Newmont (NYSE:NEM) has jumped to the number four spot among the world’s most valuable mining companies, following the completion of its non-core asset divestiture program. The company finalized the sale of its Akyem gold mine in Ghana and its Porcupine operation in Canada, bringing in about $850 million in after-tax proceeds before any closing adjustments.

These two transactions mark the final steps in a divestiture strategy Newmont kicked off in February 2024. The overall program aimed to raise $4.3 billion in gross proceeds, with $3.8 billion expected from selling off non-core assets and the remaining $527 million from divesting other investments. With these latest deals completed, Newmont has now shed all six of the non-core operations it initially targeted.

The company’s market position reflects the market’s response. Shares of Newmont have risen 52% since the beginning of the year, significantly outperforming major peers like BHP, Rio Tinto, and Southern Copper, all of which have posted negative returns so far in 2025. On Wednesday, Newmont stock was up 3.1% in midday trading on the New York Stock Exchange, pushing its market capitalization to $63.41 billion.

Discovery Silver acquired the Porcupine asset earlier in January. The operation produced 260,000 ounces of gold in 2023. The Akyem sale was the final divestment in the sequence, completing a process that had been underway for months.

Newmont’s CEO, Tom Palmer, called the completion of the asset sales a milestone for the company, noting that the exit from these non-core assets was a key goal of the restructuring strategy rolled out earlier in the year. Newmont’s divestiture program came during a period of shifting market dynamics and tightening investor focus on capital discipline. Shedding less strategic operations allowed the company to sharpen its focus on higher-return assets and projects.

The company’s rise to fourth place in market value among global mining firms reflects both investor confidence and a stronger financial position, bolstered by the cash generated from the divestitures. The company now trails only BHP, Rio Tinto, and Vale in market capitalization within the mining sector. So far, Newmont has not disclosed any immediate plans for how it will allocate the proceeds from these recent sales. Analysts are watching closely to see whether the miner will increase shareholder returns, reduce debt, or reinvest in core operations. While the broader mining sector has struggled to find solid footing in the first months of 2025, Newmont’s streamlined portfolio and clear execution on its asset sale strategy have helped it stand out.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Gold prices are hovering near record highs, yet the world’s two largest gold producers Barrick Gold (TSX:ABX) and Newmont (TSX:NGT) have struggled to capitalize on the precious metal’s rally. Over the next ten days, both companies will have an opportunity to regain investor confidence as they report earnings, but they face mounting pressure to deliver results that reflect gold’s historic surge.

An Important Earnings Season for Gold Miners

Barrick is set to kick off the industry’s latest earnings season on Wednesday, February 14, followed by Agnico Eagle Mines Ltd. on February 13 and Newmont on February 20. Investors will be watching closely to see if the companies can move beyond the disappointments of the third quarter, when both Barrick and Newmont fell short of Wall Street expectations due to higher-than-expected costs and production challenges.

Gold prices have been on a steady march toward $3,000 per ounce, driven by increased demand for the metal as a safe-haven asset. As of this week, gold is trading at around $2,900 per ounce, putting added pressure on miners to show they can translate higher bullion prices into improved profitability.

“Gold is at $2,900, so the market is now saying, show me the money,”said Imaru Casanova, a portfolio manager at Van Eck Associates. “As the gold price makes fresh highs, the market will be focused on the companies ability to expand margins.”

Gold Stocks Rebound, But Challenges Remain

Gold producers have started to see their stocks recover this year. A Bloomberg index of 10 senior gold miners has surged 31% in 2024, nearly triple the gains seen from spot gold. That recovery is helping the world’s biggest gold miners catch up after an underwhelming 2023, when gold prices climbed 27%, but the index of senior gold miners gained only 11%.

Despite this rally, Barrick and Newmont continue to underperform some of their smaller peers, including Agnico Eagle Mines, which has consistently exceeded earnings expectations. The Toronto-based company benefits from operating the bulk of its mines in Canada, a politically stable jurisdiction compared to some of the regions where Barrick and Newmont operate.

Barrick’s Challenges: Mali Dispute, Operational Setbacks, and Costs

Barrick, the world’s second-largest gold producer, has faced multiple challenges that have weighed on its stock. A major setback has been a dispute with the military rulers of Mali, where the company operates one of its largest mining complexes, Loulo-Gounkoto. In January, Barrick was forced to suspend operations after the Malian government began removing gold from the mine and blocking shipments out of the country.

The company is also dealing with operational difficulties at key mines in Papua New Guinea and the Dominican Republic, as well as persistently high input costs in the United States. In Nevada, Barrick co-owns a massive mining complex with Newmont, and rising costs in the region have made it more difficult for the company to maintain profitability.

Newmont, the world’s largest gold producer, has also struggled with rising costs. Its third-quarter results revealed higher-than-expected spending at operations in Australia, Canada, Peru, and Papua New Guinea. Since then, the Denver-based company has been working to reduce overhead costs and strengthen its balance sheet.

To improve its financial position, Newmont has been selling off assets. Over the past several months, the company has completed a series of asset sales totaling $4.3 billion. These sales have helped Newmont generate cash, but investors are still waiting to see if the company can rein in operational expenses while taking advantage of high gold prices.

High Expectations for the Final Quarter

Both Barrick and Newmont have guided investors to expect a strong final quarter of 2024. Now, they will need to deliver on those promises.

One of the biggest challenges facing gold miners is rising inflation, which has driven up costs for everything from labor to energy to equipment. While high gold prices should, in theory, benefit miners, the reality is that inflationary pressures can erode profit margins if companies fail to control their expenses.

With gold prices at record highs, Barrick and Newmont face a critical moment. Investors will be scrutinizing their earnings reports, production guidance, and cost-control strategies to determine whether these industry giants can capitalize on gold’s rally.

If both companies fail to meet expectations again, it could further frustrate shareholders who have been waiting for a stronger performance. But if they manage to exceed expectations and demonstrate improved efficiency, it could mark a turning point for two of the world’s largest gold miners.

In a major announcement, Newcrest Mining (ASX:NCM) confirmed it has approved a monumental takeover offer from Newmont (NYSE:NEM), a deal estimated to be worth A$28.8 billion ($19.2 billion). This colossal business merger is expected to create the world’s premier gold mining enterprise.

The deal is structured such that Newcrest shareholders will acquire 0.4 shares of Newmont for each Newcrest share they hold. This arrangement allows them to secure 31% ownership in the resultant merged entity, a fact affirmed by the Melbourne-based firm, following a Bloomberg News report from Sunday.

The agreement culminates in an inferred enterprise value for Newcrest of A$28.8 billion, incorporating the net debt. Furthermore, Newcrest is committed to disbursing a franked special pre-completion dividend, reaching up to $1.10 per share. Preceding this agreement, Newcrest had consented to extend Newmont’s due-diligence rights to May 18, post the expiry of an earlier deadline.

Newcrest’s chairman, Peter Tomsett, lauded the transaction, stating, “This transaction will combine two of the world’s leading gold producers, bringing forward significant value to Newcrest shareholders through the recognition of our outstanding growth pipeline.”

The expanded Newmont will possess gold assets spread across the globe from North and South America to Africa, Australia, and Papua New Guinea. The merger also signifies an expanded interest in copper, a critical metal in the clean energy transition.

This transaction could potentially represent the zenith of a rapid five-year consolidation amongst the world’s top gold miners, a trend that took off with Barrick Gold Corp’s $18 billion acquisition of Randgold Resources Ltd. and includes the recent $5.2 billion takeover of Yamana Gold Inc. in March. The announcement of Newmont’s proposal coincides with a time when the spot trading price of bullion is nearing a historic peak, amidst global stagflation concerns.

Newmont initially proposed a $17 billion non-binding bid to its Australian counterpart in February, which was turned down by Newcrest’s board. In April, the US company increased the offer to $19.5 billion, terming it as the best and final offer. Sherry Duhe, Newcrest’s chief executive officer, has stated that the board was ready to endorse the proposal to its shareholders, contingent upon successful due diligence.

The global gold mining industry is grappling with the prospects of stagnant production, increasingly challenging mining deposits, and escalating input costs. These industry hurdles are thought to be a driving force for more mergers and acquisitions, as firms strive for expansion to escalate production and gain efficiencies through economies of scale.

Newcrest’s allure for Newmont extends beyond its five gold mines spanning three continents, as the Australian company generates approximately one-fourth of its revenue from copper. Newmont, currently facing a decade-long slump in gold, has expressed a desire to diversify, aiming for more of the energy-transition metal in its portfolio.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Peru’s Ministry of Energy and Mines recently reported that mining investments increased through November 202 to an accumulated total of $4.6 billion, up from $4.4 billion in 2021. The country has focused on attracting more investments in the sector, which has been a major contributor to its economy.

The final month of the period, November, was the best performing month with the most inflows with a total of $467 million, 7.8% higher than October’s total of $434 million, as reported in the Mining Statistical Bulletin.

The biggest investor was Anglo American (LON:AAL) which invested $964 million in the country in 2022, bringing its share of mining investments to 20.9% for the year. The company’s share is the biggest in the sector in Peru. The runner-up was Minera Antamina, owned by BHP, Glencore, Mitsubishi, and Teck Resources, investing $394 million. Third place was given to Minera Yanacocha, owned by Newmont (NYSE:NEM), with $332 million invested, and fourth was Southern Peru, with $238 million invested. Those four mining companies comprised 42.7% of all mining investment in Peru for 2022.

The report is important to the country, which has long been dependent on the mining sector, as it demonstrates that the sector is still a major driver of Peru’s economy and that investors are confident in the industry’s future. The investments also represent a major source of revenue for the government, with the majority of investments going toward infrastructure and operations.

Exploration activities were also a highlight in 2022, where $383 million in investments flowed from January to November 2022, up 33.9% from the previous year. For existing projects and accumulated mine development investments, the total reaches $778 million, up 49.5% from the same period the previous year.

Peru’s copper production is second only to Chile, which is the world’s largest producer of the metal. The country is also a major producer of silver, zinc, lead, and gold. The mining sector has been a major contributor to the Peruvian economy for many years, and the recent investments show that this trend will likely continue for years to come. The further boost to the industry from the ongoing green energy transition accelerated by factors including the pandemic, rising demand for metals and minerals, and technological advancements should further support the sector’s growth in the years to come.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The Government of Yukon and the Government of Canada have approved in partnership with Yukon First Nations, the Coffee Gold project. The Yukon government completed a consultation with the Selkirk First Nation, Tr’ondëkHwëch’in Government, White River First Nation and Na-ChoNyäk Dun First Nation to make the decision. The Yukon government looks forward to further engagement and consultation with First Nation governments in considering regulations related to the project.

Yukon Premier Sandy Silver said “”The Coffee Gold project will provide significant employment opportunities for many Yukoners and contribute to the territory’s growing economy. Through our ongoing engagement with Yukon First Nations and our collaboration with the Government of Canada, we look forward to supporting the next stages in the development of the Coffee Gold project.”

The Coffee Gold project is an open-pit, heap leach development project consisting of four gold mines in west-central Yukon proposed by Newmont Corporation. The Latte, Double Double, Supremo and Kona mines are located 130 km south of Dawson City; plus a permanent waste rock storage facility.

In a stock transaction in 2016, Goldcorp acquired Kaminak Gold and its Coffee Gold project for approximately C$520 million when it was in the exploration stage. Goldcorp was subsequently acquired by Newmont (NYSE:NEM).

The project, with an operating life of ten years, will be constructed over a 30-month period, providing approximately 700 jobs during peak construction.

Canada’s mining industry is pressing ahead with a run of new projects and reopenings for existing mines. As the country lifts restrictions and returns to full operations for most companies, the mining industry is looking to return to normal drilling operations and output for producers.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The COVID-19 pandemic has affected different industries worldwide. One of the industries affected from an operational standpoint during that period is the mining industry.

Newmont (NYSE:NEM), the world’s leading gold producer, is facing a number of operational problems in addition to accelerating cost increases.

The Denver-based producer said in a recent report that it was forced to cut its annual bullion production target by 500,000 ounces while raising its cost projection.

The company raised its all-in sustaining cost forecast (AISC) to $1,050 per ounce, $80 higher than its previous forecast, citing lower production and higher royalties and taxes.

Newmont’s average gold prices were $1,778 representing a decrease of $135 per ounce from a year earlier.

After third quarter production fell to 1.45 million ounces versus the average estimate of 1.6 million ounces, Newmont announced a reduction in its full-year guidance. This reduction was from 6.5 million ounces to 6 million ounces due to difficulties at its Boddington, Western Australia and Nevada mines.

Newmont announced adjusted earnings of 60 cents per share for the quarter, down from 86 cents last year. That represents a 30% drop to $483 million as bullion prices and sales were down.

Next year production is expected to increase by about 5% and costs are likely to be in line with 2021 levels mentioned in a call with analysts, Tom Palmer, chief executive officer.

Who Is This Affecting?

Overall, the mining industry is facing a number of operational constraints due to the increased costs caused by the pandemic. Tight labor markets, movement and transportation constraints, and supply chain issues have affected the shipment of everything needed for exploration, development, and production.

All of these challenges have affected bullion producers more than base metal miners as gold prices have declined over the past year.

Society, governments and industries are working together to address all the challenges caused by the COVID-19 crisis. The aim is to support infected people, their families and communities to obtain sufficient treatment and vaccines for all.

The impact on the mining sector remains uncertain. However, this crisis has also brought lessons regarding how the pandemic affects commodity demand, supply chains and operating models.

A Resilient Industry

The mining industry has suffered six different crises over the past 40 years. The first was the second oil shock of the 1980s and the most recent was the commodity price shock.

In the analyses of the major crises of the last decades, a comparable pattern could be observed. Each crisis has been divided into four different phases of varying duration and extent. In each phase it can be observed that the crises progressed from a period of price shock, a demand shock, followed by supply and demand equilibrium and finally recovery and the beginning of the new normal.

It is believed by some analysts that the recovery has already begun due to the pickup in operations for the mining industry, and a return of normal production levels for many major miners.

Some Key Commodity Winners

Countercyclical metals such as gold and new industrial applications such as copper will be more resilient to shocks in supply and demand. Iron and metallurgical and thermal coal are likely to be more affected as construction demand falls along with energy requirements as the world transitions to a decarbonized economy.

Additionally, the copper undersupply plaguing the market right now will continue for decades as miners scramble to discover and produce more. New projects are not coming online fast enough to keep up with demand, and the shortage has some countries worrying about sustaining their supply.

Even despite projections based on past crises, there is significant uncertainty around the recovery and effectiveness of health systems to control the spread and impact of the virus.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

While serious concerns linger in the markets about the strength of the swing up, gold mining stocks have continued their leg higher. The first quarter of 2021 was a positive period for gold miners, creating a new extended rally to bring most back to pre-pandemic levels. While most of the biggest miners have been doing well, a drop in the gold stock benchmark and trading vehicle GDX VanEck Vectors Gold Miners ETF of 9.8% in Q1 demonstrates a lack of equality in the gains.

Sentiment Uncertainty Turns to Directional Confidence

Gold itself lost 10% through the period, but has rebounded quickly in Q2. This has been a big boost to miners, particularly in the US. It has been the majors that propped up the GDX in Q1; these stocks often amplify gold’s material moves by two or three times. As spot gold continues to recover, so does sentiment for gold miners, and the majors are seeing this more than others. The GDX reverted 21.8% higher in May, and continued to climb this month. During the same time, gold prices climbed 6.6%, with all indicators pointing to a better sentiment around gold and gold mining stocks.

Q1 2021 reported results show that the majors in particular are outperforming all other gold miners, with strong results and a growing share of the dominant gold-stock ETF. The top 25 GDX gold miners now account for 88.1% of the market cap of the ETF. This dominance is also borne out in the results, with almost all of the top gold mines by production and expansion in the U.S. being owned and operated by those same companies.

The top 25 stocks in the GDX reported recovering and powerful production numbers for Q1. Although total production dropped 2.8% in the period, total revenues jumped 10.5% YoY to $13.7B. This is one of the best quarters ever for this group.

Higher Commodity Prices Boosting Everything

The lower output was offset by 13.4% higher gold prices in the same period, boosting their bottom lines and pushing their financials along healthily. This has been a recurring trend in the mining industry as commodity prices continue to push higher every month with reopenings driving demand along and a positive outlook for the industry expands with every new project and restart announced. Production is nearing pre-pandemic levels again and investment in the first quarter picked up rapidly as miners raced to get back on track for 2021.

The bottom lines of the major gold miners in the ETF was impressive, with 47.1% high YoY earnings. Those soaring earnings and profits seem to be in line with a recovering industry and one that is moving faster than many other parts of the global economy. While some have tried to attribute this to low comparison from 2020, looking at most of these companies shows that this performance comes on the back of normal performance and not any over-compensation from the slowdown of last year.

The List of Winners

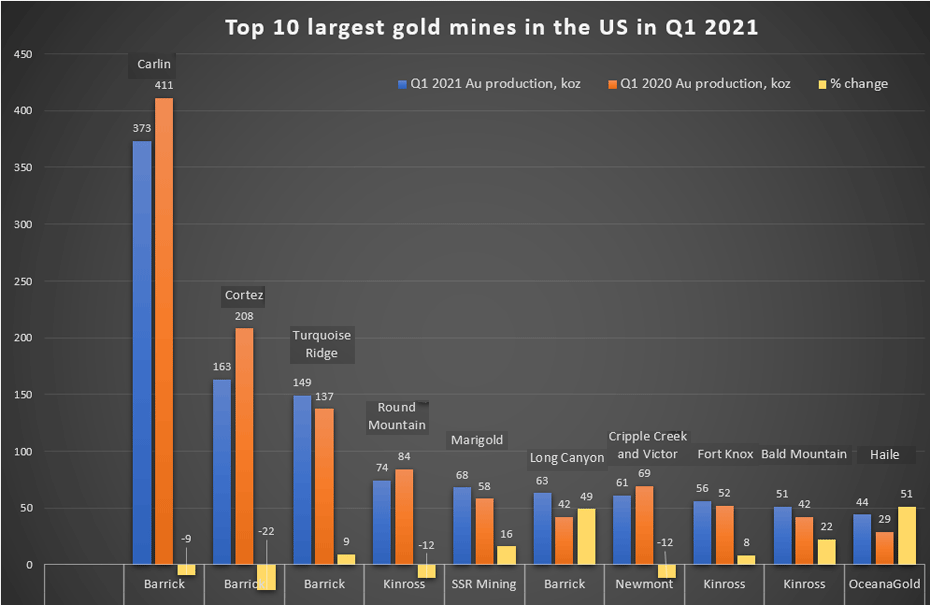

Kitco has put together a list of the top largest gold mines in the US based on gold production in Q1 2021, and it is clear that the biggest players continue to dominate not just the biggest gold stock ETF, but also production quantities.

Barrick takes four of the top ten spots, including the three top spots that seem to generally be reserved for the company across its Carlin, Cortez, and Turquoise Ridge mines. The biggest miners in the industry continue to dominate production and profits right now, but they are also lifting other stocks with them as gold prices rise and industry sentiment begins to reverse in Q2 2021.

| Operation | Major Owner/Operator | Q1 2021 Au production, koz | Q1 2020 Au production, koz | % Change | |

| 1 | Carlin | Barrick | 373 | 411 | -9 |

| 2 | Cortez | Barrick | 163 | 208 | -22 |

| 3 | Turquoise Ridge | Barick | 149 | 137 | 9 |

| 4 | Round Mountain | Kinross | 74 | 84 | -12 |

| 5 | Marigold | SSR Mining | 68 | 58 | 16 |

| 6 | Long Canyon | Barrick | 63 | 42 | 49 |

| 7 | Cripple Creek and Victor | Newmont | 61 | 69 | -12 |

| 8 | Fort Knox | Kinross | 56 | 52 | 8 |

| 9 | Bald Mountain | Kinross | 51 | 42 | 22 |

| 10 | Haile | OceanaGold | 44 | 29 | 51 |

Source: Kitco

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Companies engaged in exploration, mining, and trading often have good returns and revenues. The past year has seen the VanEck Vectors Gold Miners ETF (GDX) underperform the broad market in the last 12 months, but the 11.8% return was more than solid. It is only against the backdrop of a 46.2% gain for the iShares Russell 1000 ETF or the S&P 500 that comparisons lose steam.

Mining for Gold Value

Gold mining companies within gold indexes, however, have been generating asymmetric returns. Many of the winners have continued to scoop up the gains of a rising gold price and a favorable market. Today we’ll take a look at those stocks which may be undervalued according to it’s P/E for June 2021.

Stock picking is often thought of as the reserve of people who have a special talent or gift, however, value investing is as simple as figuring out whether a business’s stock is cheap compared to its intrinsic value as measured by its price-to-earnings ratio. Taking a look at the 12-month trailing P/E ratio, the best value gold stocks are Centerra Gold Inc. (TSX:CG) (NYSE:CGAU), Jaguar Mining Inc. (JAG.TO), Torex Gold Resources Inc. (TSX:TXG), Karora Resources Inc. (TSX:KRR)), and Kinross Gold Corp. (TSX:K)).

Centerra Gold (TSX:CG) (NYSE:CGAU)

The Canadian gold mining and exploration company operates three mines at the moment producing 824,059 ounces of gold and 82.8 million pounds of copper in 2020 alone. The company ran into a speed bump at its Kumtor Mine in the Kyrgyz Republic when the Kyrgyz Government took control of the mine in mid-May. The company lost control of the mine and suspended previously issued guidance for 2021 due to the uncertainty of the situation. However, with a 12-month trailing P/E ratio of 4.1, the company could be a value play for some portfolios.

Jaguar Mining Inc. (TSX:JAG) (OTC:JAGGF)

Our second Canuck on the list explores and develops gold properties in the Iron Quadrangle in Brazil, a profitable greenstone belt in Minas Gerais, Brazil. With a 12-month trailing P/E of 5.4, Jaguar (TSX:JAG) (OTC:JAGGF) is a technical value play for a company operating in an area of mineral exploration dating back to the 16th century.

Torex Gold Resources (TSX:TXG) (OTC:TORXF)

Torex’s 100% owned Morelos Gold Property comprising 29,000 hectares in the Guerrero Gold Belt in Mexico is the flagship project for the company, in a portfolio that includes two other major mines in Mexico. The company’s P/E of 6.7 may be an indicator of an undervalued company waiting for the right attention from investors.

Karora Resources Inc. (TSX:KRR) (OTC:KRRGF)

Both of the company’s primary gold-producing operations are located in Australia along the Norseman-Wiluna Greenstone Belt. Net earnings for Q1 2021 came in at more than ten times YoY as revenue grew 9.2%. The company’s P/E of 6.7 could be an indication of a value play waiting to be unlocked with the kind of financial results from the first quarter of this year.

Kinross Gold Corp. (TSX:K) (NYSE:KGC)

With a diverse portfolio spanning Brazil, Chile, Ghana, Mauritania, and Russia, and forward guidance of 2.4 million gold equivalent ounces for 2021, Kinross (TSX:K) (NYSE:KGC). Net earnings rose 21% as revenues grew 12.1%, possibly making the company’s P/E of 6.8 a value indicator for 2021.

Hunting for Deals

Undervalued companies can be opportunities to pick up shares at bargain prices before the rest of the market figures it out. Stocks like Centerra Gold (TSX:CG) (NYSE:CGAU), Jaguar Mining Inc. (TSX:JAG) (OTC:JAGGF), Torex Gold Resource (TSX:TXG) (OTC:TORXF), Karora Resources Inc. (TSX:KRR) (OTC:KRRGF), and Kinross Gold Corp. (TSX:K) (NYSE:KGC) could be the value buys for 2021 for investors looking to add some gold stocks to their portfolios.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

As mining companies continue to shift away from dirtier, less efficient practices, electrification is one of the first things on their to-do list. For many, reducing carbon emissions on-site and throughout operations outside of mining is critical to attracting capital and remaining competitive. The rising costs of fuel and complex maintenance for combustion engines have given companies an incentive for change, and miners are stocking up on battery-powered trucks for hauling, transportation, and other tools that previously used diesel or gasoline to get the job done.

A Scandinavian Approach

Swedish equipment manufacturer Sandvik now expects that the market for battery-electric underground mining equipment will grow at a faster clip in two to three years. The dual goals of lowering emissions and cutting costs give these companies plenty of incentives to make the switch, with investors also looking on eagerly to see what companies are doing with respect to the all-important environmental, social, and governmental principles.

Sandvik’s mining business head said that the company could sell more electric than diesel-driven underground mining equipment in the coming ten years. Epiroc and Caterpillar, two of Sandvik’s main competitors and some of the largest suppliers in the world for the mining industry, will also be going head to head with the company to supply the tools necessary for the electrification coming down the line, beginning now.

Sandvik claims that its approximately 30 battery-electric loaders and trucks operating in underground mine production is the largest amount in current operation, more than any of its competitors. Still, this amount is less than 0.5% of its total fleet and shows how much runway there still is for this market segment to expand for equipment suppliers. As it continues to gain pace, it will drive much of the new equipment sales over the coming decade. Henrik Ager, head of Sandvik Mining and Rock Solutions, said, “In the past two years, we have gone from thinking that electrification might turn into a great technology shift to becoming certain that’s where we’re heading.”

He said that in two to three years, electric machinery should be fully proven to work in mines and be part of the discussions for all procurement. Approximately 60% of an underground mine’s energy consumption comes from infrastructure, mainly electrified. Still, the rest is consumed by loaders and trucks, transporting and hauling heavy materials from the site to refinement centers and processing plants or to stockpiles. Those loaders and trucks still primarily run on diesel, carrying up to 65 tonnes of rock at a time.

Good for the Environment, Good for Investment

For investment bank UBS, the electrification of the industry is not only an environmental benefit for all stakeholders but will bring savings for mining companies as well. Analyst Guillermo Peigneux Lojo said, “In the years to come we shall see an accelerated replacement cycle for especially underground mining equipment, although surface equipment will also benefit from solid growth rates.”

Barriers still remain until full adoption of electric vehicles and fully electric mines are the new normal. Battery-driven loaders and trucks are more expensive to buy, making the upfront costs unpalatable for some mining companies at the moment. However, down the road, the benefits are numerous. Savings on ventilation and cooling, high costs in underground mines can make it beneficial and profitable for mines to go completely electric right now.

Major mining companies have already begun the process of electrification at many of their mines. Newmont’s (NYSE:NEM) Borden gold mine and New Gold’s (TSX:NGD) Afton mine currently use Sandvik’s battery-electric equipment in their operations. The loaders and trucks, as well as some of the lighter equipment, use lithium-ion batteries, a technology that allows for faster charging and higher battery density, leading to more prolonged use between charges, an essential factor for rapid adoptions.

Mirroring The Ethos of Tesla and Elon Musk

Elon Musk’s Tesla has created a similar business model, focusing on bringing battery technology to the forefront of the mission, and bringing down the cost and effectiveness of the batteries in its vehicles. Sandvik’s vision is to do the same; the company is building around the battery instead of starting with the vehicle itself. The research and development costs are much lower, and the equipment being used is already efficient and effective.

“It’s the Tesla parallel. That is what they have done, and it’s much better,” Ager added.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Yesterday saw US gold futures hold at $1908.20 per ounce on the Comex, a gain of almost 7.7%. July 2020 saw the biggest gains for bullion, in the middle of a pandemic that saw safe-haven assets like gold and USD climb steadily. Now, growing inflationary pressures may be providing some measure of fuel to gold’s fire, but bullion’s appeal is still multivariable.

As investors wait for key US jobs data this week, they should find a little more clarity on the progress and strength of the economic recovery. A disappointing report for April showing 266,000 jobs created versus just over 1,000,000 expected was a not-insignificant pump on the brakes for optimists. Gold saw it’s allure increase overnight and regain some of the momentum it had in 2020. A falling US dollar, currently in its ninth consecutive week of a months-long downswing, has added to some of gold’s positive shine.

Good Times for Gold Miners

Of course, gold miners are keeping up with production, as the value of their product continues to rise. The first quarter of 2021 saw a small drop YoY in Q1 production for most miners, as the pandemic only started hitting hard shortly after. The results make it clear that the first quarter of 2021 looks quite similar to the first quarter of last year, giving production the appearance of being “back to normal”.

Top 3 Gold Producers Q1 2020

1. Newmont Mining Corp. (NYSE:NEM)

Newmont (NYSE:NEM) took the top spot with production coming in close YoY at 1.45 Moz, a 2% decrease from the prior year’s quarter. The sale of its Red Lake property, lower leach pad production and the ramp down of the Yanacocha mill, lower mill throughput at Nevada Gold mines, and more contributed to the slight hit in production. Still, most sites are returning operations to full capacity while managing ongoing pandemic-related impacts lingering from the past year.

2. Barrick Gold Corp. (NYSE:GOLD)

Second place goes to Barrick Gold (NYSE:GOLD). The Canadian producer put out 1.1 Moz in Q1 2021, a bigger decline than Newmont’s (NYSE:NEM) YoY at 12% (1.25 Moz Q1 2020). With reopenings continuing, the second half of the year is likely to be stronger than the first, as the company has plans for mine sequencing at Nevada Gold Mines, a ramp-up of underground mining at Bulyanhulu and higher anticipated grades at Lumwana in Zambia.

3. Polyus (OTC:OPYGY)

Bronze goes to Russia gold mining company Polyus (OTC:OPYGY). Total output hit 592 thousand ounces in Q1 2021, almost unchanged YoY from 595 thousand ounces in 2020. As the company has just completed its mill capacity expansion project, the rest of 2021 is also likely to be brighter than the beginning for this gold miner.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

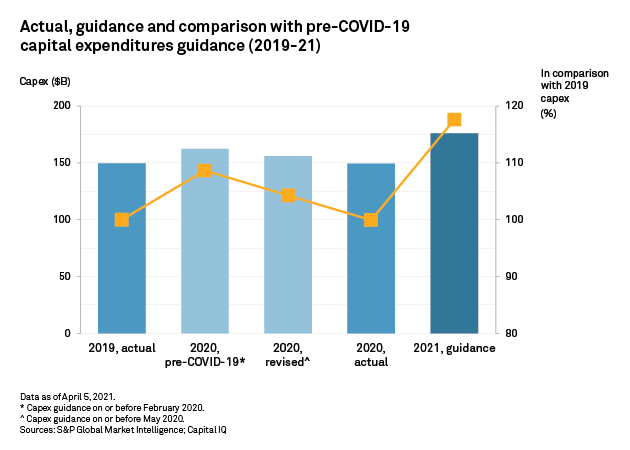

S&P Global Market Intelligence’s new report highlights the significant impact the pandemic has had on capital expenditure in 2020. The year was a complicated one, with projects shutting down temporarily, and licenses for new mines suspended until the lockdowns began to ease around the world.

Despite it all, the mining industry has fared well and continues to forge ahead with minimal disruption. However, the report found that among more than 400 mining companies examined, capital expenditures dropped 8% in 2020 when lockdown forced projects to stop work, and global supply chains began to crack under the dual pressures of shifting demands and lower production.

Feeling Better

The first quarter of 2020 held some optimism for the year. The miners’ group forecasted a capex YoY increase of 9% to $162 billion. By the beginning of the second quarter, expectations had been revised and the spending plans reduced 4% lower to reflect the coming changes. Still, this would represent an increase for the year before, as no one had anticipated the length of the lockdowns or the severity of the pandemic.

In the end, total capex for 2020 came in at $149.5 billion well below forecasts, but arguably strong considering the harsh mining environment of the year and the fact that global economic confidence was sucked out of the air faster than an airlock for a spaceflight.

A Realistic and Optimistic Outlook for 2021

S&P has set a positive tone for 2021, with a forecast of global gross domestic product growth of 5.5% in 2021, boosting capex and numbers across every. The company is forecasting a mining industry capex of $176 billion, up a substantial 18% fom 2020 and 2019.

As projects were put on hold last year and confidence dropped off a cliff, mining companies needed to revise their expectations. Now that the situation is improving rapidly, companies are ramping-up their activity. Positive outlooks are not hard to come by for miners as strong prices for metals and minerals continue to push commodity prices higher, boosting profits.

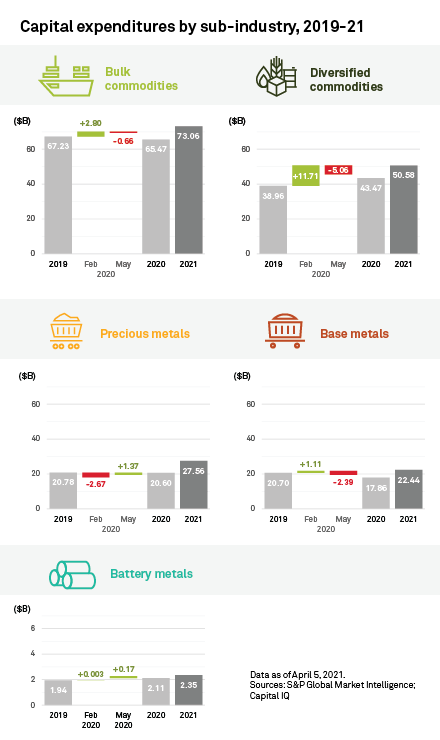

The Rich Get Richer

The Eastern Hemisphere is leading the recovery right now, particularly China and Australia. The influx of capital expenditures won’t be balanced across metals companies or metals either. Precious metals companies are expected to spend the most, and increase their capex by over a third compared to 2019. The biggest spenders will likely be the usual suspects including Newmont (NYSE: NEM) (TSX:NGT) and Gold Fields (JSE:GFI) (NYSE:GFI).

Large cap mining companies are always the first to jump into new projects with high capitalization levels and strong cash balances on hand. Most of these companies will recover stronger and faster, and S&P expects that companies with a $50 billion+ market cap will surpass their smaller peers for both forward guidance and spending. This would exacerbate the trend of the winners taking all, and the biggest players consolidating their gains and building on them. The largest market cap group is expected to spend 51% in 2021 compared to 2019, and the next three groups of companies expected to keep similar levels to 2019, averaging 12%, although they would be increasing their spending from 2020.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Monday, May 17 saw Newmont (NYSE:NEM) (TSX:NGT) complete its acquisition of GT Gold by scooping up the outstanding 85.1% of common shares of the Canadian exploration company in a C$393 million cash deal. Announced two months ago in March, the deal allows Newmont (NYSE:NEM) (TSX:NGT) to take control of the Tatogga gold-copper project in the Traditional Territory of the Tahltan Nation.

Tatogga sits about 14km west of Imperial Metal’s Red Chris copper-gold mine in British Columbia. For Newmont (NYSE:NEM) (TSX:NGT), the acquisition gives the US-based gold mining company a major advantage in the region, and further consolidates its position as the world’s number one gold producer.

Bigger and Better

By adding the copper-gold project to Newmont’s (NYSE:NEM) (TSX:NGT) portfolio, the company will add significant gold and copper annual production to its overall output. It also expands the company’s foothold in the area by adding to its existing interest through the company’s 50% ownership in the Galore Creek project; the acquisition includes the Saddle North asset. The company has also opened up opportunities for further exploration beyond the deposits at Saddle North with this acquisition.

Newmont (NYSE:NEM) (TSX:NGT) president and CEO Tom Palmer commented in a statement: “With the acquisition of GT Gold and the Tatogga project in the highly sought-after Golden Triangle district of British Columbia, Canada, Newmont continues to strengthen our world-class portfolio. We will partner with the Tahltan Nation at all levels, and with the Government of B.C to ensure a shared path forward as the company understands and acknowledges that Tahltan consent is necessary for advancing the Tatogga project.”

M&A Optimism Picks Up

M&A activity has picked up again after a sluggish rut in 2020 for the entire mining industry, but beautiful British Columbia’s volume has been higher than the average. Many of the deals in the last six months have involved deals with Vancouver-headquartered companies or companies with projects in the province.

In 2020, there was the sale of the New Gold (NYSE:NGD) (TSX:NGD) Blackwater property south of Prince George to Artemis Gold (TSX.V:ARTG) for a total of $190 million. The snowfield project operated by Pretium Resources (TSX:PVG) was bought by Seabridge Gold Inc. (TSX:SEA) in December 2020 for $100 million in cash, a 1.5% net smelter royalty on all production, and a future contingent payment of $20 million. Those deals began to foreshadow a pickup in M&A activity as miners’ optimism rose with the lifting of restrictions and business operations in some parts of the economy.

In early 2021, Eldorado Gold (NYSE:EGO) (TSX:ELD) made a neat and tidy acquisition of QMX Gold Corp. (TSX.V:QMX) for $132 million to kick off the new year.

More activity is likely with higher volume as well as bigger buyouts as a dearth of exploration projects or development projects makes anything operating or of a higher-quality worth even more. With everything scrambling to scoop up the same properties and projects, the competition is fierce, and it is driving bidding wars and competition not unlike the red-hot Canadian housing market.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Ethiopia’s mines ministry, in an effort to encourage production, has issued warnings to companies operating idle mines. Many mines sit unused or without active operations for years. The ministry was quoted: “Following a re-investigation, 27 mining companies that had been licensed to operate in the mining sector but failed to enter operation have had their licenses revoked, and three miners have been immediately warned to correct their mistakes.” Takele Uma, Ethiopian mines minister, was reported by Reuters as saying that the licenses will now be opened up to international tender.

The country has revoked 90 mining licenses, with 63 of those being revoked in December 2020. The mining companies involved failed to renew their licenses, or had not made royalty payments. Ethiopia would like to expand and develop its mineral and metal resources and needs committed partners to reach its goals. Mining will be a key sector for the country moving forward as it aims for economic growth and reform across every sector.

Trying to Revive an Economy on Life-Support

A large trade deficit and lack of regular foreign exchange have left the country in an untenable position with stagnant growth for most parts of the country and recession for others. Ethiopia relies on many artisanal miners, but would like to lure more international miners into the region. Larger companies will be allowed to bid on the licenses available for international tender to build a more robust and consistent mining industry.

The nation so far has exported gold valued at over $504.73 million in the last ten months. The metal accounts for the vast majority of the country’s mining exports, with over 90% being attributed to the yellow metal. Unfortunately, official figures and royalty payments have been on the decline for the past eight years as illegal trade and the closure of big plants have plagued the industry.

There is Hope for the Patient

December 2020 saw the government take its economic future in a new and more determined direction with a 10-year plan directed at bringing more foreign exchange through imports and exports. The goal is to grow the current import and export substitution of minerals from $265 million to $17 billion by 2030. The ambitious plan has its roadblocks, but the cancelling of the licenses is a solid first step in the right direction.

Investors may also be enticed by a 25% corporate tax rate and a 10-year loss carry-forward, royalties of 4% on industrial minerals, 5% on metallic minerals, and 7% for the all-important gold production. Mining companies obtaining licenses will also be pleased with their exemptions from customs duties and taxes for machinery, equipment, and vehicles that can be considered essential to operations.

Some big companies already have a foothold in the country and will benefit from this accommodating 10-year roadmap. Kefi Gold and Copper, as well as US-based Newmont (NYSE:NEM) (TSX:NGT) have assets in Ethiopia, with ongoing operations.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |