mines. And it’s even harder forging them into primary-silver-mining businesses. Since silver isn’t very valuable, most silver miners need multiple mines in order to generate sufficient cash flows. Traditional major silver miners are increasingly diversifying into gold production at silver’s expense, chasing its superior economics.

So there aren’t many major silver miners left out there, and their purity is shrinking. The definitive list of these companies to analyze comes from the most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. In mid-August at the end of Q2’s earnings season, SIL’s net assets were running 6.7x greater than its next-largest competitor’s. So SIL continues to dominate this small niche contrarian sector.

While SIL has its flaws, it’s the closest thing we have to a silver-stock index. As ETF investing continues to eclipse individual-stock picking, SIL inclusion is very important for silver miners. It grants them better access to the vast pools of stock-market capital. Differential SIL-share buying by investors requires this ETF’s managers to buy more shares in its underlying component companies, bidding their stock prices higher.

In mid-August as the silver miners were finishing reporting their Q2’18 results, SIL included 23 “Silver Miners”. Unfortunately the great majority aren’t primary silver miners, most generate well under half their revenues from silver. That’s not necessarily an indictment against SIL’s stock picking, but a reflection of the state of this industry. There aren’t enough significant primary silver miners left to fully flesh out an ETF.

This disappointing reality makes SIL somewhat problematic. The only reason investors would buy SIL is they want silver-stock exposure. But if SIL’s underlying component companies generate just over a third of their sales from silver mining, they aren’t going to be very responsive to silver price moves. And most of that ETF capital intended to go into primary silver miners is instead diverted into byproduct silver miners.

So silver-mining ETFs sucking in capital investors thought they were allocating to real primary silver miners effectively starves them. Their stock prices aren’t bid high enough to attract in more investors, so they can’t issue sufficient new shares to finance big silver-mining expansions. This is exacerbating the silver-as-a-byproduct trend. Only sustained much-higher silver prices for years to come could reverse this.

Every quarter I dig into the latest results from the major silver miners of SIL to get a better understanding of how they and this industry are faring fundamentally. I feed a bunch of data into a big spreadsheet, some of which made it into the table below. It includes key data for the top 17 SIL component companies, an arbitrary number that fits in this table. That’s a commanding sample at 95.8% of SIL’s total weighting!

While most of these top 17 SIL components had reported on Q2’18 by mid-August, not all had. Some of these major silver miners trade in the UK or Mexico, where financial results are only required in half-year increments. If a field is left blank in this table, it means that data wasn’t available by the end of Q2’s earnings season. Some of SIL’s components also report in gold-centric terms, excluding silver-specific data.

The first couple columns of this table show each SIL component’s symbol and weighting within this ETF as of mid-August. While most of these stocks trade on US exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each miner’s Q2’18 silver production in ounces, along with its absolute year-over-year change. Next comes this same quarter’s gold production.

Nearly all the major silver miners in SIL also produce significant-to-large amounts of gold! That’s truly a double-edged sword. While gold really stabilizes and boosts silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. So the next column reveals how pure these elite silver miners are, approximating their percentages of Q2’18 revenues actually derived from silver. This is calculated two ways.

The large majority of these top SIL silver miners reported total Q2 revenues. Quarterly silver production multiplied by silver’s average price in Q2 can be divided by these sales to yield an accurate relative-purity gauge. When Q2 sales weren’t reported, I estimated them by adding silver sales to gold sales based on their production and average quarterly prices. But that’s less optimal, as it ignores any base-metals byproducts.

Next comes the major silver miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated and hard GAAP earnings, with a couple exceptions necessary.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. This whole dataset together offers a fantastic high-level read on how the major silver miners are faring fundamentally as an industry. Was their recent plunge righteous?

Production is naturally the lifeblood of the silver-mining sector. The more silver and increasingly gold that these elite miners can wrest from the bowels of the earth, the stronger their fundamental positions and outlooks. These top 17 SIL silver miners failed to increase their mining tempos over this past year. Their collective silver and gold production deteriorated 4.4% and 2.1% YoY to 75.1m and 1327k ounces mined.

According to the Silver Institute’s latest WSS, total world silver mine production averaged 213.0m ounces per quarter in 2017. So at 75.1m in Q2, these top 17 SIL components were responsible for 35.3% of that rate. And their overall production decline last quarter is misleading, heavily skewed by two outliers with unusual situations. Tahoe Resources and SSR Mining reported huge 100.0% and 46.3% YoY production plunges!

Without TAHO and SSRM, the rest of these elite silver miners were able to grow their collective silver production by a decent 2.0% YoY. That’s impressive considering the miserable silver-price environment. Between Q2’17 and Q2’18, the average quarterly silver price slumped 3.9% to $16.51. That was really weak compared to gold, which actually rose 3.9% in quarterly-average terms to $1306 across these quarters.

Silver has always been driven by gold, effectively acting like a gold sentiment gauge. Generally big silver uplegs only happen after gold has rallied long enough and high enough to convince traders its gains are sustainable. Then the way-smaller silver market tends to start leveraging and amplifying gold’s moves by 2x to 3x. But gold sentiment was so insipid over this past year that no excitement was sparked for silver.

Yet the top 17 SIL silver miners excluding TAHO and SSRM were able to buck those silver headwinds to still grow production. That is setting up these companies for stronger profits growth once silver’s price inevitably mean reverts higher. It’s important to understand what’s going on with TAHO and SSRM though, as these are long-time favorites among American investors. TAHO’s silver production should return.

Tahoe was originally spun off by Goldcorp to develop the incredible high-grade Escobal silver mine in Guatemala, which went live in Q4’13. Everything went well for its first few years. By Q1’17, Escobal was a well-oiled machine producing 5700k ounces of silver. That provided 1000+ great high-paying jobs to locals and contributed big taxes to Guatemala’s economy. Escobal was a great economic boon for this country.

But a radical group of anti-mining activists managed to spoil everything, cruelly casting their fellow countrymen out of work. They filed a frivolous and baseless lawsuit against Guatemala’s Ministry of Energy and Mines, Tahoe wasn’t even the target! It alleged this regulator had not sufficiently consulted with the indigenous Xinca people before granting Escobal’s permits. And they don’t even live around this mine site.

Only in a third-world country plagued with rampant government corruption would a regulator apparently not holding enough meetings be a company’s problem. Instead of resolving this, a high Guatemalan court inexplicably actually suspended Escobal’s mining license in early Q3’17! Tahoe was forced to temporarily mothball its crown-jewel silver mine, and thus eventually lay off its Guatemalan employees.

That license was technically reinstated a couple months later, but the activists appealed to a higher court. It required the regulator to study the indigenous people in surrounding areas and report back, and now needs to make a decision. The government also needs to clear out an illegal roadblock to the mine site by violent anti-mine militants, who have blockaded Escobal supplies and physically attacked trucks and drivers!

So Escobal has been dead in the water with zero production for an entire year, an unthinkable outcome. This whole thing is a farce, a gross miscarriage of justice. Sooner or later the Guatemalan bureaucrats will get all their useless paperwork done and Escobal will come back online. After a few quarters or so of spinning back up, Escobal’s silver production should return to pre-fiasco levels around 5700k ounces a quarter.

That would boost SIL’s top 17 components’ current overall silver production by 7.6%. In my decades of intensely researching and actively trading mining stocks, I’ve never seen anything like this Escobal debacle. While TAHO’s cashflows are really impaired without this silver mine which was actually the world’s largest primary, it can weather this nightmare because of its other gold mines that yielded 102.6k ounces in Q2’18.

Thankfully SSR Mining’s silver-production plunge is far less dramatic. This company used to be known as Silver Standard Resources, and its old Pirquitas silver mine is simply depleting as forecast. SSRM is exploring in the area trying to extend the life of this old mine, which was joint-ventured and renamed the Puna Operations. But most of SSRM’s resources are being poured into its far-more-profitable gold mines.

That gold focus among these top silver miners is common across SIL’s components. As the silver-percentage column above shows, most of these elite silver miners are actually primary gold miners by revenue! Only 3 of these 17 earned more than half of their Q2’18 sales from mining silver, and they are highlighted in blue. WPM, PAAS, and TAHO are also top-34 components in the leading GDX gold miners’ ETF!

While they only comprised 7.8% of GDX’s total weighting in mid-August, this highlights how difficult it is to find primary silver miners. SIL’s managers have an impossible job these days with the major silver miners increasingly shifting to gold. They are really scraping the bottom of the barrel to find more silver miners. In Q3’17 they added Korea Zinc, and it’s now SIL’s 3rd-biggest holding with a hefty 11.9% total weighting.

That was intriguing, as I’d never heard of this company after decades deeply immersed in this small silver-mining sector. So I looked into Korea Zinc and found it was merely a smelter, not even a miner! Its English-language disclosures are atrocious, starting with its homepage reading “We are Korea Zinc, the world’s one of the best smelting company”. The latest production data I can find in English is still 2015’s.

That year Korea Zinc “produced” 63.3m ozs of silver, which averages to 15.8m quarterly. That is largely a byproduct from its main businesses of smelting zinc, lead, copper, and gold. The fact SIL’s managers included a company like this that doesn’t even mine silver as a top SIL component shows how rare major silver miners have become. The economics of silver mining at today’s prices are way inferior to gold mining.

The traditional major silver miners are painfully aware of this, and have spent years actively diversifying into gold. In Q2’18, the average percentage of revenues these top 17 SIL miners derived from silver was only 36.3%. That’s right in line with the recent trend, with the prior four quarters seeing 36.1%, 39.3%, 35.3%, and 36.4%. This relatively-low silver exposure is why SIL isn’t as responsive to silver as investors expect.

Silver mining is every bit as capital-intensive as gold mining, requiring similar large expenses for planning, permitting, and constructing mines and mills. It needs similar heavy excavators and haul trucks to dig and move the silver-bearing ore. Similar levels of employees are necessary to run these mines. But silver generates much lower cash flows due to its lower price. Consider hypothetical mid-sized silver and gold mines.

They might produce 10m and 300k ounces annually. At last quarter’s average prices, these silver and gold mines would yield $165m and $392m of yearly sales. Unfortunately it is far easier to pay the bills mining gold these days. So primary silver miners are increasingly becoming a dying breed, which is sad. The traditional major silver miners are adapting by ramping their gold production often at silver’s expense.

This industry’s flagging silver purity and thus deteriorating responsiveness to silver price trends will be hard to reverse. Silver would need to far outperform gold, rocketing higher in one of its gigantic uplegs while gold lags. And it would have to stay relatively strong compared to gold for years after that to entice big capital spending back into primary silver mines. While possible, that seems like a stretch in today’s markets.

Unfortunately SIL’s mid-August composition was such that there wasn’t a lot of Q2 cost data reported by its top component miners. A half-dozen of these top SIL companies trade in the UK, South Korea, Mexico, and Peru, where reporting only comes in half-year increments. There are also primary gold miners that don’t report silver costs, and a silver explorer with no production. So silver cost data remains scarce.