Peru is one of the prime copper mining destinations for miners from every corner of the globe. Some of the largest deposits of the red metal are sitting in the ground in this mining-friendly country. For Anglo American, the Quellaveco Mine presents an opportunity to add another world-class cost-efficient mining operation to their diversified portfolio.

A Hotbed

Anglo American is part of a group of miners that contributed 58% of mining investment in Peru in January. While mining investment in Peru slumped because of the pandemic and remains below pre-pandemic levels, investment in infrastructure and planning has restarted in earnest now. The Quellaveco Mine is a significant focus of capital expenditure for the company, and it’s pretty easy to see why.

A Hot Commodity

According to Bloomberg, “Within a decade, the world may face a massive shortfall of what’s arguably the most critical metal for global economies: copper.

The copper industry needs to spend upwards of $100 billion to close what could be an annual supply deficit of 4.7 million metric tons by 2030 as the clean power and transport sectors take off, according to estimates from CRU Group. The potential shortfall could reach 10 million tons if no mines get built, according to commodities trader Trafigura Group. Closing such a gap would require building the equivalent of eight projects the size of BHP Group’s giant Escondida in Chile, the world’s largest copper mine.”

Copper miners are scrambling to keep up with demand, and for the time being, prices continue to climb due to the supply shortfall. In the coming years, companies will need to manage their projects to avoid overproduction and a glut of the valuable metal, but for now, there are plenty of opportunities to ramp up production and get more copper into the market.

This is great news for companies that are developing and investing in new projects right now,

Quellaveco Mine

The mine is one of the largest copper deposits in the world and is located in Peru’s most established copper-producing region. Due to the skilled workers and established infrastructure, the project is likely to be a big winner for the company when it begins.

Anglo American expects the mine to be ready for 2022, at which time the first copper production will begin. This project seems to be coming at just the right time to take advantage of a confluence of events and circumstances in the global economy and the process of electrification worldwide. For now, investors will be watching for any sign of the Quellaveco Mine proceeding according to plan, and Anglo American will need to deliver on many of their promises to deliver this project on time and on budget.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Lupaka Gold’s (TSX-V: LPK) Invicta Gold Project is on the brink of production, set to become Peru’s next producing gold mine.

However, everything is not going to plan…for the better.

What has been quietly observed is that (1) the grades are coming in higher than the PEA and (2) the company is already making plans to increase production above the PEA throughout rate of 350 tpd. All this means higher levels of production and cash flow once the actual mining commences later this year.

Recent underground sampling of mineralization is revealing an asset that offers more than originally outlined in the company’s April 2018 Preliminary Economic Assessment (“PEA”) which gives investors additional upside for any increases in mine output, improvement of grade and additional ounces to the overall resource.

The April 2018 PEA for the Invicta Mine outlined a mineral resource of 3 million tonnes of Indicated Mineral Resources at 5.78 grams per tonne (“g/t”) gold equivalent (“AuEq”) ounces using a 3.5-g/t cut-off grade (“COG”), and 600,000 tonnes of Inferred Mineral Resources at 5.49 g/t AuEq.

Within that resource the Company has a PEA that outlines an initial 6-year mine life that will produce produce a total of 669,813 tonnes of mineralized material processing 350 tonnes per day (“tpd”) at an average grade of 8.6 g/t Au-Eq. Lupaka’s grades included estimated metallurgical recoveries, and the true grade will likely be even higher than 8.5 g/t AuEq.

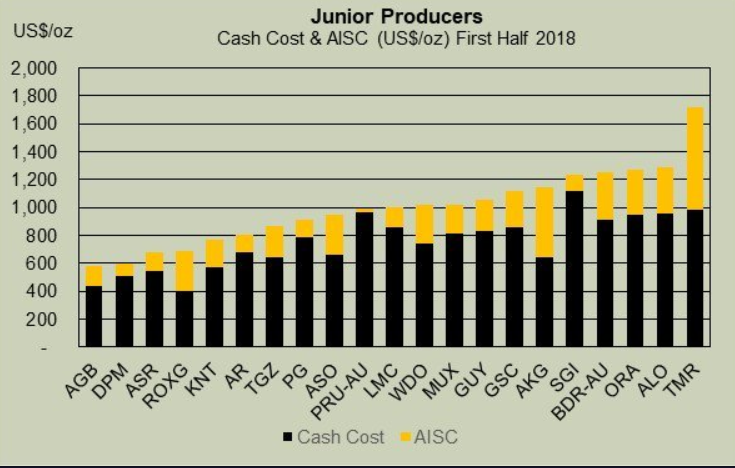

Just to highlight, with an all in sustaining cost (“ASIC”) of $575 per gold ounce equivalent, Lupaka Gold will be one of the lowest cost junior producers.

Source: AuCu Consulting, Ron Stewart (@RonStew12139302)

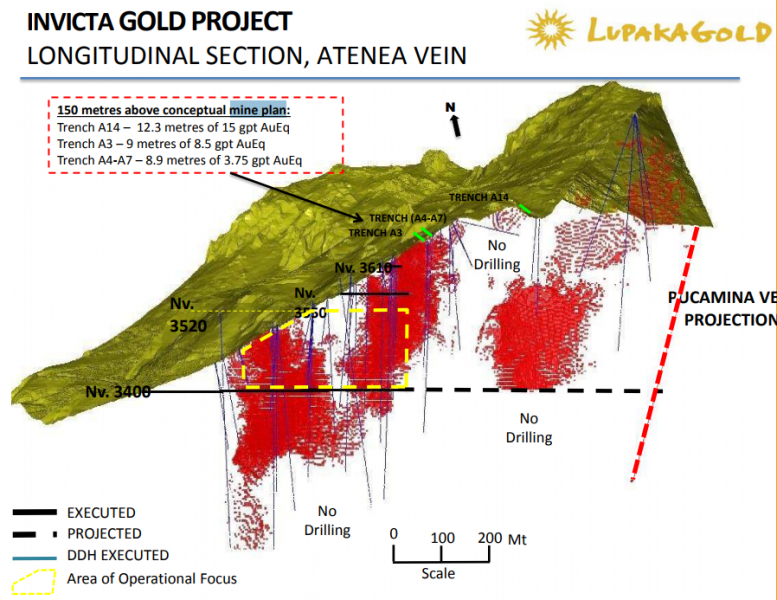

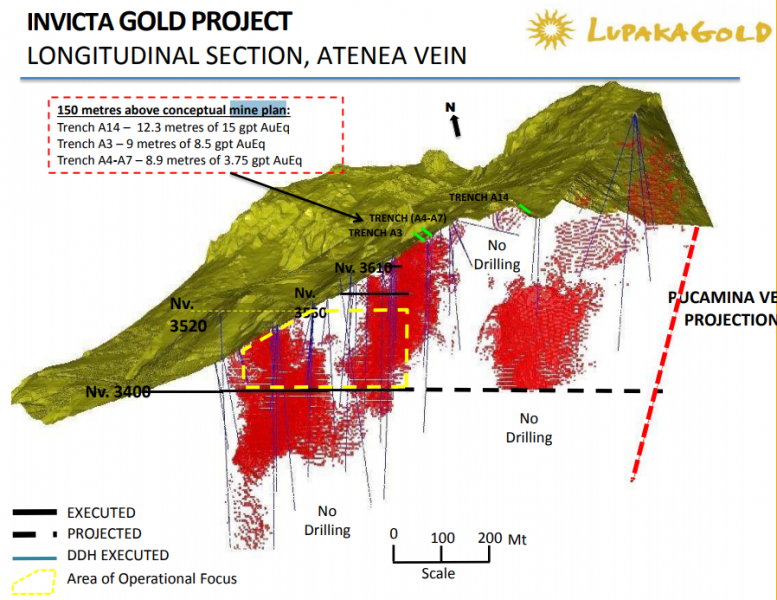

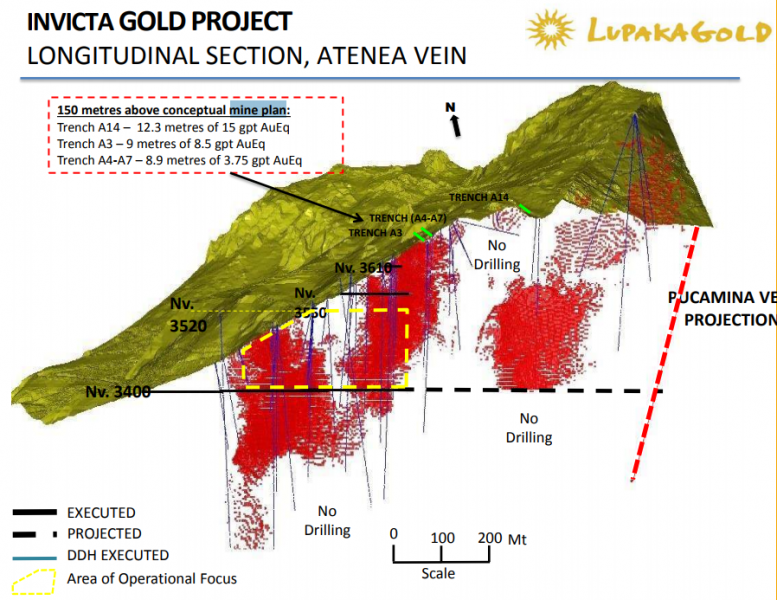

As part of the development work to put Invicta into production, Lupaka has been conducting channel sampling every 5 metres on all workings during development.

The results have demonstrated continuity of the high grade mineralization and additional potential that the Aetnea vein hosts.

In March 2018, the company released preliminary sample results:

- Sample assay values over the footwall vein averaged 9.86 g/t AuEq over 130 metres, with an average width of 6.1 metres (“m”);

- Sample assay values over the hanging wall split averaged 7.00 g/t AuEq over 70 m, with an average width of 6 m.

In June, Lupaka released further results from a underground sampling program on the newly developed 3430 production sublevel.

- 9.22 g/t AuEq over a strike length of 130 m, with an average sample width of 4.2 m.

The company provided additional results in July:

- Channel sample assay values from across the strike of the Atenea vein, within the raise development, returned an average of 23.45 g/t AuEq over a vertical height of approximately 30 m;

- Sampling returned significant grades such as sample number 2606E which returned 227.77 g/t AuEq over a width of 1.2 m.

In addition to the sampling, development and rehabilitation of the Invicta mine has provided ~6,500 tonnes of mineralized material from the 3400 Level and when sampled on surface returned an average grade of 7.21 g/t AuEq.

Grade consistency is always a problem with mining. However, it is appearing that the Invicta PEA outlined a muted gold grade on a smaller area of the known mineralization which does not highlight the potential for higher grade zones and the prospectivity of the area.

Higher grades could improve the bottom line as mining proceeds through the Aetnea vein and into the other zones around the current area of operational focus.

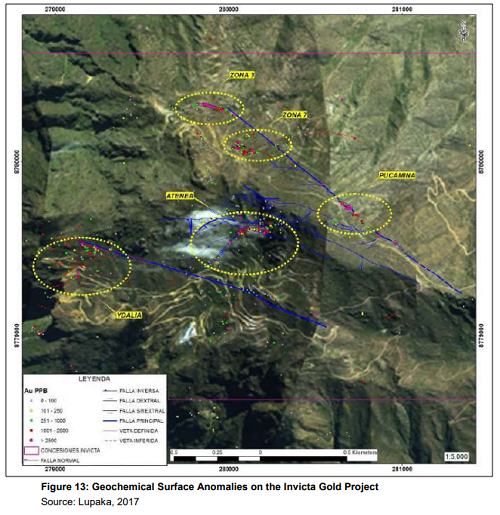

Past exploration at the Invicta mine property indicates that the property has considerable potential for mineral resource expansion through exploration.

Structural studies, geophysical and geochemical work conducted to date strongly suggest the potential for mineral resource expansion along existing mineralized structures.

Past sampling around Invicta revealed the exploration potential with many areas reporting grades greater than 6 g/t AuEq. mine

All in all, the focus on a smaller area for the PEA and initial mine plan reveals that the company’s plan has been to bring production online with a well defined resource with the Aetnea vein through underground mining with minimal capital expenditures, rather than trying to finance and build a large scale operation off the back.

With the commencement of limited toll mining in September, and the beginning of full scale production hopefully in October, Lupaka will have the necessary cash flow to conduct exploration and prove up more ounces in the ground and significantly alter the assumptions of the April 2018 PEA to extend the life of mine.

The next milestone is the final mining exploitation licence, which requires an inspection by the Peruvian Ministry of Mines and Energy.

The inspection will be performed before the end of October and upon receipt of the exploitation licence, the company will have the go ahead to produce at a rate of 400 tonnes per day, or 12,000 tonnes per month.

However, with the permit to operate at 400 tpd, the company could see its potential production increase by 14% from the 350 tpd production assumption outlined in the PEA, boosting the project’s cash flow.

Currently, shares in Lupaka gold are trading near year-lows which discounts a years’ worth of work and development that has improved access to the mine, defined a PEA, divestment of non primary assets, cash flow from initial toll mining and on the cusp of full scale mining.

The company laid out a plan to bring into production the Invicta mine with a small area of operational focus and a humble gold grade in comparison to recent sampling.

The plan is working and it is starting to reveal that there is more to the story than initially outlined…a good thing for investors.

*The author of this article was compensated for the creation of this article in cash. The author picked up shares in the public market, ranging from prices of 14 cents to 20 cents over the past year. This article is meant to serve informational and marketing purposes only and not a technical report and does not constitute a buy recommendation. As always, please do your own diligence.

*The Mineral Resource Statement for the Invicta Project is tabulated to a cut-off grade of 3.0 g/t Au-Eq. Cut-off grades are based on a price of US$1,250 per ounce of gold, US$17.00 per ounce of silver, US$3.00 per pound of copper, US$1.05 per pound of lead and US$1.20 per pound of zinc. The equivalent gold calculation assumes mill recoveries of 85 percent for gold, 80 percent for silver, 82 percent for copper and lead and 77 percent for zinc

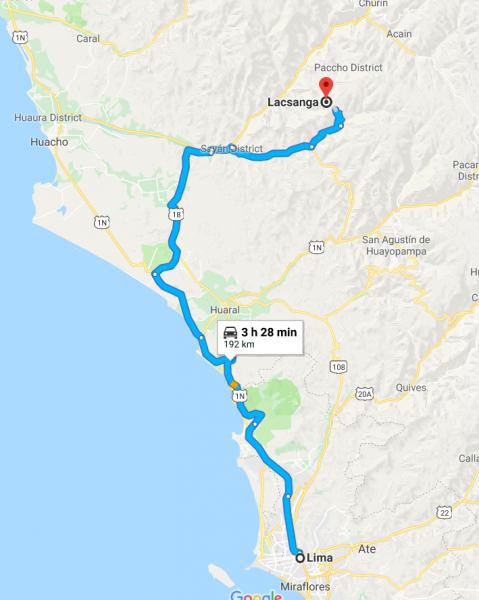

Lupaka Gold Inc. (TSX-V: LPK) has been completing the necessary steps to achieve commercial production at its wholly-owned Invicta Gold project in Peru, located 120 km north of Lima by road. Recently, I had the opportunity to re-visit the mine site to see how work is progressing towards production.

It is at this point in the life span of a mining company where institutional investors typically invest, and the stock price starts to move back up towards full value, which makes it a good time to invest. Lupaka Gold (TSX-V: LPK) is at this point.

With financing secured, the company has commenced construction and development work in order to commence production in the second half of 2018, resulting in potential full appreciation for its shares. The Company’s diligence and hard work is starting to bare fruit through the following recent developments:

- Fully funded to complete its 6 to 12-month goals, including the start of production at Invicta

- Produced a positive PEA on the project with an initial 6 year mine plan

- Community agreement in place

- Commencement of roadwork to mine site

- Building out the in-country team with the appointment of Dan Kivari, P.Eng., as Director of Operations

- Mine rehabilitation and construction

- Ongoing sampling and surveying

The financing secured in 2016 was through Pandion Finance for a total of $7 million (U.S.), available to the Company in three tranches, all of which have now been drawn. This forward gold sale agreement is repayable to Pandion by delivering a total of 22,680 ounces of gold over 45 months.

Pandion plays a partnership role in development by receiving payment in gold from the actual mine rather than by way of equity or traditional debt structures. It also does not dilute shareholders as would with a financing in the market.

With money in place, now begins the real work.

On March 1, 2018, Lupaka issued a preliminary economic assessment (PEA) which outlined low capital expenditures, an initial mining scenario of 350 tonnes per day (tpd), and a very quick payback and path to cash flow. The strategy is to commence mining in an area close to existing infrastructure and focus on a small portion of the resources within the Aetnea vein. While the current Environmental Impact Assessment allows for up to 1,000 tpd, Lupaka’s approach is to start small and gradually increase production over the next few years.

The PEA boasts all-in sustaining costs of $575 per gold ounce equivalent (“AuEq oz”) over an initial six-year mine life and an average annual pre-tax operating profit of $12.3-million ($1300 gold assumption), very attractive economics at current metal prices. There is no need to state the Internal Rate of Return (“IRR”) as it produces meaningful cash flows within the first year.

The updated mineral resource (part of the PEA) outlines 3.0 million tonnes (“Mt”) of Indicated Mineral resources at 5.78 grams per tonne (“gpt”) AuEq oz using a 3.5-gram-per-tonne cut-off, and 0.6 Mt of inferred mineral resources at 5.49 gpt AuEq oz. The initial six-year mine plan is designed on only a portion of the mineral resource (~0.6Mt at an average head grade of 8.58 gpt AuEq, incorporates existing infrastructure which minimizes capital start-up costs.

The company now has over 24 years of tonnage, in terms of Indicated Mineral resources, mining at the 350 tpd, however management’s goal would be to increase production towards the EIA level of 1,000 tpd, which would increase production from 33,700 AuEq oz/yr up to closer to 100,000 AuEq oz/yr.

At the main portal, the company recently announced sample assay values over the footwall vein averaged 9.86 gpt AuEq over a strike length of 130 metres, with an average width of 6.1 metres. The average sampled grades are in-line, or higher, than grades within the mine plan, based on the PEA. With a combined average width of over 12 metres, the sub-vertical Invicta deposit extends for over 130 metres in strike length on the 3400 level and will be immediately accessible for extraction when the Invicta mine becomes operational in the second half of 2018.

The start small approach also allows the Company to reinvest into exploration in surrounding areas, in order to gain confidence to increase the mine plan, and to prove up new resources to potentially extend production for years to come.

Lupaka has been granted a water use permit from the Peruvian Ministry of Agriculture. Surface rights have been attained, a well has been constructed, and testing studies have concluded it can supply water up to 60 liters per second during the dry season, which should be sufficient supply for an onsite mill in the future.

As part of the agreement that was completed with the community of Lacsanga in July/2017, Lupaka was to undertake and complete certain improvements to the roads, including widening and creation of bypasses around the communities. The company signed a contract with local operators to expand, enhance and modify 27 kilometres of road commencing from the paved Huacho-Churin-Oyon Highway, located at approximately 1,500 metres above sea level, up to the Invicta project located at approximately 3,500 metres above sea level.

Work is ongoing to ensure that 30-tonne trucks can operate safely and efficiently using North American standards. This involves proper safety berms, passing stations, water drainage, widening hard rock areas using explosives and community by-passes routes.

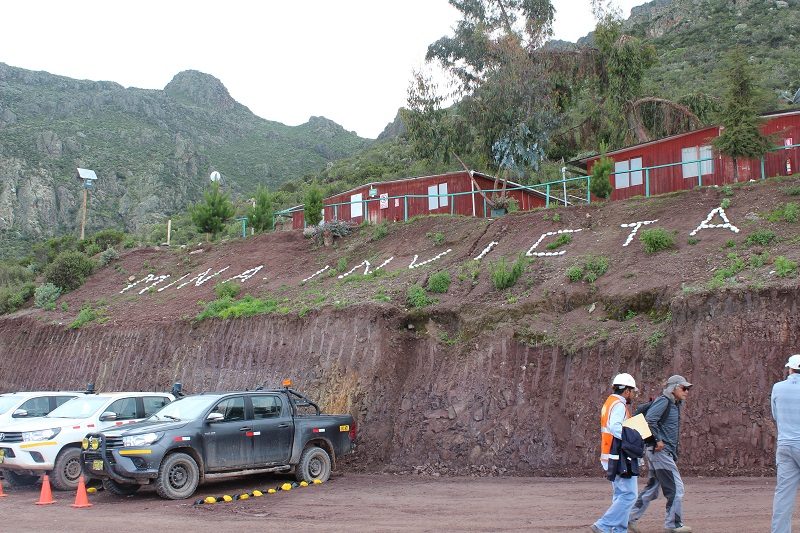

There is a camp to house workers on site that was built by previous operators. It currently can house about 60 to 70 people, but it is already looking like they will have to expand the camp to accommodate a growing team.

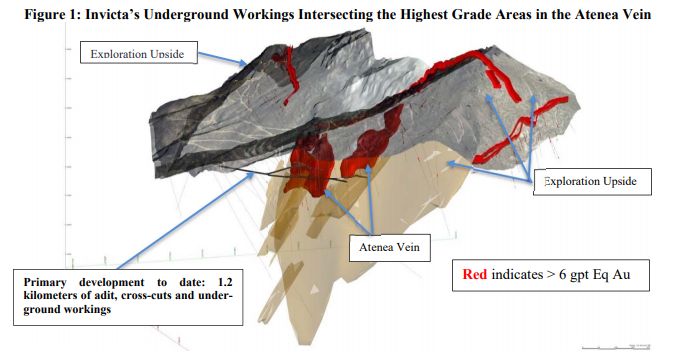

Lupaka announced that development would begin with rehabilitation, preparation at Invicta with three crews, a new adit and 3430 level to be constructed. The Invicta project has approximately of 1.2 kilometres of existing adits, cross-cuts and underground workings.

As you can see below, the cross cut at the 3430 level is in the process of rehabilitation and construction. Over the past few months, work has been advancing to the point the cross cut has approached the main vein wall. Two 4.2-yard PLH Scoops have arrived on site along with a single boom jumbo drill in preparation of accelerated development and stope preparation.

At the lead of operations on site is recently appointed Dan Kivari, P.Eng. (picture in the centre above). He has more than 30 years of international experience in metallurgy, engineering and management of mineral projects throughout various stages of development. Most recently, Mr. Kivari held the position of chief operating officer at Stellar Mining Corp., a privately held mining company in Peru.

Mr. Kivari’s previous work experience includes several senior operating roles such as regional manager for Agnico Eagle Ltd.’s Western and Nunavut operations, where he was responsible for the development of the Meadowbank gold project, and vice-president of operations with Yamana Gold (TSX: YRI) overseeing the development of the Chapada copper-gold project. Throughout this experience, he has picked up the skills necessary to build a team for the Invicta Project.

There is still plenty of work to be done to meet the company’s goal to de-risk and evaluate the suitability of a plant by the second half of 2018. New bulk samples need to be extracted and sent to toll milling facilities to test and optimize metallurgical recoveries and concentrate quality.

A previous run-of-mine bulk test in February 2016 achieved good recoveries in concentrate streams — returning 87.5% gold, 91.2% silver, 91.5% copper, 90.03% lead and 90.1% zinc. The sample was a blend of approximately 80% run-of-mine material and 20% from a low-grade stockpile derived from development.

Looking forward, the company and the geology suggests that there is plenty more to be mined and there is the potential for the construction of a mill which would further reduce the company’s costs and improve any future valuation of the Invicta mine.

From six months ago, the Invicta Gold project is now a completely different scene. Today the roads have and continue to be widened (making them safe), staff and operating equipment is on site and the newly created 3430 Level cross cut has hit the main zone of mineralization.

From an investors perspective, mines moving to production present the greatest investment opportunity because each advancement the company makes de-risks the project and it becomes a question of the operating team to achieve goals on budget and proving the business model works. Lupaka is at this stage and its shares present an opportunity right now.

The hard work is underway at Invicta and the team is already in place to bring it into production, just in time for improving metal prices and the renewed interest in gold. The company appears to be well positioned to bring the project online during the second half of 2018 and meet its objective of becoming cash flow positive in its inaugural year.

Investors can look forward to the following positive catalysts:

- Bulk sample results from prospective toll mill facilities

- Toll milling agreement

- Offtake agreement

- Exploration plans and results

- Obtaining commercial production at 350 tpd

- Engineering and trade-off studies for building a plant onsite

With an all-in-sustaining cost of $575 per AuEq oz over initial six-year mine life, and plenty of resources not yet announced with permits in place to increase production, Lupaka Gold (TSX-V: LPK) is a company to watch.

It is at this stage where investors could see the greatest share price appreciation as the company is on task and working towards becoming a producing gold mine.

Lupaka Gold Inc. (TSX-V: LPK)

With the recent close of the sale of the company’s Crucero property to GoldMining (TSX-V: GOLD), Lupaka Gold Corp. (TSX-V: LPK) has secured the funds to take the next step with its Invicta Gold project. Today, the company announced the commissioning of a Preliminary Economic Assessment “PEA” for the Invicta Gold Project.

With the backing of Pandion Finance and its gold purchase agreement providing the necessary funding, Lupaka is motivated to meet its obligations which makes now an exciting time for the company and its shareholders.

The company has hired SRK to prepare the PEA. This provides a continuity of project knowledge as the project’s 2012 resources estimate was prepared by SRK and the company’s own internal mining studies of Invicta were prepared with assistance from SVS Ingenieros of Lima “SVS”, Peru, a subsidiary of the SRK Consulting Group. The company plans the completion of the PEA technical report in the first quarter of 2018.

The initial six-year mine plan that was developed and prepared by SVS, which outlined ~735,000 tonnes at a grade of ~6.1 g/t AuEq. for 23,000 oz. of gold equivalent a year, according to a rough calculation. The plan was developed from the 3,400-metre level and extends up 120 metres.

Drill results indicated that the mineralization extends at least as far below the 3,400 level as it does above. In addition, there is a well-defined section of measured and indicated directly along strike to the northeast that is within a few hundred metres, and of the same characteristics as the segment in the mine plan.

The first bulk sample in October 2015 produced a copper, lead and zinc concentrate that was sold to an off-taker. The concentrate was exceptionally clean and was absent of any penalty elements, so buyers could pay well for it because they can mix it with less clean concentrate and blend it.

The company completed its second run-of-mine bulk test in February 2016 and achieved good recoveries in concentrate streams — returning 87.5% gold, 91.2% silver, 91.5% copper, 90.03% lead and 90.1% zinc. The sample was a blend of approximately 80 % run-of-mine material and 20 % from a low grade stockpile derived from development.

The bulk sample was processed with the prime objective of producing a saleable concentrate and no effort was made to optimize content of specific metals, according to the company. The resulting concentrate was clean, with few penalty elements which is ideal for sale and blending with other concentrates.

Once in production, the hope is that cash flow from Invicta will be used to grow the operation. There are numerous zones outside of the Atenea vein that contain mineralization, and the targeted Atenea resource could increase, as development offers access to high-grade intercepts and underground drill sites. In addition, based on gold and copper within the under-explored quartz-sulphide vein zones, the company believes the Invicta resource could expand.

At 350 tonnes per day, Invicta could operate for between 10 and 15 years based on the current measured and indicated resource in the Atenea zone. However, the project is permitted to operate at 1,000 tonnes per day and the company would like to increase their resources through drilling, expand operations to the 1,000 tpd rate and build their own mill on site but for the time being will use third party transport and processing contractors. All of this could take production to over 70,000 AuEq. oz/yr, according to a cocktail napkin calculation.

Proceeds from Invicta will also be used for more exploration at its other projects in Peru — Josnitaro which is a whole other story, worthy of an update of its own.

***MiningFeeds was compensated to provide marketing services. As always, do your own diligence. The writer of this article, Nicholas LePan does own shares.

On Nov. 8, 2017, Lupaka Gold Corp. (TSX-V: LPK) received $2 million to further advance its Invicta Gold Project in Peru. This funding was Tranche 2 of the forward gold purchase agreement with Pandion Mine Finance (PLI). This is an important step on the path to production for Lupaka and is an effective alternative to equity financing that links success to production not just share price appreciation.

The receipt of this money satisfied the company’s agreement with Pandion to register the Lacsanga Community Agreement in the Public Registry system in Peru, which was completed on Nov. 6, 2017. These funds will partially go towards the widening of the road up to the site which the company hopes to complete before the rainy season in Peru.

With the registration of the Lacsanga Community Agreement now complete, the only significant conditions remaining to be completed in order to receive Tranche 3 are the requirements to put a mineral offtake agreement in place and to raise an additional US $2 million from other sources.

To meet the conditions for third and final tranche, the company entered into an agreement to sell the Crucero Gold Project to GoldMining Inc. (TSX-V: GOLD) for total approximately $6 million ($750,000 in cash and 3,500,000 shares of GoldMining).

The prepaid forward gold purchase deal with Pandion was announced at the end of June and is an attractive way to finance Lupaka’s Peruvian development project because it is non-dilutive to shareholders and has a fixed end-date.

In an interview earlier this year in the Northern Miner, Chairman of Lupaka Gold Gold Ellis outlined the strategy and benefits of this agreement.

“This is not a royalty agreement that goes on forever…We don’t pay anything for the first 15 months and we only pay them a small percent of what we produce for the next 45 months, and we’re done. It’s gone, it’s clean, there is no residual.”

Furthermore the agreement allows for a 15-month payment holiday which is important as it allows Lupaka the ability to complete development of the mine and ramp up cash flow before having to make any gold repayments.

A prepaid commodity forward agreement is where a buyer agrees to purchase a certain quality and quantity of a commodity from a producer in exchange for an upfront payment. In short, the buyer is acting as a lender in the sense that it is providing money up-front in exchange for future production.

Getting up and running will not be as onerous as other development mining projects as the company plans on using contract miners, contract trucking, and using toll milling facilities.

Tying financing to certain conditions and goals is an excellent way to ensure capital is not wasted on “general corporate purposes” plus tying financing to production is a great way to avoid dilution for shareholders. Lupaka Gold is on the path to production with a clear vision of how to fund and become the next producing mine in Peru.

On April 18, 2017, Camino Minerals Corp. (TSX-V: COR) released drill results from its copper exploration project, Los Chapitos in Peru. The company intersected in hole CHR-002 1.30 per cent copper over 106 metres, with the hole ending in mineralization, including a section of 2.12 per cent copper over 38 m and hole CHR-001 intersected 0.47 per cent copper over 76 m, including 0.67 per cent copper over 22 m. These results put the company on the radar as a company to watch. On August 25th, John Kaiser of Kaiser Research Online appeared on the Discovery Watch to discuss Camino’s results, its market activity and future prospects.

According to Kaiser, there were good results but as he studied the data it became apparent to him and the company that there was a magnetic anomaly next to hole CHR-002 which suggested there might be a sulphide body at a 200-metre depth. Combined with the data that hole CHR-002 ended in mineralization, the hope was that once they get into the sulphide body that there would be high tonnage and high grade copper in this anomaly. The next phase of drilling was designed to target this anomaly with drill hole DCH-012 (hole 12).

The results drove the company’s share price to an intraday high of $2.21 settling at $1.24 by the end of the day. However, since then the stock has retreated to 47 cents at time of publication, largely in part because the company did not find what it thought was there.

On Aug. 28, the company released results from the Adriana and Katty zones on the los Chapitos project, that included hole 12. Kaiser said that the results were not what the company was expecting. Hole 12 was great until it hit the anomaly; the mineralization very quickly faded out and the company’s theory did not pan out. As a result, the company is choosing not to use IP anomalies as a targeting-tool on this project. Nonetheless, Kaiser and the company are still optimistic about the results and the project.

The company reported drill highlights for the Adriana zone from DCH-012 which intersected 0.93 per cent copper over 96.5 metres, including 2.03 per cent copper over 19.5 m and 5.01 per cent copper over 4.5 m and which DCH-019 intersected 0.97 per cent copper over 42.0 m, including 3.31 per cent copper over 7.5 m. Some drill highlights from the Katty zone included DCH-010 which intersected 0.70 per cent copper over 43.5 m, including 1.85 per cent copper over 5.6 m and DCH-014 which intersected 1.20 per cent copper over 21.4 m, including 2.70 per cent copper over 7.9 m. It is early in the exploration program and the company has plenty of work coming up.

Kaiser believes it is a still interesting project without the sulphide anomaly. The company has about 8,000 to 10,000 metres of drilling planned at the Adriana Zone plus another 2,000 to 3,000 metres at the Katty Zone. Over the next two to three months as the company drills this trend, they will put together a resource estimate. He feels it may not be that great unless they hit something different from the current trend. In addition, the company is applying for permitting at the Atajo zone.

When Kaiser asked Ken McNaughton, President of Camino, why the company is moving forward so aggressively, McNaughton replied because they are seeing copper in all of the core. Kaiser concludes that Camino results were not as spectacular as he had hoped but the company has the cash and is marching in the right direction.

Source: http://www.howestreet.com/2017/08/25/can-inzinc-get-back-in-sync/

***The author does not own any shares in Camino and provided this report for information purposes. The author was not compensated for this article.

In a move that may ease investors concerns, Peru’s President-elect Ollanta Humala formally named Luis Miguel Castilla as Finance Minister and also announced that Central Bank President Julio Velarde would remain in his post. He first made the announcement of Castilla’s appointment on June 20th via Twitter and it was later confirmed by his Ganu Peru party in an official email today.

Humala, the controversial former army officer that sent Peru’s financial markets into turmoil, takes office on July 28th. These appointments are seen by many as an effort to reassure investors that any plans the new administration may have to raise taxes, increase mining royalties or enlarge state control will not erode economic growth.

Castilla, who served as departing President Alan Garcia’s Deputy Finance Minister, is considered to be a fiscal moderate and holds a doctoral and master’s degrees from Johns Hopkins University. Castilla is a former consultant to the World Bank and wrote a chapter on Latin America and East Asia trade strategies in a 2008 book entitled “Growth and Development in Emerging Market Economies.” Patricia Teullet, general manager of the Peruvian Exporters’ Association and a critic of Humala stated that naming Castilla is a “magnificent” sign that Humala has heard investors’ concerns.

Humala also appointed Carlos Herrera Descalzi as Peru’s Energy and Mining Minister. Descalzi most recently served as Dean of the College of Engineers. In a recent interview with Peru21 the newly appointed minister said he had already spoken with a number of mining companies and members of the National Mining and Petroleum Society who were willing to negotiate a “windfall tax” on their profits. He stated that the purpose is to meet the needs of the population and to reduce social conflicts, which have been growing faster than Peru’s booming economy. Descalzi also said, “It is a crucial issue, because the population is convinced that mining can contribute more to Peru.”

Ollanta Humala’s path to President-elect of Peru hit Peruvian mining stocks hard. As Peruvians went to the polls MiningFeeds.com looked at 10 Canadian listed mining stocks, which, on average, were already down 18.9 percent prior to his victory – CLICK HERE – for the article.

- Ollanta Humala is the President-elect of Peru.

On Sunday June 5th, 2011 Ollanta Humala won Peru’s national election over Keiko Fujimori by a tight margin, 51.6% to 48.4% with 95% of polls now reporting. On Monday June 6th, 2011, Peru’s stock market plunged 12.5%, the biggest decline on record. In the aftermath of Peru’s election investors are no doubt wondering, what’s next?

Humala’s campaign strategy mirrored Luiz Inacio Lula da Silva, who was elected president of Brazil in 2002 by persuading voters that his history as a union leader wouldn’t lead him to pursue anti-business policies that could damage the economy. Like Humala, Lula’s climb in the polls triggered a selloff of Brazilian bonds and stocks. But as he took office in Brazil, Lula moved quickly to reassure markets by naming FleetBoston Financial Corp. banker Henrique Meirelles as head of the central bank.

Mauricio Cardenas, director of the Latin America program at the Brookings Institution in Washington says, “Humala’s had enough time since the last election to see that Venezuela’s economy is a disaster while Lula has been a success in Brazil but markets aren’t going to give him the benefit of the doubt.”

Omar Chehade, Peru’s new Vice President-elect, said yesterday that in order to reassure Peruvians the country’s economic policies will remain in place, Humala may appoint in the coming days an ally of former President Alejandro Toledo to head the Finance Ministry. Toledo’s economic policies are described as neoliberal or strongly pro-free trade. Toledo’s pre-election support for Ollanta Humala was, considered by many, the tipping point in the campaign which delivered Humala the victory over Fujimori.

After the first round of Peru’s national elections, Gana Perú, the party led by Ollanta Humala, received 47 of the 130 congressional seats to be filled on July 28th, 2011 when the new government takes office. Before the runoff, Jorge Morel, a researcher at Instituto de Estudios Peruanos, predicted, “One scenario is that Ollanta Humala pacts with Perú Posible (Alejandro Toledo’s party), this would permit Humala to govern without problems.” The Perú Posible party will hold 21 seats in Peru’s Congress. Morel noted that informal alliances in previous parliaments were necessary when one party doesn’t control congress. “Informal alliances — that is, between individuals — have been a constant in Peruvian politics since the ’90s.”

Ben Ramsey, an analyst at JPMorgan in New York, wrote in a research note, “We would see a sharp selloff in Peru as a buying opportunity.” Adding that Peru’s local pension funds have “underweight” holdings of bonds while global investors have historically low positions in the country’s local and foreign-currency debt. Whereas, Alberto Bernal, head of research at BullTick Capital Markets in Miami says, “My sense is that … investors will be on the defensive. That kind of uncertainty is going to take a toll on the economy. I think Peru is going to lose at least a couple of quarters of investment.”

As reported by the Globe and Mail, TSX mining executives have their theories as well. David Garofalo, HudBay Mineral’s President & CEO, said in response to Monday’s selloff, “I think it’s a bit hysterical, frankly. He’s no Chavez … Peru has been a wide-open market economy for 20 years. So, the prospect of him nationalizing things is ludicrous.” Andrew Swarthout, CEO of Bear Creek Mining, pointed out that the industry is expecting some form of tax hike or royalty increase, up from the current rates of 30% and 3% respectively. “The current royalty structure is quite favourable and there’s room for discussion, especially given these commodity prices we’ve seen for the last five to 10 years,” Mr. Swarthout said.

Investors in Peru long TSX mining stocks have been battered since Humala’s first round victory on April 10th, 2011. Prior to the post-election selloff, a basket of 10 Canadian listed miners doing business in Peru was already down 18.9% in the days leading up to the runoff between Humala and Fujimori. In comparison, Compania De Minas Buenaventu (NYSE: BVN), the largest owner of mining rights in Peru, closed trading at $43.45 on April 8th, 2011 and, today, is currently trading at $36.09. This marks a cumulative decline in Compania de Minas’ share price of 16.9% since the Humala effect hit the Peruvian markets by storm.

Nationalist, radical, leftist. These are the labels that were thrown at Ollanta Humala before the results of Peru’s second round election gave him a new label: President-elect. So who is Ollanta Humala? A backwards iron-fisted dictator ready to plunge Peru into an economic abyss or another left-of-center South American leader trying to improve the quality of life for his nation’s poor? Only time will tell. In the meantime, you can join his Facebook page or follow him on Twitter.

A cursory look at Peruvian mining will show you that many of the world’s senior mining companies have operations there. The list of majors in the South American county includes Barrick Gold (TSX: ABX), Newmont Mining (TSX: NMC), BHP Billiton (NYSE: BHP), Freeport-McMoRan Copper & Gold (NYSE: FCX), and Teck Resources (TSX: TCK.B).

These major producers have solidified Peru’s status as the world’s largest producer of silver, second largest producer of copper, third largest producer of zinc and fifth largest producer of gold. Peru also produces molybdenum, tin, lead, iron ore and other industrial minerals.

On April 10th Ollanta Humala, a leftist nationalist, won the first round of Peru’s 2011 elections with 31.7% of the vote. The results set the stage for a runoff election this Sunday, June 5th, against Keiko Fujimori, the daughter of former President Alberto Fujimori.

Humala’s election success in Peru caught the financial markets off guard. The cost of insuring Peru’s debt against default jumped to a five-year high relative to neighboring Colombia, and the market value of Peru’s stock index plunged by roughly $18 billion in less than three weeks. The sell-off in Peruvian equities effected mining stocks around the world.

After the first round, Eduardo Suarez, a strategist at RBC Capital Markets in Toronto said the market may be overreacting and predicted Humala will lose in a second-round ballot as voters who dislike Humala will rally around his opponent. There was a precedence for Suarez’s hypothesis. During Peru’s 2006 elections, Ollanta Humala received 30.6% of the first round votes. A runoff was held between Humala and Alan García of the Peruvian Aprista Party and Humala narrowly lost with 47.4% of the votes versus 52.6% for García.

On May 12th, 2011, Reuters reported that Fujimori was leading a poll with a narrow 2.7-point lead, getting 40.6% of decided voter support to Humala’s 37.9%, which stabilized the Peruvian financial markets and resulted in a modest 1.1% recover in the benchmark stock index. One June 1st, research company Eurasia Group reported that the race had tightened considerably and was a “statistical tie“. And today, just three days before the election, Reuters reported that Fujimori’s was holding a slight lead over Humula (51% to 49%) based on the results from pollster Ipsos Apoyo. The news of the poll sent the Lima General Index up 7.2%.

Erasto Almeida, an analyst at Eurasia Group said, “Despite the tight race, the risk of serious post-election political instability is low, even though a slow counting of votes could generate significant noise in the weeks following the election.”

With an outcome that is too close to call the mining world will undoubtedly be watching the Peru election on Sunday with bated breath. MiningFeeds.com offers up 10 Peruvian mining stocks that could be real rollercoaster-rides over the next few days and weeks. We list these issuers in alphabetical order, note their minerals of interest and the percentage change in their share price since the possibility of a Humala victory has been overshadowing the markets.

1. Andean American Gold (TSX-V:AAG)

Minerals: gold & copper.

Closing price on April 8th, 2011: $0.79

Closing price on June 2nd, 2011: $0.64

Percent change: – 19.0 %

2. Bear Creek Mining (TSX-V:BCM)

Minerals: silver.

Closing price on April 8th, 2011: $10.67

Closing price on June 2nd, 2011: $6.44

Percent change: – 39.6 %

3. Candente Copper (TSX:DNT)

Minerals: copper, gold & silver.

Closing price on April 8th, 2011: $1.81

Closing price on June 2nd, 2011: $1.59

Percent change: – 12.2 %

4. Dorato Resources (TSX-V:DRI)

Minerals: gold & copper.

Closing price on April 8th, 2011: $0.57

Closing price on June 2nd, 2011: $0.315

Percent change: – 44.7 %

5. Duran Ventures (TSX-V:DRV)

Minerals: gold, silver, zinc, lead, molybdenum.

Closing price on April 8th, 2011: $0.40

Closing price on June 2nd, 2011: $0.37

Percent change: – 7.5 %

6. Fortuna Silver (TSX:FVI)

Minerals: silver.

Closing price on April 8th, 2011: $6.43

Closing price on June 2nd, 2011: $4.79

Percent change: – 25.5 %

7. Panoro Minerals (TSX-V:PML)

Minerals: copper & gold.

Closing price on April 8th, 2011: $0.46

Closing price on June 2nd, 2011: $0.49

Percent change: + 6.5 %

8. Rio Alto Mining (TSX-V:RIO)

Minerals: gold & copper.

Closing price on April 8th, 2011: $2.22

Closing price on June 2nd, 2011: $2.33

Percent change: + 5.0 %

9. Tinka Resources (TSX-V:TK)

Minerals: gold, silver, zinc & lead.

Closing price on April 8th, 2011: $0.64

Closing price on June 2nd, 2011: $0.53

Percent change: – 17.2 %

10. Trevali Resources (TSX:TV)

Minerals: zinc, lead, copper & silver.

Closing price on April 8th, 2011: $2.23

Closing price on June 2nd, 2011: $1.45

Percent change: – 35.0 %

Disclosure: at publication date Dorato Resources is a client of MiningFeeds.com.

Ollanta Humala is not a name that many outside of South America are familiar with. In 2006, however, the Peruvian Nationalist actually won the first round in Peru’s 2006 presidential vote. Although Hugo Chavez openly backed him Humala was, ultimately, defeated in a runoff 53 per cent to 47 percent by current Peruvian President Alan Garcia.

Humala was back in the news this past Sunday when, yet again, he won the first round of Peru’s elections with 31.7 % of the vote. This sets the stage for another runoff which is scheduled for June 5th, this time against Keiko Fujimori, the daughter of incarcerated former President Alberto Fujimori. On 7 April 2009, Alberto Fujimori was convicted of human rights violations and sentenced to 25 years in prison for his role in killings and kidnappings by the Grupo Colina death squad during his government’s battle against leftist guerrillas in the 1990s.

Peruvian Nobel literature laureate Mario Vargas Llosa went as far as to call the Humala-Fujimori runoff option “a choice between AIDS and terminal cancer,” given their perceived anti-democratic tendencies. Vargas Llosa was defeated by Alberto Fujimori in Peru’s 1990 elections.

The Peru election results caught the financial markets off guard. The cost of insuring Peru’s debt against default has jumped to a five-year high relative to neighboring Colombia, on concern that Ollanta Humala may win the presidential vote and expand government control over the economy. Marjorie Hernandez, a currency strategist at HSBC Holdings Plc in New York stated, “While everyone had expected this to be a non-event election, we were proven wrong. The market was not positioned that way. Everyone was long Peru everything.” Since Peru is ranked #5 on the world’s mining exploration list, the political instability is spilling over to the mining sector.

Compañía de Minas Buenaventura S.A. (NYSE: BVN), Peru’s largest publicly-traded mining company, with seven operating mines in the country, is being hit hard this week down $4.50 to $39.00 (10.3%).

Some Canadian listed Peruvian precious and base metal juniors have also been affected by the news. Candente Copper (TSX: DNT) is down $0.24 to $1.56 (13.3%), Tinka Resources (TSX-V: TK) is down $0.04 currently trading at $0.60 (6.3%); while Duran Ventures (TSX-V: DRV) has managed to buck the trend and is up half a cent.

Peru is the world’s largest silver producer, second in zinc, and sixth in gold production. Peruvian silver production totaled 135.8 million ounces in 2009. Meanwhile, zinc and gold production totaled 1.50 million tons and 6.42 million ounces, respectively. So when Humala talks about renegotiating mining contracts with foreign companies, investors naturally take note.

But Eduardo Suarez, a strategist at RBC Capital Markets in Toronto thinks the market may be overreacting. In a report on March 29th, he estimates Humala’s chance of becoming president at about 20 percent, and believes recent declines in asset prices are overdone. Suarez says “the current sell-off should be seen as a buying opportunity, but timing is key.”

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |