On August 29, Cypress Development Corp. (TSX-V: CYP) / (OTCQB: CYDVF) announced the successful completion of slurry rheology & filtration studies that are an integral part of the Pre-Feasibility Study (PFS) for the Clayton Valley clay-hosted lithium project, located immediately adjacent to Albemarle Corp.’s Silver Peak brine processing facilities in Nevada.

Management believes its U.S. location will become an increasingly valuable attribute. While many junior lithium companies like to name drop “Albemarle” and “Silver Peak,” Cypress owns 100% of one of just a few projects in Nevada that Albemarle might actually be interested in.

More promising results from Cypress’ expert technical team

Back to the latest news…. the outcome was the result of months of testing by laboratories and a detailed review with consultants & equipment vendors. This news represents a major milestone in the project because the results simplify the process flow sheet.

Cypress CEO Dr. Bill Willoughby commented in the press release,

“A critical step for us at Clayton Valley is the separation of solids & liquids. A viable process is dependent upon the ability to separate the process leach solution (PLS) from the leached residue whether by thickeners, filters, or other means. Significant test work has allowed Cypress to identify a commercially viable process, based on filtration, to take the solid-liquid separation from the laboratory benchtop to the operational scale.”

Readers may recall that Cypress released positive results from the first & second phases of its PFS metallurgical program in February & July. Since then, work has continued on other aspects of the PFS, including recovery & concentration of lithium from solution through mechanical evaporation, membrane filtration, and ion-exchange processes.

CEO Willoughby continued,

“The Cypress technical team discovered the Clayton Valley clays behave differently at varying leach conditions. By looking at the electro-kinetic potential of the clays we can select the optimal reagents & equipment. We also know under what conditions the rheology of the slurries becomes a limitation, and can design the flow sheet accordingly. With this new knowledge, we are confident we can simplify a significant portion of the leaching flow sheet.”

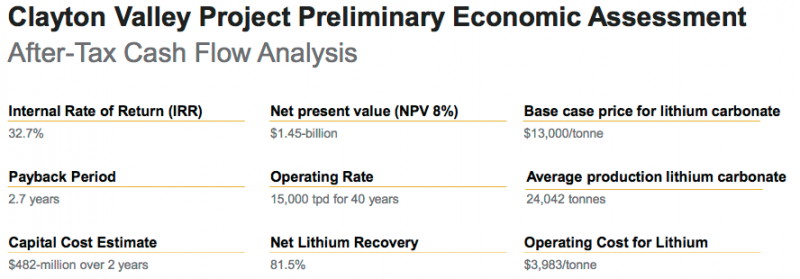

Cypress is looking at additional steps to simplify plant design with the goal to further streamline the production process and lower costs. With metallurgical & materials handling studies completed, Cypress expects to publish a PFS during the fourth quarter.

Next major milestone is a PFS in 4th quarter

It appears the PFS has been pushed back a few months. After a recent capital raise the company is comfortably funded through delivery of a PFS later this year. Come to think of it, what’s the rush? Investor sentiment remains very weak for lithium, cobalt, vanadium & graphite juniors. As long as Cypress is funded, let them keep carrying out studies to improve the PFS! Below are some highlights from the PEA.

It’s important at this point to reiterate the considerable strength of management, the Board, technical advisers & retained consultants. All of these impressive people and groups are being effectively led by CEO Willoughby, who has a Doctorate in Mining Engineering & Metallurgy from the Univ. of Idaho.

Who on earth could possibly be better to run this show than a PhD in engineering & metallurgy!?! He knows what he’s doing, and he’s a driving force behind the very good results and progress his technical team is delivering.

I asked Dr. Willoughby about last week’s news, he said,

“It’s a major technical problem to separate ultrafine clays particles < 5 microns from a leach solution. Our solution could put us in the forefront of clay-hosted lithium projects globally.”

Demand keeps increasing, supply increasingly uncertain

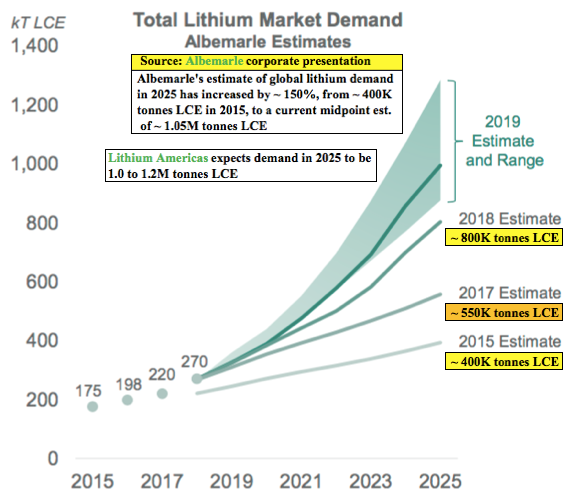

There’s a massive disconnect in the lithium world. For years, demand forecasts have been going up. The demand side of the equation — driven by both energy storage & the electrification of passenger & commercial vehicles — is likely to increase at a Compound Annual Growth Rate (CAGR) of at least 15%, perhaps 20% or more. For example, at a 20% CAGR from Albemarle’s 270K tonne figure in 2018, demand would reach 967K tonnes in 2025.

Albemarle has a particularly good graphic depicting this unmistakable trend. Four years ago they expected ~400K tonnes LCE demand in 2025. Now, Albemarle is forecasting demand of about 1 million tonnes in 2025. Likewise, Lithium Americas is forecasting between 1.0 to 1.2 million tonnes LCE demand in 2025, a range it says comes from industry producers & publicly reported forecasts.

, Finally, Fastmarkets expects LCE demand to grow from ~300K tonnes in 2019 to “at least” 1.1 million tonnes in 2025. So, a lot of forecasts in and around the one million tonne mark, but even if it turns out to be less, I think it will be a major challenge for supply to approach that level in the next six years.

The longer the project delays in Argentina / Chile brine projects, and the more project mishaps like at Nemaska, the more room there is for unconventional projects such as Cypress Development’s Clayton Valley. The market will take every battery-grade tonne of lithium chemicals produced by any company that can supply them. Lithium juniors who can make it across the production finish line will be richly rewarded.

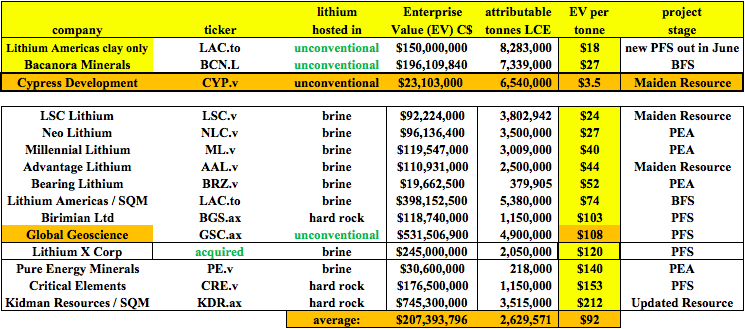

Despite significant fiscal & political challenges in Argentina that could further delay brine projects there, and continued slow movement in project development & production expansions in Chile, unconventional projects are still meaningfully undervalued compared to brine projects.

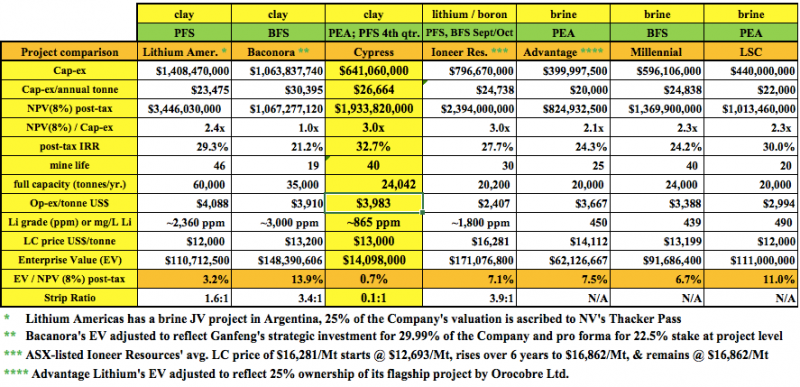

For example, Cypress Development Corp.’s enterprise value (“EV“) is less than 1% of the after-tax NPV found in its PEA. Compare that to the average 8.2% EV/NPV on the chart below. Cypress’ EV/cap-ex ratio of 3.0 times (3.0x) is 40% better than the 2.1x average of the other unconventional projects.

Cypress has the highest after-tax IRR on the chart at 32.7%, compared to an average of 26.1% among the others. And, the company’s cap-ex at C$641 million is 21% lower than the peer average.

Finally, readers should note that the Clayton Valley project has a strip ratio of 0.1 to 1. The other three projects with strip ratios average 3.0 to 1. Cypress has 1/30th the strip ratio of its unconventional peers!

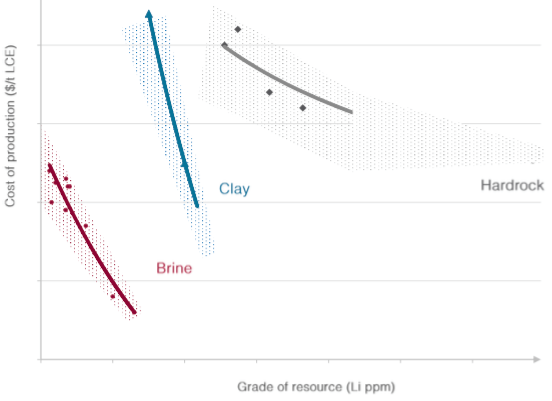

That’s a big reason why the company has attractive op-ex & cap-ex, despite having lower grade Li to work with. Another reason is the mineralogy; the Clayton Valley project’s lithium abundance is hosted in a friendlier clay than that at some of the other projects. Friendlier meaning easier and less costly to liberate the lithium into solution.

The extreme weakness in the vast majority of lithium juniors is actually great news. Great news for any lithium company hopeful that can produce lithium next decade. Great news for investors who may want to average down in their favorite battery metals names.

Brine projects have gone from, “can’t go wrong,” to “can’t fund”

A funny thing happened over the past two years. Brine projects went from no-brainers; (lowest cost, best understood, most reliable) — to the exact opposite. Solar evaporation ponds are getting less and less popular by the week, day, hour! And, unusually rainy weather in the Puna region of Argentina has negatively impacted pond yields. Speaking of Argentina….. well just read the headlines, it’s not pretty.

Chile imposed an onerous sliding-scale royalty on realized lithium prices from production in the Atacama salar. Albemarle’s & SQM’s best, lowest cost lithium brine operations…. the world’s best, may no longer the world’s lowest cost.

Brine projects were sure things and clay-hosted lithium projects were, “maybe in 10 years.” Now? Most brine projects are dead in the water, some of them never coming back to life. Even the top-quartile, most advanced projects are not getting funded. By contrast, the prospects for clay-hosted lithium projects are better than they were two years ago, albeit also difficult to fund.

Investors would be crazy not to consider unconventional assets. Brine projects, with evaporation ponds attached, will themselves be unconventional at some point in the future. The only question is when.

In early August, Glencore announced it was shutting a major cobalt / copper mine in Africa at the end of the year. Three weeks later, cobalt prices are up 30-35%. It might not take that much to get lithium prices back on an upswing. If prices were to improve, juniors like Cypress Development Corp., trading at under 1% of third-party derived after-tax NPVs, could do quite well.

Peter Epstein

September 13, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker / dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this interview was posted, Peter Epstein owned shares of Cypress Development Corp., and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any future events & news, or write about any particular company, sector or topic. [ER] is not an expert in any company, sector or investment topic.

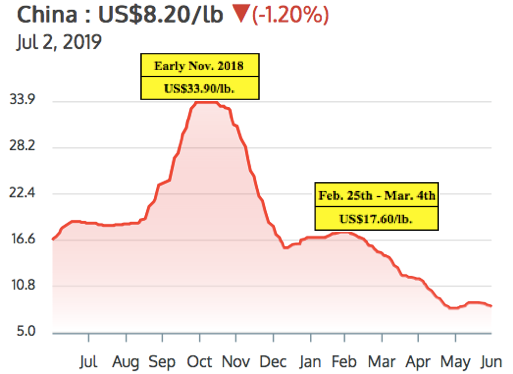

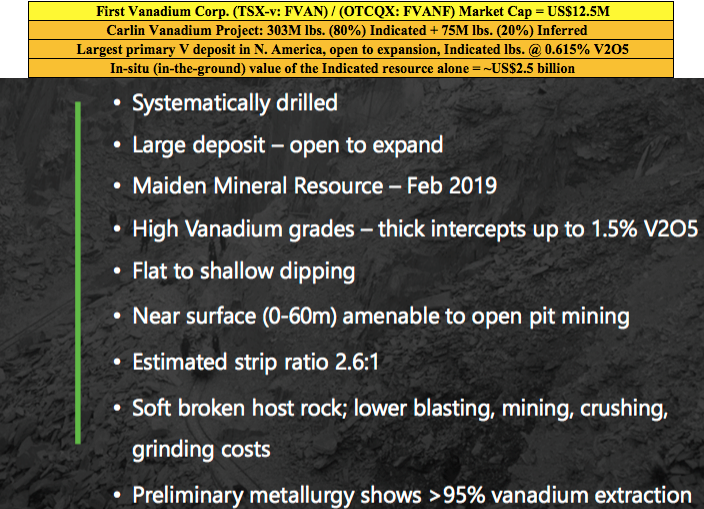

First Vanadium Corp. (TSX-V: FVAN) / (OTCQX: FVANF) has been under pressure, along with hundreds of battery metal juniors and the underlying metals including vanadium, cobalt, lithium. Even vanadium giant Largo Resources is down 61% from its 52-week high. Yet, if one believes in vanadium, it’s hard to ignore First Vanadium’s shares at C$0.44, down 78%! The pro forma Enterprise Value [market cap + debt – cash] is just US$12.8M. The Company has C$1.9M in cash.

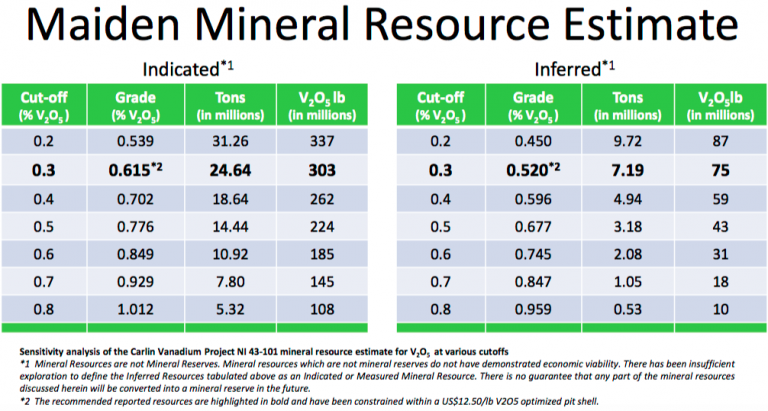

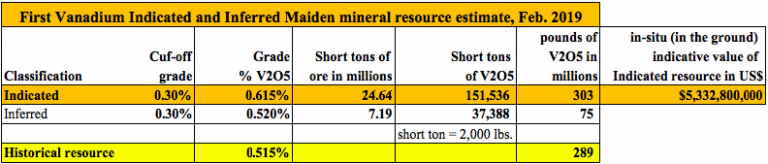

Yet, even at current vanadium pentoxide (“V2O5“) prices, the in-situ value of the Indicated-only portion (303 million pounds) of the Company’s estimated resource is ~US$2.5 billion. Management believes it has the largest high-grade primary vanadium resource in North America.

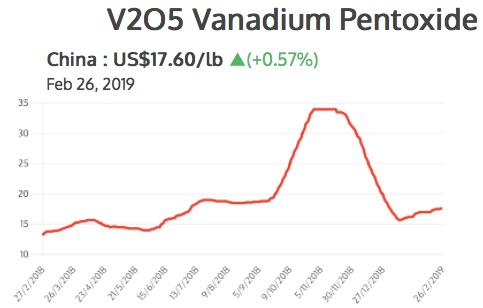

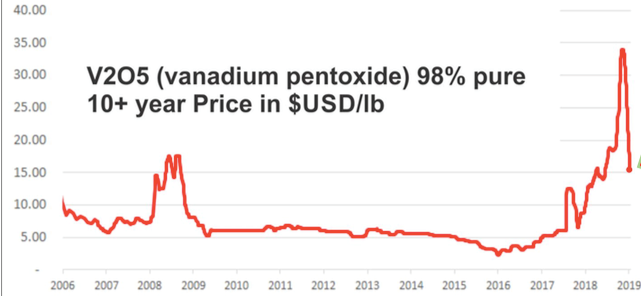

There has been a lot of weeping and gnashing of teeth over the V2O5 (China) price falling from a 2019 high of US$17.6 to its current US$8.2 per pound. But, as the saying goes, the cure to low prices is…. low prices. Few new projects make sense at today’s levels. I believe that V2O5 (China) between US$10-US$15 per pound might be a sweet spot, good for both producers and end users.

Steel companies can afford to pay higher prices for V2O5, but grid-scale, Vanadium Redox Flow Battery (“VRBs“) Energy Storage Systems (outside of China) might need prices below US$10/lb. to go mainstream. Importantly though, VRB plant costs are coming down. Vincent Sprenkle, a lead researcher at the U.S. Department of Energy’s Pacific Northwest National Laboratory, (“PNNL“) recently said, “VRB costs could be lowered by another 50%.” That would be very bullish for vanadium prices, it would allow for widespread adoption of VRBs even with V2O5 prices above US$10/lb.

First Vanadium has a sizable resource, a good grade, in a great jurisdiction. A Preliminary Economic Assessment (“PEA”) is expected by year end. The following interview of Paul Cowley, P.Geo., President, CEO & Director of First Vanadium, was conducted by phone & email between June 24th & July 2nd.

Please tell us about yourself and your team.

I’m an exploration geologist with 40 years’ experience in the discovery & evaluation of mineral deposits around the world. About half of my career was with a Major, BHP Minerals. I was involved in leading the team in the Canadian arctic that made 4 gold deposit discoveries that generated about 6 million ounces of gold. I also worked at Escondida and BHP’s Ekati diamond mine during their exploration days.

I’m a senior guy, but I’m the youngest of our group. The others have even more years of experience. We have two mining engineers that held mine general manager positions of very significant mines at Majors. We have four metallurgists that have worked for Majors, in senior roles. We have a construction engineer who’s built 20 mines in North & South America, he’s currently building Lundin’s mine in Ecuador.

What do you make of the recent volatility in the vanadium price?

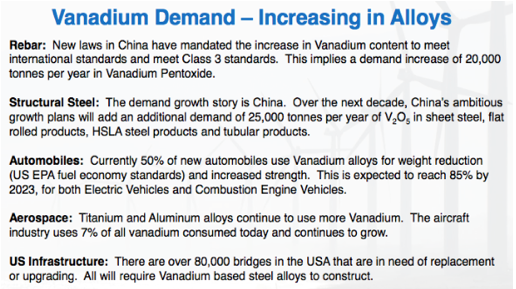

Since early March 2019 the vanadium price has taken an unexpected turn lower. Prices are not responding to the bigger picture demand and supply imbalance. Chinese steel plants did not recharge their vanadium inventories in this period, as many expected they would, putting pressure on traders to liquidate at undercutting prices, but they will have to restock. The U.S.-China trade wars, and some shortfall of enforcement of new Chinese rebar standards, appear to have exacerbated the situation in the short term.

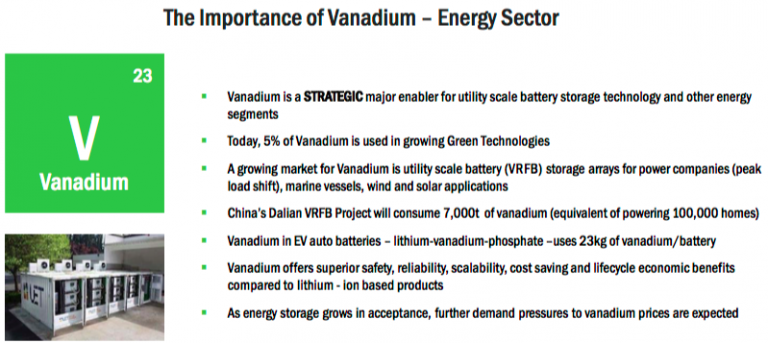

It’s our view that the fundamentals of demand in global steel applications will outstrip supply and should push vanadium prices higher again in the second half of the year, and beyond. Adding to the demand side is the exciting boom in solar & wind projects, all of which require battery storage. This is happening on so many levels around the world that we expect to see the vanadium battery carve out a healthy market share in this expanding renewable space. Some are calling the 2020’s, the Solar Decade.

Please explain the significance of the historical data you recently received, that extended the strike length by 300 meters to the south.

It means more potential than we had expected. From our drilling, the deposit appears to be open to expansion in several areas, but we did not expect the deposit to be open to the south. The newly acquired data demonstrates a 15% strike length increase to the south and it’s still open in that direction. This is exciting news as this data was not included in the resource estimate we put out in February.

You already have a 303 million pound vanadium resource (in-situ value of ~US$2.5 billion) in the Indicated category alone. Does the resource need to get any bigger?

That’s a good question. But it needs to be answered through an economic study. In our view, the resource is sizable. It’s currently the largest, highest-grade primary vanadium resource in North America. Our immediate priority is to demonstrate potential economic viability with what we have, knowing that we believe we could always make it bigger if and when we need to.

Several readers may assume that First Vanadium will need an expensive roaster in its operating flow sheet. What are your latest thoughts?

Not true. The path we are on with our metallurgical flow sheet does not include, or require, a roaster.

Although Nevada is the #1 global mining jurisdiction in the latest Fraser Institute Mining Survey, some complain that it takes a long time to get permits. What does your team expect in this regard?

In general, in the U.S. that is true, but not in Nevada. Nevada has a responsible review and process, but it’s a mining state. And, even more so for us now that vanadium is on the critical minerals list. The U.S. has unveiled its strategy in an effort to rebuild struggling domestic supply chains for metals & minerals it deems “critical” to the country’s manufacturing & defense sectors. Recently this was reiterated when President Trump & Prime Minister Trudeau announced a plan for the U.S. & Canada to collaborate on critical minerals.

What are the latest developments on the metallurgical front?

We continue to make strides on the metallurgical front. In April we announced an average of 95% vanadium extraction from the rock across the deposit, into solution. We do not know what ultimate recoveries will look like just yet, but we are making good progress. And, we’re making strides in the area of pre-concentration, with the aim to reduce the plant size, which would lower the capital intensity of the project.

What are First Vanadium’s plans for a Preliminary Economic Assessment (“PEA”)? Might that be a 1H 2020 event?

No, we think that we can move faster, our aim is to initiate a PEA in the 3rd quarter, with results to be reported before the end of the year.

Why should readers consider buying shares of First Vanadium?

I see very good value and upside; an exceptional senior technical team, a good share structure and a great project. We now have C$1.9 million in cash with the recent private placement closing, and 42.4 million shares. Our share price now is where it was at the beginning of 2018! Yet, we have delivered two successful drill campaigns, a mineral resource with considerably higher grades, and more metal in the ground than our historical resource, and 80% (303 million pounds) of it is in the Indicated category.

That, plus positive metallurgical test work and environmental baseline studies to advance permitting. If one is bullish on the vanadium price, currently at US$8.20/lb., then First Vanadium’s (TSX-V: FVAN) / (OTCQX: FVANF) project in the #1 of 84 ranked global jurisdiction of Nevada should be high on the list of projects to consider investing in.

Thank you Paul, very interesting and timely commentary on the vanadium market and on First Vanadium. I look forward to seeing a PEA later this year!

Peter Epstein

Epstein Research

July 9, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Vanadium Corp., including, but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Vanadium Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of First Vanadium Corp. and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

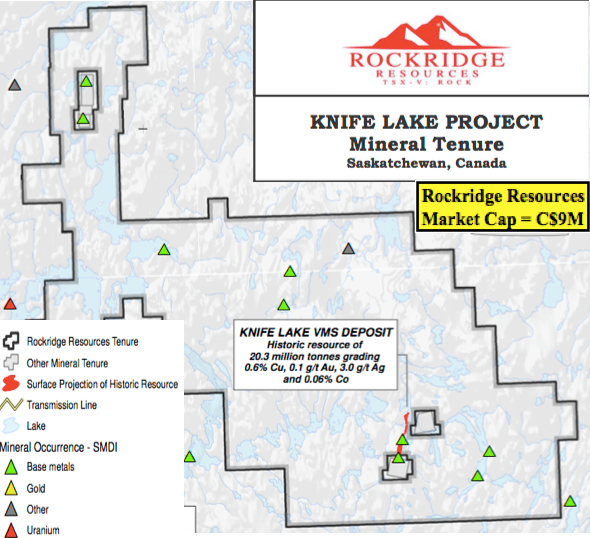

Rockridge Resources (TSX-V: ROCK) / (Frankfurt: RR0) is an exploration company focused on acquiring, exploring & developing mineral resource properties in Canada. Its focus is copper & base metals; more specifically — base, green energy & battery metals — of which copper is all three. Not just in any place, only top-tier mining jurisdictions such as Saskatchewan. And, only in mining districts that have had significant past exploration, development or production. And, only projects in close proximity to key infrastructure. Rockridge’s management team, Advisors & Board expertly and methodically eliminate many of the risk factors, early on, that can kill projects. This is a tremendous team for a company with a market cap of just C$5.6M / US$4.2M.

New CEO Bolsters Already Strong Team

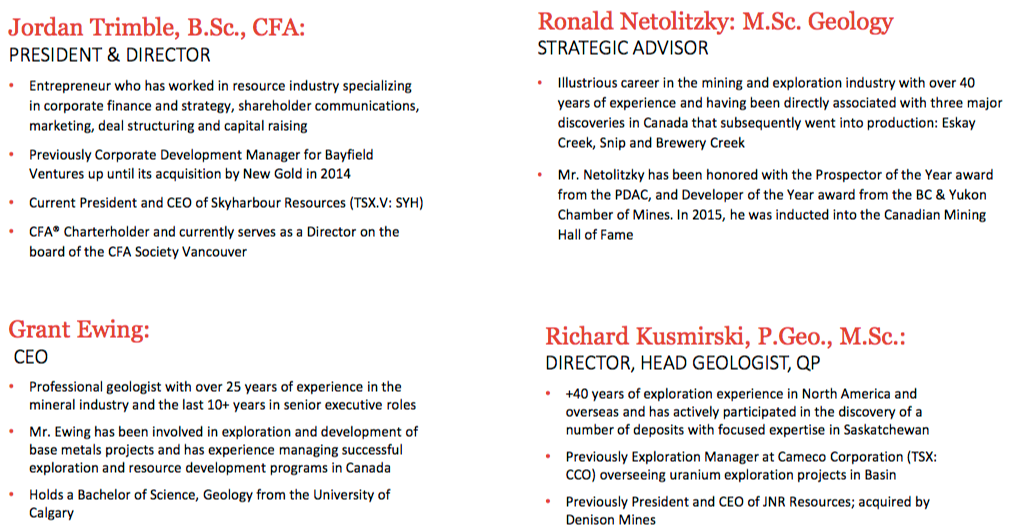

Late last month, Rockridge appointed Grant Ewing, P.Geo to be its new CEO. Jordan Trimble remains as President & a Director. Grant has more than 25 years’ experience in the Metals & Mining space. His expertise covers the mine development cycle, from early stage exploration through to production. I spoke with Grant last week and was impressed with his very extensive knowledge of base metals and his understanding of the district that hosts the Company’s Knife Lake project. Grant seems to be an ideal person to help advance the Project and make new discoveries. Please see more about CEO Grant Ewing, P.Geo here.

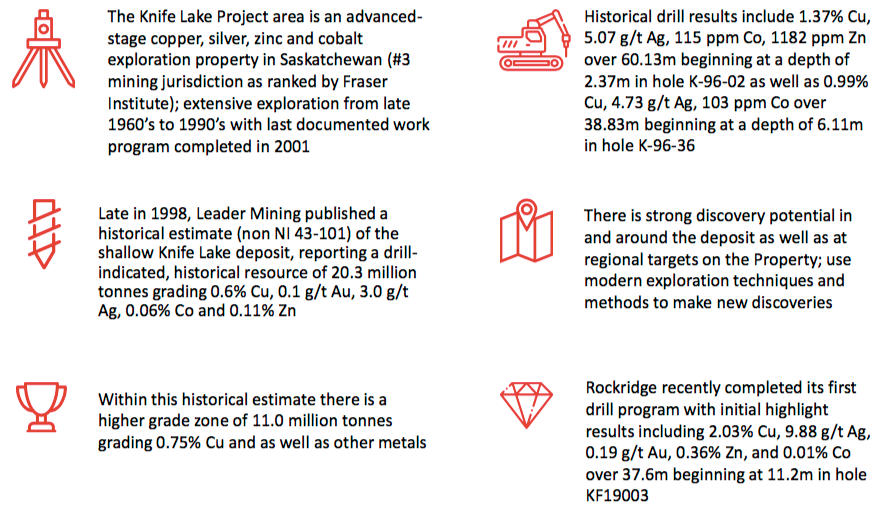

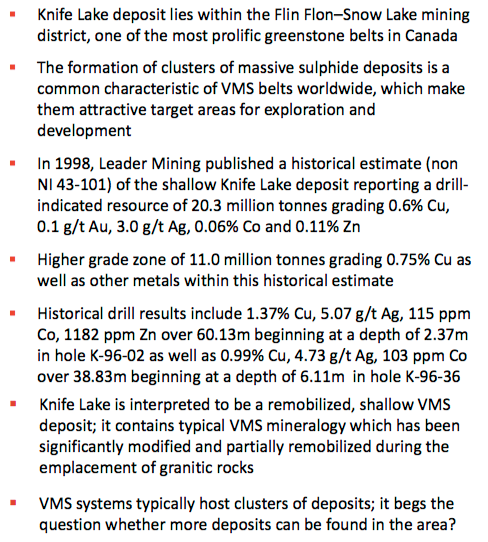

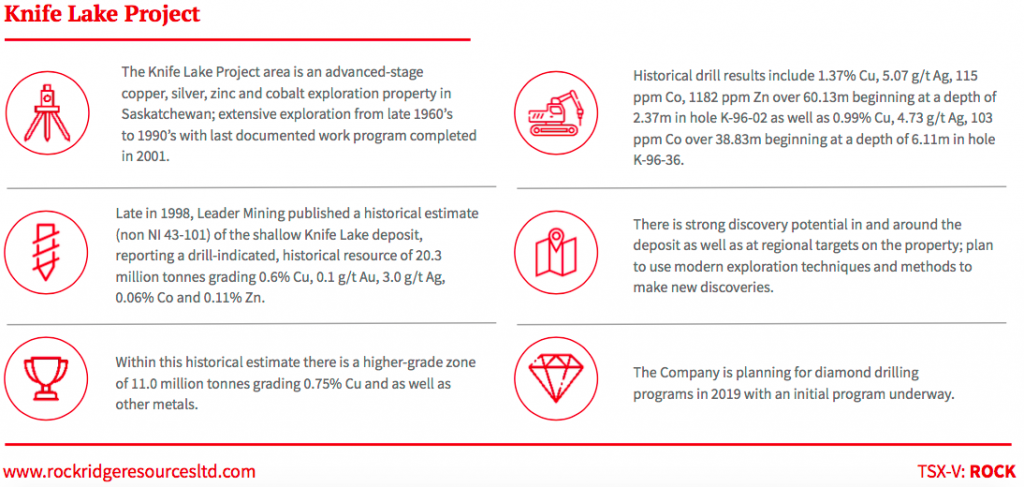

The Company’s flagship project, Knife Lake, is in Saskatchewan, Canada, (ranked 3rd best mining jurisdiction in the world) in the Fraser Institute Mining Company Survey. The Project hosts a near-surface, (high-grade copper) VMS copper-zinc-silver-gold-cobalt deposit, open along strike and at depth. Management believes that there’s strong discovery potential in and around the deposit area, and at additional targets on roughly 85,200 hectares of contiguous claims. As a reminder, Rockridge has an option agreement with Eagle Plains Resources to acquire a 100% Interest in the majority of the Knife Lake VMS deposit.

Flagship Project, Knife Lake, 12 Drill Hole Results Now in….

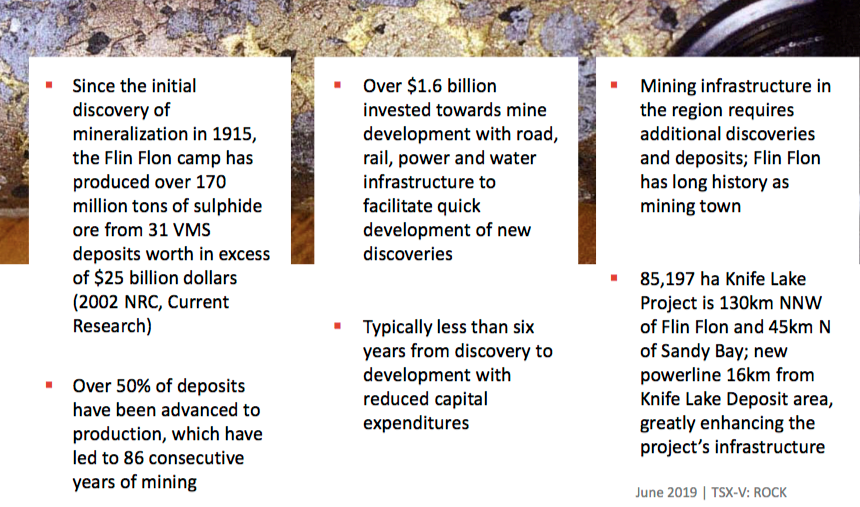

The Project is within the famous Flin Flon-Snow Lake mining district that contains a prolific VMS base metals belt. Management believes there’s tremendous exploration upside. The goal? High-grade discoveries in a mineralized belt that could host multiple deposits, as VMS–style zones often contain clusters of mineralized zones. Of course, the trick is finding them.

However, no modern exploration, drilling method or technology has been deployed at Knife Lake. It was discovered 50 years ago and last explored in the late 1990s. Airborne geophysics, regional mapping & geochemistry was done, but technologies have improved. Management believes that modern geophysics; high resolution, deep penetrating EM & drone mag surveys to cover large areas in detail, could make a big difference.

Earlier this year, Rockridge drilled 12 holes for a total of 1,053 meters. Importantly, this represents the first significant work on the property since 2001. Readers may recall from reading past articles & interviews on Epstein Research & Equity.Guru & Aheadoftheherd, and viewing videos of then CEO Trimble, that the Company’s primary goal is to explore districts that have been under-explored, never explored, or not recently explored. Management’s highly skilled & experienced technical team & advisors deploy the latest exploration technologies & methods. A lot has changed in 18 years; a simple example would be the use of lower-cost, high resolution drones to fly various surveys.

These 12 assays, added to the historical database, will generate a new NI 43-101 mineral resource estimate in late July or early August. This will be a major milestone that will hopefully draw the attention of prospective strategic partners. Subsequent to that de-risking event, Rockridge is funded for a Summer exploration program, that will likely stretch into Fall. The goal is to identify & refine targets at depth and regionally. Modern vectoring techniques will be deployed, using metal ratios & structural interpretation to identify “primary” VMS deposits.

Other modern methods include high-resolution geophysics, deep penetrating EM to identify conductors, and drone mag surveys to cover large areas in detail. Finally, ground work & sampling will be conducted, analyzing rock geochemistry to identify prospective VMS style hydrothermal systems. Importantly, very limited previous drilling was done below 100m, but of the deeper holes, several intersected mineralization at around 300m. Could they be mineralized lenses?

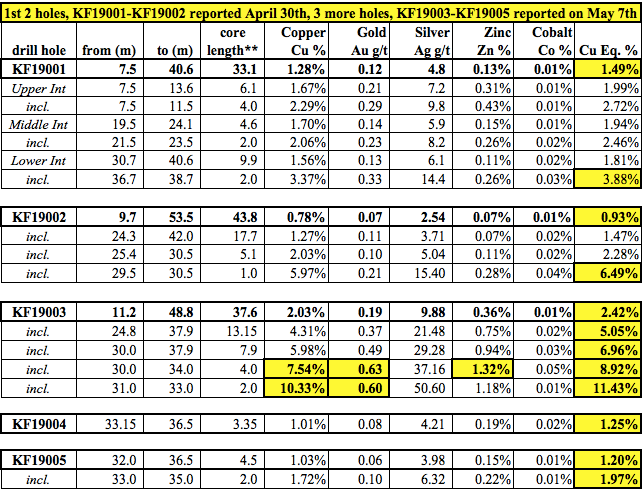

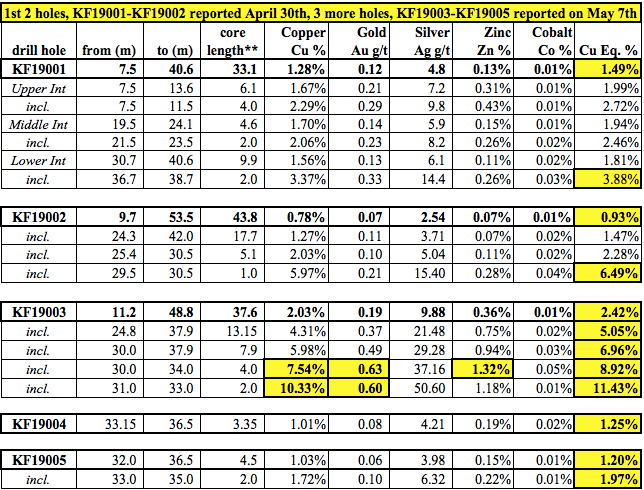

Last month Rockridge reported additional results from its Winter diamond drill program. The first 5 holes are shown in the chart above. Readers may recall that a key takeaway was that holes KF19001 & KF19002 largely confirmed historical grades, intercept widths & geological conditions. Hole KF19003, reported on May 7th, was a blockbuster, 37.6m of 2.42% Cu Eq., significantly better than the first 2 holes. KF19003 had a grade (Cu Eq.) x thickness (in meters) value of 91, compared to 41 & 49. Importantly, it confirmed high-grade mineralization up-dip of KF19002 in an area where no historical drilling is known to have been done. Therefore, this assay, and perhaps nearby assays to follow, could potentially increase the size & grade of the upcoming mineral resource estimate.

Best Intercept in Last 7 Holes: 15.2 m of 2.45% Cu Eq.

In a press release June 10th, holes KF19006 thru KF19012 did not contain any blockbusters, but 6 of 7 were nicely mineralized with Cu Eq. values ranging from 0.46% to 2.45%. The interval widths averaged nearly 8 meters. The best intercept was 15.15 m at 2.45% Cu Eq. in hole KF19006. This intercept is a good one, like those found in holes KF19001 & KF19002, reported in the April 30th. press release. Importantly, KF19006 tested the up-dip extension of the Knife Lake deposit in an area that had not been previously tested. Likewise, hole KF19007 tested the down-dip extension of the deposit near KF19006. KF19007 intersected a solid 2.95 m of 0.82% Cu Eq. grade. The latest property map provided from today’s press release is too large to fit comfortably within this article, please click on link here.

Rockridge’s CEO, Grant Ewing commented:

“The Knife Lake property package is highly prospective for new discoveries using modern exploration techniques & methods given the lack of recent field work. The known deposit is thought to be a remobilized portion of a presumably larger primary VMS deposit, and there is excellent potential for deposit expansion at depth which we plan to test in future programs. Furthermore, there are several high quality targets to test on the expansive landholding, and there have yet to be satellite deposits discovered in the vicinity as VMS systems often host clusters or stacked deposits.”

Something I found interesting was the 2 portions of the 15.2 m intercept in KF19006 that assayed 7.25 m of 0.72 g/t Gold, (from 8.75 to 16.0 m), and 5.0 m of 0.93 g/t Gold, (from 11.0 to 16.0 m), both within 16.0 m of surface. Those 2 grades (true widths undetermined) are the highest Gold values reported to date. The 0.93 g/t showing is nearly 50% higher, and 1.0 m longer, (5.0 vs. 4.0 m) than the next highest grade Gold showing, in blockbuster hole KF19003. While intriguing, these values in isolation may not amount to much. Still, they’re worth keeping an eye on.

Rockridge’s President & Director, Jordan Trimble commented:

“The results from this first-pass drill program have exceeded our expectations with almost all drill holes having intersected high-grade copper mineralization, and in doing so, we have successfully confirmed the tenor of mineralization reported by previous operators, while expanding known zones of mineralization. We are working towards issuing an NI 43-101 compliant resource estimate as well as planning a regional summer field program, both of which will provide steady news flow and catalysts over the near term. We will continue to execute on our value creation strategy of going into overlooked but prospective projects in prolific mining jurisdictions and using modern exploration methodologies to test new ideas and make new discoveries.”

The deposit remains open at depth. Additional discoveries are very possible as the property is nearly 85,200 hectares in size and vastly under-explored. The Winter drill program gives the Company’s technical team valuable information about geology, alteration & mineralization that will be applied to regional exploration targets. The Company is now working towards completing an NI 43-101 compliant resource estimate for Knife Lake with the results from this drill program. A summer exploration program is also being planned, details to follow.

Conclusion

As mentioned, Rockridge Resources (TSX-V: ROCK) / (Frankfurt: RR0) has a tremendous team — Management, Board & Advisors — for a company with a market cap of C$5.6M = US$4.2M. Readers should take just 5-10 minutes to review the Company’s new June Corporate Presentation. And, the latest press releases can be found here. The flagship Knife Lake project is large enough, at ~85,200 hectares, to keep the Company busy for years to come. Even if management were to farm out (get free-carried) a portion of the Property, there would still be tens of thousands of hectares remaining to explore in a top mining district in Canada.

Copper prices are down into the US$2.60’s/lb. from close to US$3/lb., but near-term fluctuations in the price are meaningless for anyone who believes that copper is needed for, 1) clean-green energy storage, 2) the global electrification of passenger & commercial vehicles, and 3) the surge of infrastructure building needed to accommodate a growing global middle-class population migrating to ever-larger cities. Not to mention the re-building of old and destroyed infrastructure like buildings, roads & bridges. Everything uses copper, everything will continue to use copper. The price of copper has to rise, or there won’t be enough copper, it’s that simple. Several experts believe that the copper price is headed to US$4-$5/lb. by 2020 or 2021. If so, a company like Rockridge Resources has a lot of leverage to that outcome.

Peter Epstein

Epstein Research (ER)

June 13, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] about Rockridge Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Rockridge Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock in Rockridge Resources and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

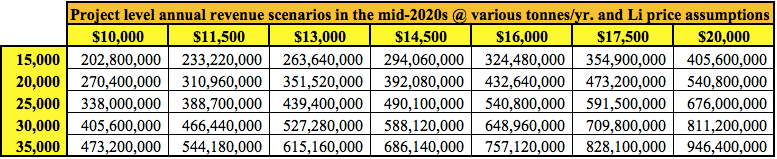

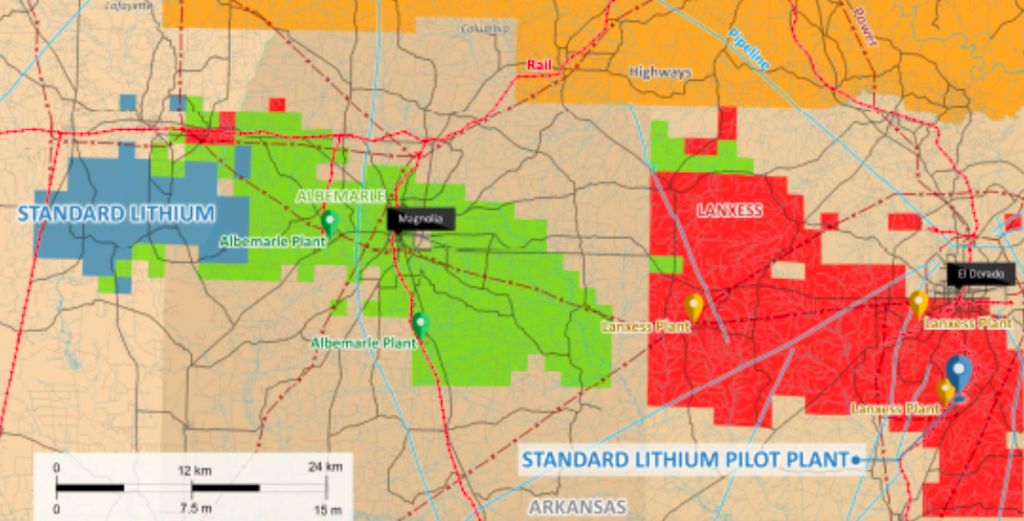

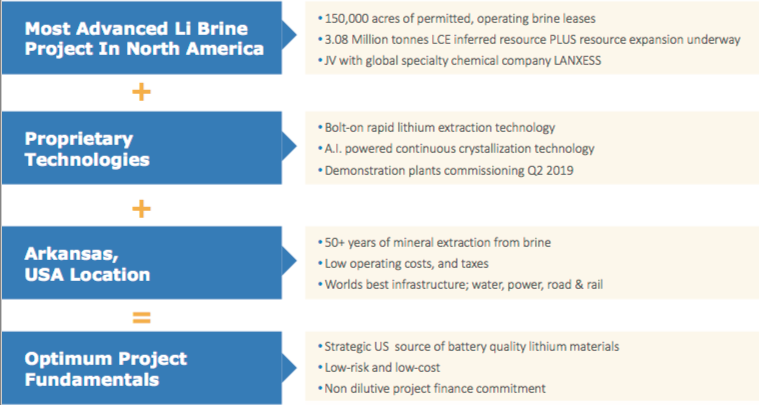

Standard Lithium Ltd. (TSX–V: SLL) / (OTCQX: STLHF) shares are caught up in a battery metals sell off, but is it warranted given recent positive developments, ongoing supply challenges in the Lithium Triangle & exciting near-term Company catalysts? Its Arkansas Project could reach commercial production by 2022, and ramp up to ~20K tonnes/yr. of Lithium Carbonate, bolting onto brine streams from 3 existing facilities, to feed a central crystallizer plant by the mid-2020s. [a crystallizer is standard equipment made by multiple manufactures, used in many commercial applications, to convert a solution into a solid material] In this case, the solid material would be a high-purity, finished lithium product.

After successful bench & mini-pilot scale testing, Standard Lithium is at Demonstration Plant stage. The Demo Plant being constructed by Zeton Inc. is a 20 m x 20 m x 11 m tall, industrial-scale modular facility designed to process tail brine from the Lanxess South Plant in southern Arkansas. Lanxess is a leading European specialty chemicals company with > 15,000 employees in 33 countries. It develops, manufactures & markets a wide range of specialty chemicals & plastics. Last year, sales were nearly C$11 billion.

The Demonstration Plant is based on Standard Lithium’s proprietary technology that uses a solid sorbent material to selectively extract lithium. The Plant is designed to continuously process a flow of tail brine at 50 gallons per minute from the Lanxess South Plant, equivalent to annual production of 100-150 tonnes Lithium Carbonate. The Demo Plant is designed to be expanded to commercial scale early next decade.

Dr. Andy Robinson, Standard Lithium President & COO, commented in a June 3rd press release,

“The Standard Lithium team is very pleased with both the speed of execution and the exceptional quality and attention to detail that Zeton are bringing to our Demonstration Plant. We are very confident that we will be delivering a high-quality plant to the project site in southern Arkansas, and we look forward to integrating it into Lanxess’ brine operations. We are progressing very quickly on the ground, and hope to announce real progress in project implementation in the near-future.”

With all the doom & gloom around lithium pricing, even at current pricing of ~US$11.5K per tonne, 20K tonnes of Lithium Carbonate/yr. = US$230M = ~C$311M revenue at the Project level. There are possible scenarios to produce up to 30K tonnes/yr., for 25+ years by the 2H of the 2020s. Subject to a formal JV between Standard & Lanxess — in exchange for 100% funding of commercialization costs (hundreds of millions of CAD$ over several years) — by Lanxess; Standard Lithium will end up with 30%-40% of the Project. That’s a win-win for both companies in my opinion.

I believe that lithium carbonate pricing will improve early next decade, perhaps meaningfully, as forecasts for the global electrification of commercial & passenger transportation and the deployment of large-scale Energy Storage Systems, continue to rise.

On the other hand, long-term lithium supply is highly uncertain. Brine projects in Argentina & Chile are coming, but they’re delayed due to funding & other challenges. Claimed project capacities of 20-40K tonnes of Lithium Carbonate/yr. may never be attained, look at Argentina’s Orocobre Ltd., after 4 years, it’s running at ~72% of nameplate capacity.

Of roughly 12 potentially viable brine projects in Chile & Argentina, I assume 4 won’t make it and the other 8 are delayed by an average of 2 years. I then pencil in a 4-yr ramp up period to 75% of stated project capacity. Under those assumptions, if 450K tonnes/yr. was expected from the Lithium Triangle in 2025 — what we might see, instead, is 225K tonnes/yr. in 2028! This means security of supply (from the U.S., Canada & Australia) will be of critical importance. Speed to market will be rewarded handsomely with long-term contracts at strong prices.

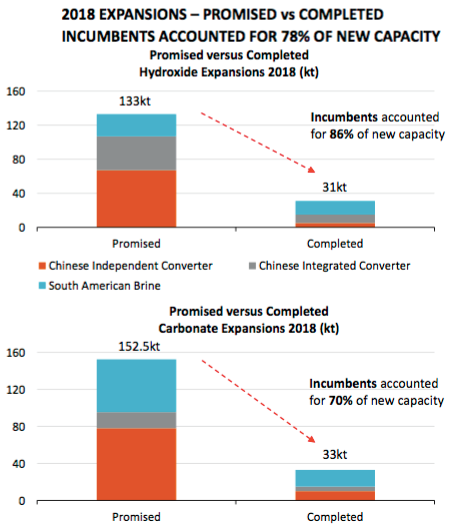

In the chart below we see a review done by Orocobre of 2018’s expectations vs. reality, a combined 78% shortfall in hydroxide & carbonate expansions. 285.5K tonnes of new supply expected, 64K tonnes delivered. We see this year after year after year…. when will the market catch on? This can only be good news for lithium pricing going forward.

Any lithium company, be it brine, hard rock, clay or “unconventional;” that can reach production by early next decade, will be in the driver’s seat. I believe that Standard Lithium, with JV partner Lanxess could be in commercial operation by 2022. The Lanxess project has been de-risked in a number of important ways. I hope that readers & investors in lithium companies are starting to understand that risks avoided can add considerable value to a project. However, one risk still at large is technology & scale-up risk. With that in mind, I spoke at length with Standard Lithium’s President & COO, quoted above, Dr. Andy Robinson. Robinson has 20+ years’ experience as a Geoscientist and has a PhD in Geochemistry. No one is better suited to be in the position he’s in.

Please tell us about your background and what brought you to Standard Lithium.

I’m a PhD Geochemist who worked in the engineering consulting world for 10 years, and then as an entrepreneurial project developer in the mining & power space for the last decade. Robert (CEO Robert Mintak) and I worked together at Pure Energy. When we took over management of Standard Lithium in the spring of 2017, we had a very clear vision of what we wanted to build. We took our experience in the lithium business, both in terms of modern technology and project development goals, and looked for the ideal project. The ideal project had to have:

The right location for a modern approach,

Existing infrastructure at the project site – not 100’s of km away…

The right partner,

Minimal permitting & environmental risks, and

A globally significant resource

This was the only way we could realistically hope to get a project into commercial production within 5 years versus the usual 10 or more years.

How did your team choose a process technology to move forward with?

We took an agnostic approach to processing technology. The project drives the process. We started by understanding project fundamentals, then we developed a flow sheet that would work for our specific project in Southern Arkansas. Our process development work was guided by the philosophy that we didn’t just want it to work in a lab – we wanted a robust flow sheet that could work economically at commercial-scale.

Please describe the steps your team went through at the bench and mini–pilot plant stages.

At the bench-scale, we worked with large volumes of real brine from the project – we then tested a whole range of different technologies, ranging from those already in commercial use, through to novel and experimental technologies, to determine which general ‘suite’ of technologies would work best with our brine’s characteristics. We quickly determined that a modern alternative to the types of technologies developed in the 1970’s & commercialized in the 1990’s would be the ideal solution.

So, we spent the time at bench-scale solving chemistry problems of selectively extracting lithium from the brine – then we ran 2 programs of mini-pilot work to build our understanding of the process engineering. One was done at a batch-scale, then we scaled that up and ran it on a continuous basis. Now, in June 2019, we’ve just completed 2 years of test work on our southern Arkansas brines.

What were the key takeaways from each stage?

At the bench-scale – we learned that direct lithium extraction from the tail brine using a highly selective solid sorbent was the way to go. At the mini-pilot-scale – using both chemical & process engineers from a wide range of disciplines — allowed us to develop the simplest, most efficient flow sheet we could, at a reasonable cost. We’re using equipment and processes already in use around the world, at very large commercial-scale, in complementary existing industries.

Please describe Standard Lithium’s upcoming Demonstration Plant, what do you hope to achieve?

The upcoming Demonstration Plant will be final proof-of-concept for our Project – it’s a large Plant, that can be scaled directly to a commercial facility. It’s designed to process up to 50 gallons per minute of tail brine from Lanxess’ South Plant, and produce at a rate of 100-150 tonnes of lithium carbonate per year, so about 10 to 12 tonnes per month. We hope to scale our Demo Plant up to 9,000-10,000 tonnes/yr. during the first phase of commercial execution.

If all goes as planned, Standard Lithium could be in commercial operations in 2022? 2023? Do you have a goal?

We’re aiming for a commercial decision in the first half next year, and our goal is to be in commercial operations by 2022. I should add that 2022 is aggressive, but achievable – as opposed to the aspirational targets suggested by other brine projects. Some of those projects are years away from a Bankable Feasibility Study, and then will require several more years to design, permit, win over local communities, obtain funding, construct solar evaporation ponds, regional infrastructure like roads, and build a processing facility.

Many companies are suggesting 3-year ramp up periods to full capacity, but if history is any guide, it will probably be longer. So, Standard Lithium could reach initial commercial operations years before some, if not most, of the brine projects in the ‘Lithium Triangle.’ If true, we would hope to lock-in long-term contracts (through Lanxess) at very favorable pricing.

Might you be able to sell lithium output into specialty niche–markets that command premium pricing?

That’s a great question. If one looks at Lanxess’ business model, it centers around taking raw materials and converting them into a large variety of tertiary products that maximize the value obtained from their feedstock. They do these conversions using their global specialty chemicals expertise. Several niche lithium chemicals command high margins and typically are served by a small number of manufacturers. Lanxess is a leading global specialty chemical company, they know how to: a) build & operate a chemical plant, and b) extract maximum value from their chemical feedstock!

What would you like to say to readers who are still unsure about your operational flow sheet?

We think there’s still a general misunderstanding in the lithium industry about lithium processing technology. There’s a pervasive thought that evaporation ponds are conventional and therefore ‘safe,’ and that anything different is high-risk. In reality, each evaporation pond project is unique, each has initial, and ongoing, chemical & operational challenges; Orocobre is an example of taking the traditional approach and not delivering battery-quality, or nameplate capacity.

Interestingly, FMC (now Livent Corp.) has been successfully operating an ‘alternative’ lithium-selective sorbent technology (similar to ours) in Argentina since the 1990’s. Standard Lithium (TSX–V: SLL) / (OTCQX: STLHF) is not engaging in a high-risk processing technology – we’re simply making incremental improvements to what has already been done successfully for decades.

Once people see our onsite Demonstration Plant in continuous operation later this year, I think perceptions will change as to our technology being unconventional. We don’t have untested technology, we have customized technology, specifically designed with our project fundamentals in mind. The project drives the process. It took years of hard work and millions of dollars, but we think we’re about to cross the finish line regarding proof-of-concept. That should turn a lot of heads.

Peter Epstein

Epstein Research

June 6, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Standard Lithium, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Standard Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Standard Lithium and it was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

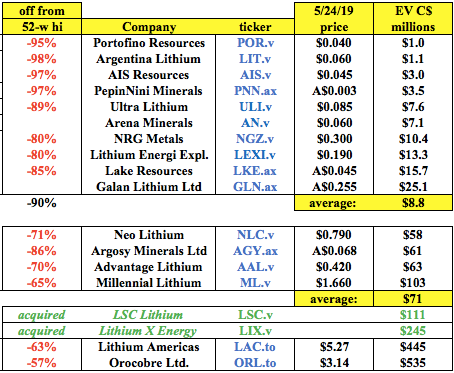

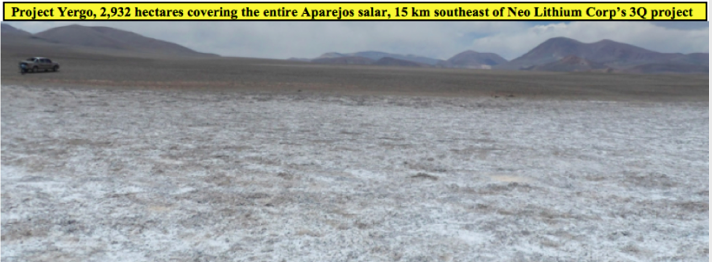

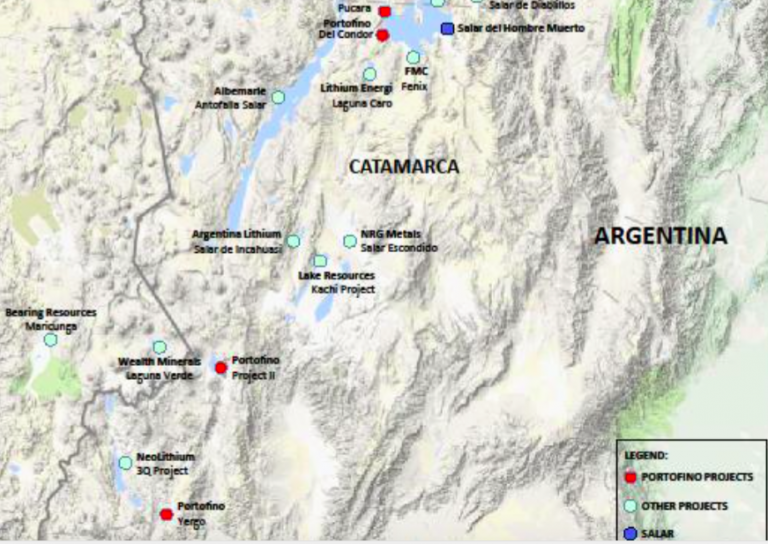

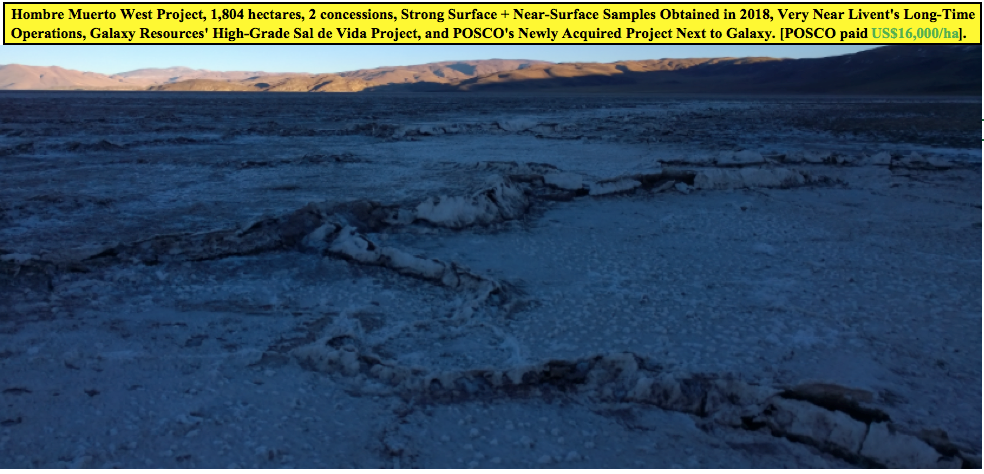

On May 27, Portofino Resources (TSX-V: POR) announced initial sampling results at its Yergo lithium brine project that covers the entire Aparejos Salar in the Province of Catamarca, Argentina. Yergo is within 15 km of Neo Lithium’s high-grade, PFS-stage 3Q Project. Before getting to this important company news, a quick recap of Portofino.

The Company controls 3 projects in Catamarca, covering > 8,600 hectares, via low-cost, 4-yr. options. Through the end of 2020, total cash outlays are < $65K, for all 3 projects. There are no work commitments or royalties. Portofino’s most advanced (initial drilling this summer) asset is the 100%-controlled, 1,804-hectare Hombre Muerto West project. Close neighbors in the Hombre del Muerto Salar include– Livent Corp. (formerly FMC), POSCO, and Australian-listed Galaxy Resources. POSCO paid ~$375M to Galaxy for 17,500 hectares in Catamarca province, that’s ~$21,400/ha. If POSCO, Galaxy, Livent Corp., Lithium Americas, Albemarle, SQM, Ganfeng, Orocobre Ltd. or smaller players like Neo Lithium, Millennial Lithium, Argosy Minerals, Advantage Lithium and Galan Lithium, were to pay half of what POSCO paid (per hectare) for 1/3 of Portofino’s 1,804 hectares in Hombre Muerto; that would equate to 6x the Company’s current market cap of C$1M. As a reminder, of 18 surface samples taken at the Hombre Muerto West project last year, 2 were > 1,000 mg/L Li, averaging 1,026 mg/L Li, 4 were > 800 mg/L Li, averaging 935 mg/L Li and 6 were > 700 mg/L Li, averaging 871 mg/L.

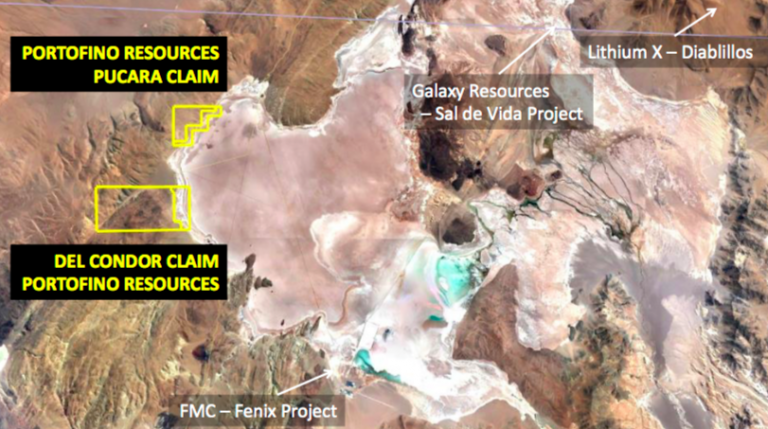

A Second Project, Named Project II, Looks Promising as Well….

Portofino can acquire 85% of Project II, which is 3,950 hectares in size and located 10 km from the Chile border (see map above) and 65 km northeast of Neo Lithium’s 3Q project. Historical exploration work included near-surface brine samples that averaged 274 mg/L Li, with several in excess of 300 mg/L Li. Project II captures the whole salar, has relatively easy access, and has returned consistent surface / near-surface sampling results over a wide area. The Maricunga project (BFS completed) is located just across the Chile border. Maricunga is billed as the highest grade, undeveloped brine project in the Americas.

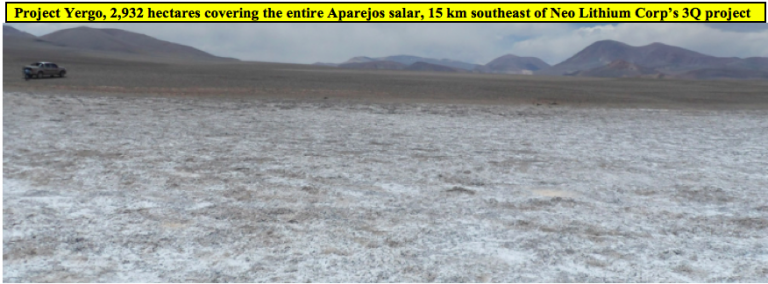

Last, but not Least, Yergo, Subject of the May 27th News

Portofino has the right to acquire a 100% Interest in the 2,932 hectare Yergo lithium brine project. The property covers the entire Aparejos salar {see map above}. Earlier this year, surface & near-surface brine sampling & geological mapping were done. Twenty-two locations were sampled, returning values up to 373 mg/L Li and up to 8,001 mg/L Potassium (“K“). The sample sites averaged 224 mg/L Li, 4,878 mg/L K and 184 mg/L Magnesium (“Mg“.) The average Mg:Li ratio of the 22 samples is a very low 0.8:1. Due to unusually high levels of water in the salar, 16 of the 22 samples were taken from the southeast portion of the salar. Those 16 samples averaged 278 mg/L Li, 6,091 mg/L K and 86 mg/L Mg. The average Mg:Li ratio of the 16 samples is extremely low at 0.4:1. Most projects in Argentina have Mg:Li ratios of 3.0 to 3.5 to 1.

According to the press release, one sample taken from the northwestern portion of the salar returned a value of 351 mg/L Li, indicating a potential area of elevated near-surface Li brines up to 3 km in length by 1-2 km in width. Additional sampling will be required to better test the central portions of the area. Management intends to complete additional sampling once surface waters have evaporated to allow for less-diluted brine samples. Due to the close proximity of the salars comprising Neo Lithium’s 3Q Project and Portofino’s Yergo project, geologists studying Yergo believe it’s likely that they have similar geological histories and are similarly enriched in Lithium & Potassium.

David Tafel, Portofino’s CEO stated:

“We are encouraged with these very good, initial lithium and potassium sample results combined with extremely low magnesium/lithium ratios. As soon as weather permits, our geological team will continue their exploration work to follow up on the potential surface extent of the mineralization.“

Conclusion

Although the main event is drilling in June/July at Hombre Muerto West, these surface sample results from the Yergo project are certainly promising. Portofino is slowly but surely, without burning too much cash, advancing multiple projects. In a better battery metals market or a better lithium juniors market, I believe that the optionality embedded in Portofino’s 3 projects would be valued higher. Perhaps a lot higher. A C$1M market cap is a cheap entry point to see a few drill holes in one of the best lithium enriched salars on the planet. A proven salar with long-term existing production and advanced-staged development projects underway.

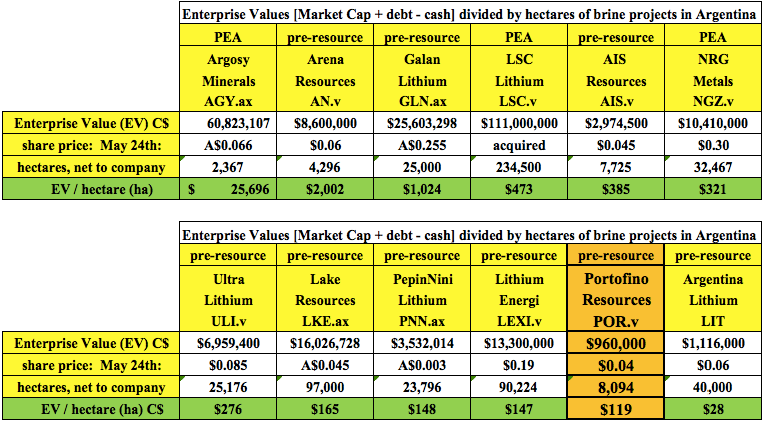

The following chart is another look at relative valuation. I calculated each company’s Enterprise Value per hectare. Portofino is the 2nd cheapest by this measure. To be fair, this is not the best metric, because not all hectares are of equal quality, or equally far advanced. For instance, some of the companies below have Preliminary Economic Assessments (“PEAs“) on select projects. However, I believe that Portofino’s 3 projects have the potential to be Company-makers (it’s easy to be a Company-maker when your market cap is C$1M). By contrast, some of the companies below have projects and green field properties in provinces or salars that have shown poor or mediocre drill results. Mediocre doesn’t make the grade in this market!

To be clear, Portofino Resources (TSX-V: POR) is a very high risk investment opportunity, it has not drilled a single hole yet. But several of the companies listed above have properties in less attractive salars, have experienced drilling problems, reported unimpressive grades, narrow brine intervals or announced small resources. One company reported a resource of just 66,000 tonnes of Indicated & Inferred lithium carbonate! Portofino could end up with mediocre drill results, or run into problems, but with a market cap of just C$1M, it might be worth taking drilling risk for the possibility of good, or very good, drill results, and perhaps a better lithium junior market later this year.

May 29, 2019

Peter Epstein, Epstein Research

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Portofino Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Portofino Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Portofino Resources and Portofino was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

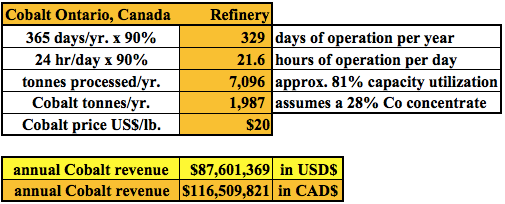

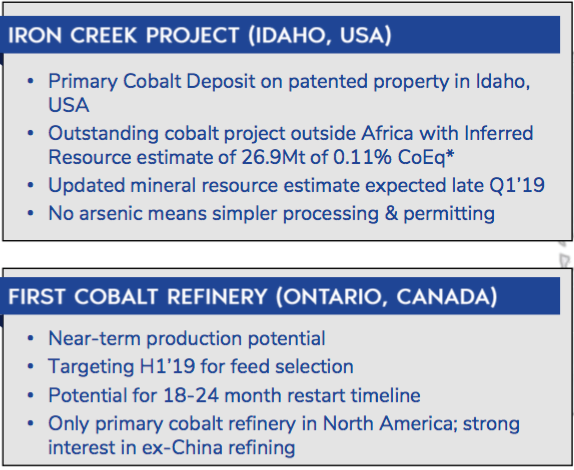

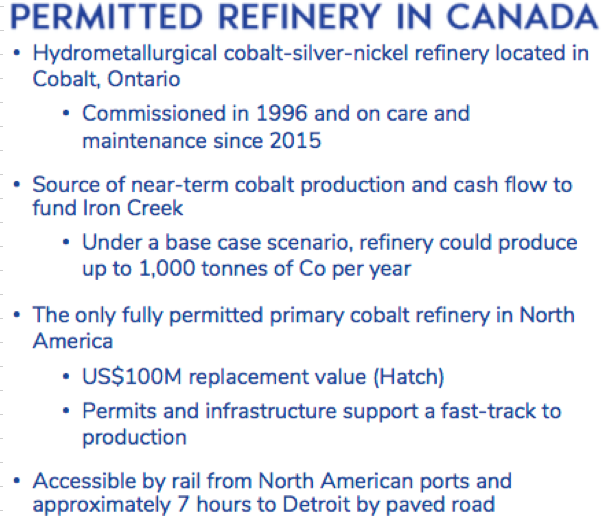

This is big, really big. I can’t say that it’s a surprise that Glencore might want to partner with First Cobalt Corp. (TSX-V: FCC) / (QTCQX: FTSSF), but it would be by far the best possible outcome for management’s strategic review of its 100%-owned refinery in Ontario. Shareholders & prospective investors were understandably growing nervous about First Cobalt’s ability to deliver the restart funding with little or no additional equity issuance. Not because of management, because the battery metals sector is a complete disaster. Everyone knows that the Cobalt price is down a lot, did you know that Vanadium is down 73.5% in 6 months? This news alone, if this agreement is consummated, could mark a turning point for select Cobalt juniors. {See full press release here}

Glencore adds tremendous credibility to First Cobalt’s Refinery

In addition to the potential for significant revenue (C$100M+ at US$20/lb. Cobalt) and good, very good or great EBITDA margins (depending on the Cobalt price), this would open A LOT of doors for the company. They would instantly become the premier pure-play, North American Cobalt junior, not that there are many left to choose from. First Cobalt could solidify its leading position by acquiring other companies & assets. Might eCobalt Solutions (TSX: ECS) be first on the list !?! eCobalt might now prefer the embrace of First Cobalt over a takeover by Australian-listed Jervois Mining. I have no insight on this, I’m just reflecting on the recent acquisition of ECS shares.

At the risk of getting ahead of myself, this is a MOU not a signed, sealed & delivered deal, I continue with the benefits of an agreement between First Cobalt & Glencore. Glencore adds increased credibility to First Cobalt, the management team and the refinery. It would be a supreme vote of confidence. Outside of North America, First Cobalt might not be a very well-known name. That would change overnight, in fact it might be changing as I write this sentence…. First Cobalt would attract additional world-class executives. The company could pay a dividend! My quick math suggests that a 5% dividend yield would be possible from 50% of the cash flow on 2,000-2,500 tonnes of production at US$20/lb. Cobalt.

Glencore would greatly de-risk Refinery restart & attract attention to FCC.v

It’s amazing what Glencore would bring to the table that no one else possibly could. It appears from the press release that Glencore might provide a loan for up to US$30M, all of the capital needed, to restart the refinery. In addition, Glencore would provide technical assistance in bringing the refinery back into production, for instance they would, “collaborate on final flow sheet design.” Glencore would source up to 100% of the feedstock. The refinery is a hydro-metallurgical Cobalt facility in the Canadian Cobalt Camp of Ontario. It has the potential to produce either a Cobalt Sulfate for lithium-ion batteries, or Cobalt metal for the North American Aerospace industry and other industrial & military applications.

Taking this news a step further, if the restart were to be a success, guess who would be there to help (if feasible) ramp up operations from 2,000-2,500 to perhaps 4,000-5,000 tonnes/yr.? Glencore is to Cobalt what Albemarle and SQM are to Lithium. Yes, closing on this agreement would be really, really good for shareholders.

Assuming that Glencore is on board, the refinery would likely be up and running sooner than otherwise would be the case. And, once the world realized that a Cobalt Refinery was coming online in Canada in 2021, and that produced Cobalt would to be ethically sourced from mine to finished product, end-users would be very interested in speaking with First Cobalt. First on the list of visitors to see CEO Trent Mell would likely be execs from the automakers. The company has already signed NDAs with a number of them. Next to visit? Li-ion battery makers. Both automakers and battery companies need ethically sourced Cobalt for genuine moral considerations, for public relations and for security of supply.

As per the press release,

“With no cobalt sulfate production in North America today, the First Cobalt Refinery has the potential to become the first such producer for the American electric vehicle market. The Company has signed confidentiality agreements with several automotive companies interested in securing cobalt for the North American market.”

I have to remind myself that this is a MOU, not a done deal, but I think the chances of it getting done are pretty high. First Cobalt & Glencore have likely been talking about the refinery for months now, if not longer. And, although I’ve outlined the many benefits for First Cobalt shareholders, Glencore benefits as well. Over time, if the refinery could produce 5,000 tonnes of Cobalt products, and Glencore controls that off-take, that’s a meaningful amount, probably > 10% of the battery-grade Cobalt processed / refined & sold outside of Africa & China.

Speaking of China, recent news shows that geopolitical risks are alive and well with China hinting at restricting the free trade of rare earth metals from China to the U.S. It doesn’t matter who’s to blame, how the U.S. and China got here, all that matters are the potential consequences. Today it’s rare earth metals, will China threaten to stop exporting lithium & cobalt next? I doubt that China would sell to Canada or Mexico if there was an embargo against the U.S. for rare earth metals, lithium, cobalt, vanadium, graphite, etc.

But now I’ve veered off course, this isn’t about China… The news today is about Glencore signing a MOU with First Cobalt Corp. (TSX-V: FCC) / (OTCQX: FTSSF) to help design, re-engineer, refurbish & commission the company’s Cobalt refinery in Ontario. Glencore could deliver up 100% of the feedstock needed to produce 2,000-2,500 tonnes of finished Cobalt. And, Glencore is considering paying the entire US$30M cost (in the form of a loan to First Cobalt Corp.) to get it up and running again. This is the biggest news of the year for the Company. This is important news for the Cobalt sector. Let’s see if this marks a change in sentiment for Cobalt juniors.

May 24, 2019

Peter Epstein

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Cobalt Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Cobalt Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of First Cobalt Corp. and the Company was an advertiser on Epstein Research [ER].

Readers should consider me biased in favor of the Company and understand & agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Rockridge Resources (TSX-V: ROCK) is a fairly new mineral exploration company focused on the acquisition, exploration & development of mineral resource properties in Canada. Its focus is copper & base metals. More specifically, base, green energy & battery metals, of which copper is all three! Not just any place in Canada, world-class mining jurisdictions such as Saskatchewan. And, not just good jurisdictions, but in mining camps with significant past exploration, development or production, in close proximity to key mining infrastructure.

The company’s flagship project Knife Lake is in Saskatchewan, Canada, (ranked 3rd best mining jurisdiction in the world) in the Fraser Institute Mining Company Survey. The Project hosts the Knife Lake deposit, a near-surface, (high-grade copper) VMS copper-cobalt-gold-silver-zinc deposit open along strike and at depth. Management believes there’s strong discovery potential in and around the deposit area, and at additional targets on ~85,000 hectares of contiguous claims.

On May 7, Rockridge reported additional results from its Winter diamond drill program at its flagship Knife Lake project in Saskatchewan. Hot on the heels of last week’s press release (April 30th) of 2 holes, comes 3 more. I was planning on writing an article on those excellent results, but Equity.Guru beat me to the punch, putting out this well done piece. Readers following along may recall that the key takeaway was that holes KF19001 & KF19002 largely confirmed historical grades, intercept widths & geological conditions. Fast forward to May 7th, and management’s interpretation of drill holes KF19003, KF19004 & KF19005 was announced. Results on the remaining 7 holes will be released over the next 20-30 days. As a reminder, Rockridge has an option agreement with Eagle Plains Resources to acquire a 100% Interest in the majority of the Knife Lake Cu-Zn-Ag-Au-Co VMS deposit.

Earlier this year, Rockridge drilled 12 holes for a total of 1,053 meters. Importantly, this represents the first work on the property since 2001. Readers may recall from reading past articles & interviews on Epstein Research and Equity.Guru and viewing videos of CEO Trimble, that the company’s primary goal is to explore districts that have been under-explored, never explored, or not recently explored. Management’s highly skilled and experienced technical team & advisors deploy the latest exploration technologies & methods. A lot has changed in 18 years; a simple example would be the use of drones to fly various surveys.

Whatever management is doing seems to be working, as evidenced by 2 of the first 5 holes returning very strong results, and the third hole, KF19003 a true blockbuster.

Hole KF19003 was even better than the first 2 holes. In fact, significantly better, with a grade (Cu Eq.) x thickness (in meters) value of 91, compared to 41 & 49. Make no mistake, KF19001 / 19002 were great, they averaged 1.21 Cu Eq. over an average 38.5m. But, KF19003, WAS something to write home about…. [if under the age of 30, Google the idiom, “nothing to write home about“]. Near-surface like the first 2 holes, the 37.6m interval assayed 2% Cu, 0.2 g/t Au, 9.9 g/t Ag, 0.36% Zn & 0.01% Co, for an estimated 2.42% Cu Eq. grade. 2% Cu over 37.6 meters is a tremendous showing at under 41 meters downhole.

Holes KF19004 & KF19005 were mineralized, but had narrower intercept widths of interest. Still, there were attractive Cu Eq. grades (1.25% & 1.20%, respectively). Interestingly, Gallium (up to 25.6 ppm) & Indium (up to 15.2 ppm) values were found in the mineralized zones of all 3 holes. Those 2 Rare Earth Metals trade at an average of about US$300/kg. Each 10 ppm = 1kg/tonne. KF19004 & KF19005 confirmed mineralization up-dip of historically drilled high grade mineralization. So, those 2 holes were like KF19001 & KF19002, important in building the potential resource size. All activities are advancing the Project toward a NI 43-101 compliant mineral resource estimate later this year.

Perhaps best of all, drill hole KF19003 confirmed high-grade mineralization up-dip of KF19002 in an area where no historical drilling is known to have been done. Therefore, this assay, and perhaps nearby assays to follow, will increase the size & grade of the upcoming mineral resource estimate. There were also encouraging zinc values, incl. 4m (from the 37.6m) of 1.32% Zn, nearly C$50/tonne rock. Gold values up to 0.63 g/t are interesting, but like the zinc, I’m referring to only the best grades, from smaller intercepts. That 4m interval I mentioned also had 7.54% Cu. This is clearly a COPPER deposit, Knife Lake is a near-surface, high-grade Cu project. See drill hole results from KF19001 – KF19005 below. Holes KF19001 & KF19002 were released on April 30, and KF19003-KF19005 on May 7.

Rockridge’s President & CEO, Jordan Trimble commented: “The results from drill hole KF19003, specifically 2.42% Cu Eq. over 37.6m, far exceeded our expectations and represents one of the best holes ever drilled on the project. It is important to note that this drill hole was collared in an area where no historical drilling has been reported. As such these drill results are expected to have a positive impact on the historical resource. Final results from the remaining 7 drill holes are pending and will provide steady news flow over the near term.”

Drill indicated intercepts (core length) are reported as drilled widths and true thickness is undetermined. {details about calculation of Cu Eq. grade can be found in the press release}.{details about calculation of Cu Eq. grade can be found in the press release}.

From the press release, “The Knife Lake area saw extensive exploration from the late 1960s to the 1990s with the last documented work program completed in 2001. Between 1996 & 1998, Leader Mining completed 315 diamond drill holes, outlining a broad zone of mineralization occurring at a depth of less than 100 m. Late in 1998, Leader published an historical estimate, reporting a, “drill-indicated” resource of 20.3 M tonnes, grading 0.6% Cu, 0.1 g/t Au, 3 g/t Ag, 0.06% Co & 0.11% Zn. Within the historical estimate there is a higher grade zone containing 11.0 M tonnes of 0.75% Cu, plus other metals.”

NOTE: These mineral resource estimates are not supported by a compliant NI 43-101 technical report. A qualified person has not done the work to classify these estimates as current mineral resources in accordance with NI 43-101 standards. Furthermore, the categories used for these historical resource estimates are described as, “drill-indicated”. This is not a NI 43-101 resource category, but based on the methodologies & drill hole spacing, management believes it would likely be classified as Inferred.

The Project is within the word famous Flin Flon-Snow Lake mining district that contains a prolific VMS base metals belt. Management paid < half a penny/lb. of copper and they believe there’s tremendous exploration upside. The goal? High-grade discoveries in a mineralized belt that could host multiple deposits, as VMS-style zones often contain clusters of mineralized zones. Of course, the trick is finding them. No modern exploration, drilling or technology has been deployed at Knife Lake. It was discovered 50 years ago and last explored in the 1990s. Airborne geophysics, regional mapping & geochemistry was done. Management believes that modern geophysics; high resolution, deep penetrating EM & drone mag surveys to cover large areas in detail, could make a big difference.

The deposit remains open at depth. Additional discoveries are very possible as the property is > 85,000 hectares in size. The winter drill program marks the end of the beginning of this highly prospective project. Importantly, the program gives the company’s technical team valuable information about geology, alteration & mineralization that will be applied to regional exploration targets. According to the press release, most of the historical work was shallow drilling in and around the deposit area. Very little regional or district work has been documented. In fact, there wasn’t even much drilling done below the deposit. That’s why management is optimistic about discovery potential both at depth and regionally. I’m excited to see what the next 7 assays add to the Rockridge Resources (TSX-V: ROCK) story!

Peter Epstein

May 9, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein about Rockridge Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Rockridge Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock in Rockridge Resources and the Company was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

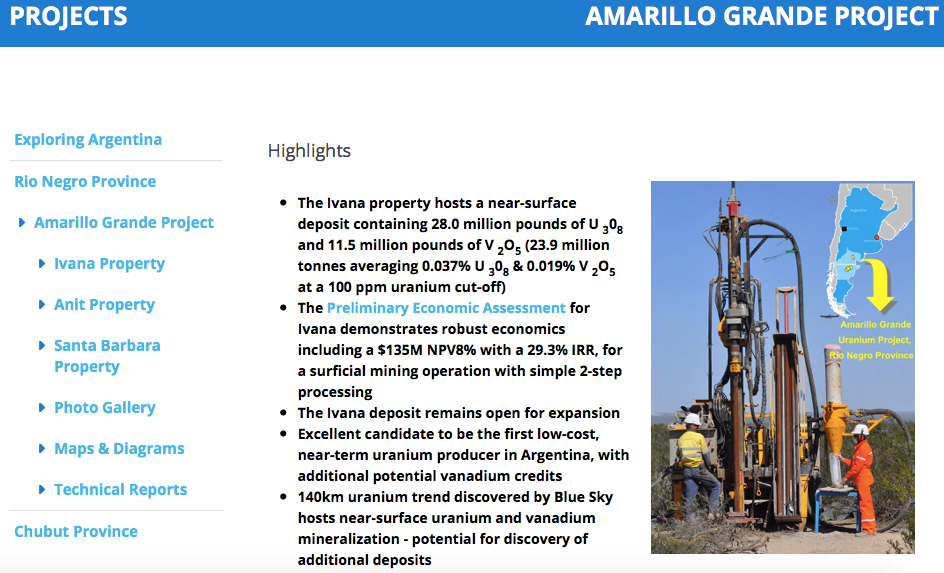

In February, Blue Sky Uranium (TSX-V: BSK; OTC: BKUCF) delivered a very positive Preliminary Economic Assessment (“PEA“) on the Ivana uranium-vanadium deposit at the Company’s 100%-owned Amarillo Grande project in Argentina. The after-tax IRR & NPV is 29.3% & $135M. The upfront cap-ex is estimated at $128M. Importantly, the all-in sustaining cost is estimated to be in the lowest quartile of the global cost curve, at $18.27/lb. The resource contains nearly 23M pounds uranium, plus 12M pounds vanadium. These indicative economics are based on just a 13-yr. mine life. The metrics are strong, but they could get even better. CEO Niko Cacos has stated in recent interviews that the next C$2-$3M capital raise (probably in May) will fund them into the 4th quarter, and pay for well over 100 shallow drill holes that could potentially double the resource size.

The Company is well on its way to a larger resource. On April 29, Blue Sky Uranium reported,

“additional high-grade uranium & vanadium results from pit sampling carried out in the area immediately west of the Ivana Uranium-Vanadium deposit, at the Company’s wholly-owned Amarillo Grande Project in Rio Negro, Argentina. This newly-identified near-surface mineralization is open to expansion, as indicated on Figure 1, (https://bit. ly/2IZknLO) but drilling is required for further testing as the target zone is interpreted to be at greater depth in adjacent areas.”

Doubling the resource would provide a strong foundation for a blockbuster Pre-Feasibility Study (“PFS“) next year. Ultimately, management believes there’s potential for > 100 M pounds uranium, which might include > 50 M pounds vanadium. That would take longer to drill out, so I’m assuming a doubling in the next 9 months and a PFS completed in about a year from now. In my opinion, all else equal, a PFS could show an after-tax IRR > 35% and all-in sustaining costs of $16-$17/lb. The mine life could be extended to 20+ years, or annual production of uranium + vanadium in the initial 10 years could be significantly increased.

Therefore, if management is correct in their belief that a doubling of the resource is possible by 1H 2020, then the current market cap of C$20M = US$15M could be an attractive entry point. If over a longer time frame the Company could triple, quadruple or quintuple the current resource, then instead of bottom quartile costs, they could be looking at a project in the bottom decile. However, they don’t need to spend the time & money this year or next to get anywhere near 100 M pounds of uranium on the books. They have to deliver a strong PFS and then assess the uranium market at that time. If the market has improved, I think that Blue Sky could start production by 2022.

Uranium & vanadium prices over the past 6 months have had a negative impact on company share prices. Uranium bottomed at about $17.5/lb. in 2016, but rebounded to a bit over $29/lb. in Q4 of last year. Sentiment started to shift, momentum seemed to be gaining, but the spot price stalled. It now sits at close to $26/lb. Likewise, vanadium had a tremendous run, from about $3/lb. 3 years ago to just shy of $34/lb. in early November, 2018. Since then vanadium pentoxide (China price) has fallen to ~$12/lb., down 65%. As an aside, cobalt is off about 62% from its 52-week high.

Most analysts & industry pundits believe that both vanadium & uranium prices are headed higher by year-end and higher again in 2020. For vanadium, a price between $10-$20/lb. could be the new normal. Blue Sky doesn’t need a high vanadium price, it’s just icing on the cake. At $10/lb., it doesn’t help project economics all that much. At $20/lb. it has a moderately favourable impact. The PEA uses a $15/lb. price assumption.

Everyone talks about the spot price when they discuss uranium. The spot price is ~$26/lb., but the long-term contract price is quoted at $32/lb. {See Cameco’s pricing page}. Notice that the spread between contract & spot prices over the past 4.25 years ranged from 7% to 89% and averaged 37%. Currently the spread is about 23%. All Blue Sky needs to start production early next decade is $10/lb. more in the spot price, which would likely translate to a contract price in the mid $40’s/lb. The Company doesn’t need that price this year, or even next year. Early 2021 would be perfect timing.

According to the PEA, Blue Sky’s Project has a 20% IRR at $40/lb., and that will likely improve in the upcoming PFS.