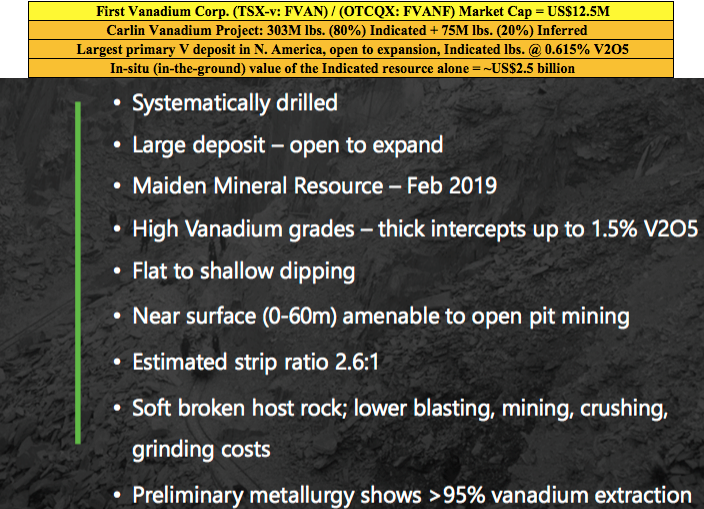

First Vanadium Corp. (TSX-V: FVAN) / (OTCQX: FVANF) has been under pressure, along with hundreds of battery metal juniors and the underlying metals including vanadium, cobalt, lithium. Even vanadium giant Largo Resources is down 61% from its 52-week high. Yet, if one believes in vanadium, it’s hard to ignore First Vanadium’s shares at C$0.44, down 78%! The pro forma Enterprise Value [market cap + debt – cash] is just US$12.8M. The Company has C$1.9M in cash.

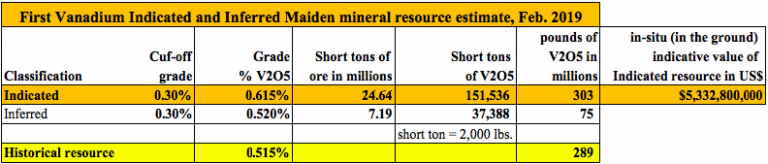

Yet, even at current vanadium pentoxide (“V2O5“) prices, the in-situ value of the Indicated-only portion (303 million pounds) of the Company’s estimated resource is ~US$2.5 billion. Management believes it has the largest high-grade primary vanadium resource in North America.

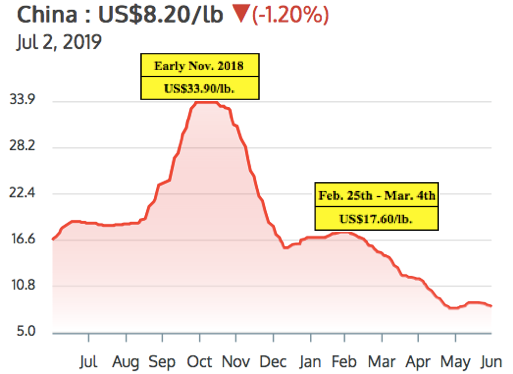

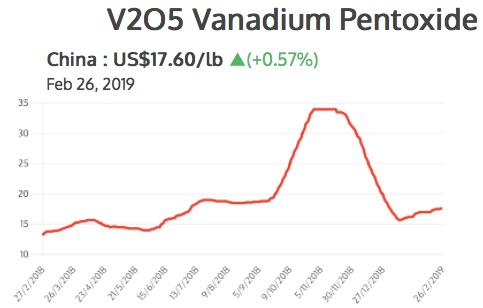

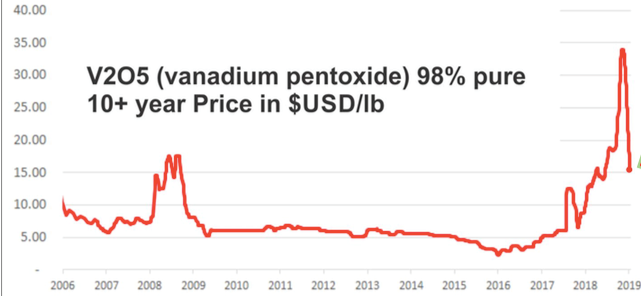

There has been a lot of weeping and gnashing of teeth over the V2O5 (China) price falling from a 2019 high of US$17.6 to its current US$8.2 per pound. But, as the saying goes, the cure to low prices is…. low prices. Few new projects make sense at today’s levels. I believe that V2O5 (China) between US$10-US$15 per pound might be a sweet spot, good for both producers and end users.

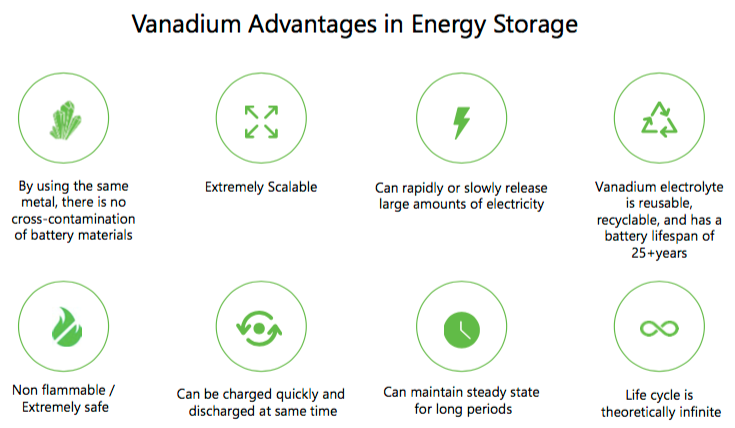

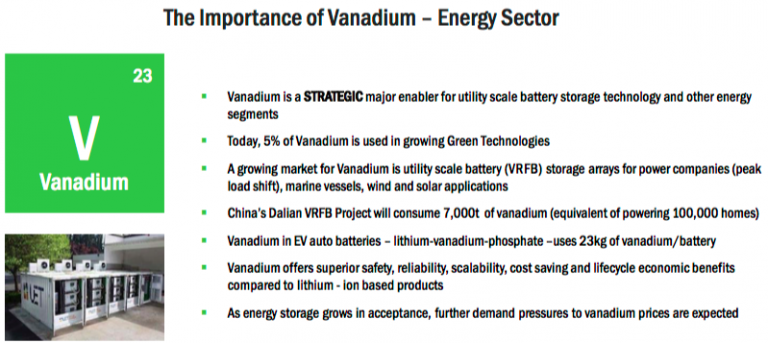

Steel companies can afford to pay higher prices for V2O5, but grid-scale, Vanadium Redox Flow Battery (“VRBs“) Energy Storage Systems (outside of China) might need prices below US$10/lb. to go mainstream. Importantly though, VRB plant costs are coming down. Vincent Sprenkle, a lead researcher at the U.S. Department of Energy’s Pacific Northwest National Laboratory, (“PNNL“) recently said, “VRB costs could be lowered by another 50%.” That would be very bullish for vanadium prices, it would allow for widespread adoption of VRBs even with V2O5 prices above US$10/lb.

First Vanadium has a sizable resource, a good grade, in a great jurisdiction. A Preliminary Economic Assessment (“PEA”) is expected by year end. The following interview of Paul Cowley, P.Geo., President, CEO & Director of First Vanadium, was conducted by phone & email between June 24th & July 2nd.

Please tell us about yourself and your team.

I’m an exploration geologist with 40 years’ experience in the discovery & evaluation of mineral deposits around the world. About half of my career was with a Major, BHP Minerals. I was involved in leading the team in the Canadian arctic that made 4 gold deposit discoveries that generated about 6 million ounces of gold. I also worked at Escondida and BHP’s Ekati diamond mine during their exploration days.

I’m a senior guy, but I’m the youngest of our group. The others have even more years of experience. We have two mining engineers that held mine general manager positions of very significant mines at Majors. We have four metallurgists that have worked for Majors, in senior roles. We have a construction engineer who’s built 20 mines in North & South America, he’s currently building Lundin’s mine in Ecuador.

What do you make of the recent volatility in the vanadium price?

Since early March 2019 the vanadium price has taken an unexpected turn lower. Prices are not responding to the bigger picture demand and supply imbalance. Chinese steel plants did not recharge their vanadium inventories in this period, as many expected they would, putting pressure on traders to liquidate at undercutting prices, but they will have to restock. The U.S.-China trade wars, and some shortfall of enforcement of new Chinese rebar standards, appear to have exacerbated the situation in the short term.

It’s our view that the fundamentals of demand in global steel applications will outstrip supply and should push vanadium prices higher again in the second half of the year, and beyond. Adding to the demand side is the exciting boom in solar & wind projects, all of which require battery storage. This is happening on so many levels around the world that we expect to see the vanadium battery carve out a healthy market share in this expanding renewable space. Some are calling the 2020’s, the Solar Decade.

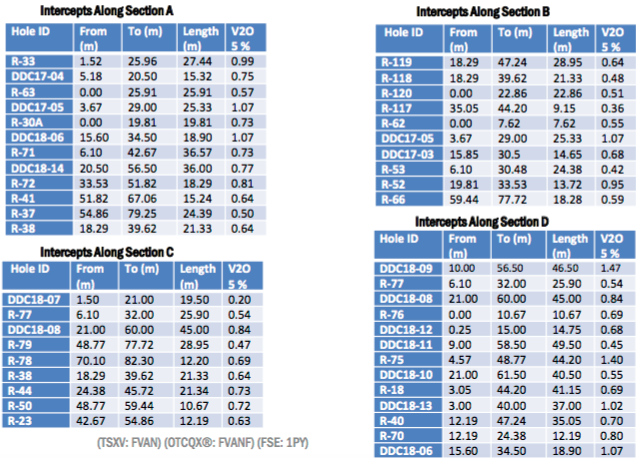

Please explain the significance of the historical data you recently received, that extended the strike length by 300 meters to the south.

It means more potential than we had expected. From our drilling, the deposit appears to be open to expansion in several areas, but we did not expect the deposit to be open to the south. The newly acquired data demonstrates a 15% strike length increase to the south and it’s still open in that direction. This is exciting news as this data was not included in the resource estimate we put out in February.

You already have a 303 million pound vanadium resource (in-situ value of ~US$2.5 billion) in the Indicated category alone. Does the resource need to get any bigger?

That’s a good question. But it needs to be answered through an economic study. In our view, the resource is sizable. It’s currently the largest, highest-grade primary vanadium resource in North America. Our immediate priority is to demonstrate potential economic viability with what we have, knowing that we believe we could always make it bigger if and when we need to.

Several readers may assume that First Vanadium will need an expensive roaster in its operating flow sheet. What are your latest thoughts?

Not true. The path we are on with our metallurgical flow sheet does not include, or require, a roaster.

Although Nevada is the #1 global mining jurisdiction in the latest Fraser Institute Mining Survey, some complain that it takes a long time to get permits. What does your team expect in this regard?

In general, in the U.S. that is true, but not in Nevada. Nevada has a responsible review and process, but it’s a mining state. And, even more so for us now that vanadium is on the critical minerals list. The U.S. has unveiled its strategy in an effort to rebuild struggling domestic supply chains for metals & minerals it deems “critical” to the country’s manufacturing & defense sectors. Recently this was reiterated when President Trump & Prime Minister Trudeau announced a plan for the U.S. & Canada to collaborate on critical minerals.

What are the latest developments on the metallurgical front?

We continue to make strides on the metallurgical front. In April we announced an average of 95% vanadium extraction from the rock across the deposit, into solution. We do not know what ultimate recoveries will look like just yet, but we are making good progress. And, we’re making strides in the area of pre-concentration, with the aim to reduce the plant size, which would lower the capital intensity of the project.

What are First Vanadium’s plans for a Preliminary Economic Assessment (“PEA”)? Might that be a 1H 2020 event?

No, we think that we can move faster, our aim is to initiate a PEA in the 3rd quarter, with results to be reported before the end of the year.

Why should readers consider buying shares of First Vanadium?

I see very good value and upside; an exceptional senior technical team, a good share structure and a great project. We now have C$1.9 million in cash with the recent private placement closing, and 42.4 million shares. Our share price now is where it was at the beginning of 2018! Yet, we have delivered two successful drill campaigns, a mineral resource with considerably higher grades, and more metal in the ground than our historical resource, and 80% (303 million pounds) of it is in the Indicated category.

That, plus positive metallurgical test work and environmental baseline studies to advance permitting. If one is bullish on the vanadium price, currently at US$8.20/lb., then First Vanadium’s (TSX-V: FVAN) / (OTCQX: FVANF) project in the #1 of 84 ranked global jurisdiction of Nevada should be high on the list of projects to consider investing in.

Thank you Paul, very interesting and timely commentary on the vanadium market and on First Vanadium. I look forward to seeing a PEA later this year!

Peter Epstein

Epstein Research

July 9, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Vanadium Corp., including, but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Vanadium Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of First Vanadium Corp. and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

First Vanadium (TSX-V: FVAN) is one of the better known vanadium companies. Its CEO, Paul Cowley, can be seen in a number of video clips that I linked to at the bottom of the page. Despite being a blue chip name, First Vanadium’s market cap is just US$19.5 M. This, for a company that claims to have the highest-grade primary vanadium project in North America, and a plan to fast-track its flagship project in Nevada. To top it all off, management just released a summary of their Maiden mineral resource estimate.

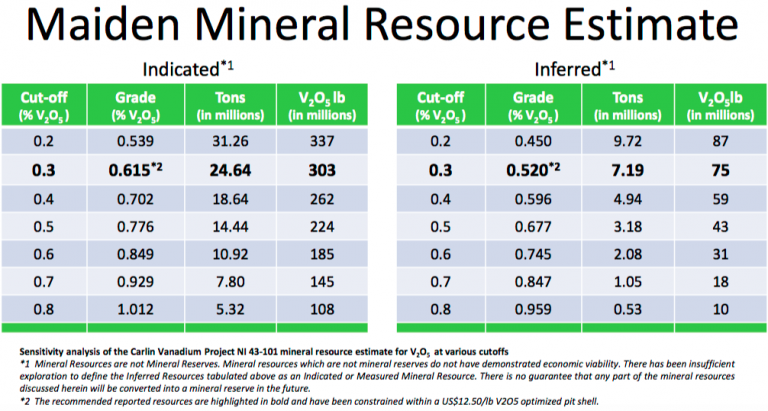

The Maiden mineral resource estimate came in at 303 M Indicated pounds @ 0.615% & 75 M Inferred pounds @ 0.52%. That represents a moderate increase in size & grade from the historical resource estimate of 289 M Inferred pounds @ 0.515%. Importantly, 80% of the new resource (in pounds) is in the Indicated category. At the current vanadium pentoxide price of US$17.60/lb., the in-situ value of First Vanadium’s 303 M Indicated pounds alone = US$ 5.33 billion. That’s about 275x its market cap. Note: {in-situ values can be misleading for early-stage projects, but they can be compared to peers at similar stage}.

Is vanadium for real? Will Vanadium Redox Flow Batteries cause demand & prices of vanadium pentoxide (“V2O5“) to soar? Will global infrastructure projects demand greatly increased amounts of vanadium-strengthened steel rebar? Please continue reading for answers to these and many other important questions. Note: Peter Epstein and Epstein Research have no prior or existing relationship with CEO Paul Cowley or First Vanadium Corp.

Please give readers the latest snapshot of First Vanadium.

First Vanadium Corp. is focused on vanadium and its advanced-stage Carlin Vanadium project in Nevada, the largest and highest grade primary vanadium deposit in North America. The Company is run by professional geologists & engineers who have worked for Major mining companies in senior positions in exploration, deposit discovery, construction & mining operations.

The company has a tight share structure and is well-funded. We just released a Maiden mineral resource estimate that’s 80% in the Indicated category and that’s larger than our historical resource, which was 100% Inferred. We are very pleased with these results.

Why vanadium, why not lithium, cobalt, graphite, nickel or copper?

All of these minerals are going to be winners in the near future with the inevitable rapid demand increases for these metals with the commercialization of lithium-ion electric batteries in automobiles and vanadium redox flow batteries in large power storage applications. There is just not enough production of these minerals from existing mines to meet the projected demand of this exciting evolution in Battery Technology and commercialization.

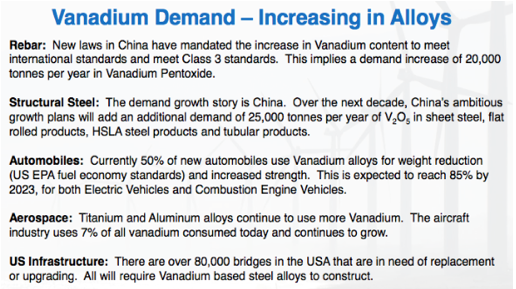

In addition, in the case of vanadium, it is chiefly used as an alloy for strengthening steel in infrastructure; rebar, pipelines, airplanes and car frames. CIBC Mellon has estimated that there will be $35 trillion dollars of global infrastructure projects starting over the next 20 years, which will spark big demand for vanadium.

Tell us more about the Carlin Vanadium project.

The Carlin Vanadium project is a black shale-hosted sedimentary bed of high-grade vanadium which is shallow dipping and near-surface, making it ideal for open pit mining. The project’s superior location and infrastructure are added benefits, being located less than 6 miles by road to a major rail hub, a major highway, power and mining community.

Furthermore, the grades are higher, about double that of other Nevada based vanadium projects, and there’s significantly more vanadium metal in our deposit, also about double that of our peers. Our Maiden mineral resource estimate shows the large scale and high grade of the deposit.

How significant has First Vanadium’s exploration drilling been compared to historical drilling? How many new holes were drilled?

The two drill campaigns that First Vanadium did in 2018 totaling 89 holes were extremely strategic and successful in both in-filling and expanding the deposit. We frequently received assay values with higher grades than those found in the older drill data. This is reflected in our Maiden mineral resource estimate that shows a 0.615% grade in the Indicated category alone. The infill drilling improved the confidence level to justify a high percentage of the resource being in the Indicated category.

Please explain First Vanadium’s fast-track approach at the Carlin project.

In the 15 months we have had the project, we quickly received permits to drill, conducted two drill campaigns, made significant inroads in metallurgy, conducted environmental studies, and delivered a significant Maiden mineral resource estimate, with 80% of the vanadium in the Indicated category, all to advance the project and unlock value for shareholders. These steps are the normal steps taken by companies to advance and de-risk projects, but normally it would take 3-4 years to accomplish what we have done in 15 months.

Is there too much talk about VRBs, which only represent 1%-2% of vanadium use? Is the VRB opportunity possibly overrated?

The Vanadium Redox Flow Battery has only just started to be commercialized over the last two years and currently draws a small percentage of global vanadium consumption. It will ramp up in the short and intermediate time frame to become a much more significant part of vanadium consumption. For example, one project alone in China, the Dalian project, is expected to consume 7,000 tonnes of vanadium, ~8% of annual production, the equivalent of powering 100,000 homes. You can see that the scaling opportunity is eye-opening.

The VRB battery is a superior battery for storing large amounts of electricity and they are forecast to last 25 years, whereas the equivalent lithium-ion battery needs to be replaced every 3 to 5 years due to its depleting characteristics. The VRB battery is the ideal battery solution for the green energy space for large-capacity electricity storage in power grids and in wind & solar applications. Some have stated that if vanadium prices are too high, the VRB battery will not be completive, but continuing technical advancements are being made to bring costs down. Some vanadium producers are offering to lease the vanadium in the battery to reduce costs to the end user.

What do you make of the sharp decline in vanadium prices in Q4 2018?

Vanadium was the best performing metal in 2018, despite the pull-back at the end of the year. September & October 2018 saw a rapid increase in vanadium prices leading up to the implementation of the announced November 1st, 2018 Chinese law requiring 30% more vanadium in Chinese rebar. Rapid price increases are normally followed by pull-backs as a normal reactionary correction, but eventually that pull-back over-reaction needed to stabilize and reflect more prevailing supply & demand factors.

Naturally, the reason for the run-up in price is real and is expected to add more demand to the stage. The strong demand for the metal, and the tight supply, are still the norm– forcing prices up. From mid-January to late-February, the Chinese price of vanadium pentoxide is up 12.8% from US$15.60 to US$17.60/lb. (see chart below from vanadiumprice.com). We expect 2019 will be another strong year for vanadium prices.

What’s the biggest risk to the Carlin project in the next 12 months?

Perceptions. In the valuations of vanadium projects and their in-situ assets, and in vanadium price performance and trajectory through 2019 to provide the investor with confidence and interest in the future of this metal.

Thank you Paul, that was very helpful, I think that readers should have a much better understanding of First Vanadium after reading this interview. Congratulations on your Maiden mineral resource estimate, and continued good luck on fast-tracking the Carlin Vanadium project.

Peter Epstein

March 1, 2019

Video clips of CEO Paul Cowley and/or First Vanadium Corp.

https://www.youtube.com/watch?v=SEsx6wPCQiM&t=9s

https://www.youtube.com/watch?v=THrnsK_ODwU&t=97s

https://www.youtube.com/watch?v=mdx-TFega1Q

Delrey Metals Corp.’s (CSE:DLRY, FSE:1OZ) mandate is to create shareholder value by sourcing, financing & developing undervalued strategic energy metals properties & projects through staking ground or making accretive, prudently and creatively financed acquisitions & joint ventures / farm-ins. They’re off to a good start and have a clean balance sheet with just 34 million shares outstanding and cash of ~C$ 1.5 million. The market cap is about C$8 M = US$6.1 M. The Company is aggressively pursuing additional strategic energy metals assets, and have honed in on 2 or 3 in particular.

Delrey Metals has acquired 5 highly prospective properties in Canada. 4 are prospective for vanadium, for a total of 9,482 hectares, and 1 is a cobalt–copper-zinc opportunity that Cobalt 27 Capital Corp. acquired a 2% NSR on. All 4 vanadium assets will be receiving airborne magnetic surveys and geophysics in February. Subject to results, management will determine which properties to focus on. Both the Porcher and Blackie properties have unique features that if confirmed, will likely make them top priority targets for the next phase of exploration.

Early Days for the Canadian Vanadium Opportunity

Interest in vanadium has grown along with the price. Demand from China continues to be the key driver. While the rest of the world grows at 2%-3% per year, a bad year for China is +6%, and its the 2nd largest economy on the planet. Not only does China use a tremendous amount of steel, it uses huge quantities or rebar which is used in construction & infrastructure building (and rebuilding).

Regarding vanadium pentoxide pricing, there’s been a lot of angst over the recent dramatic decline, but Chinese prices seem to be settling in around US$17/lb. The chart above shows a price closer to US$15/lb., but the price was US$16.90/lb. as of February 3rd. It topped out at nearly US$35/lb. in November, so the price has been halved from a 13-yr. high. Importantly, US$17/lb. is still a strong price, up from a low of US$2.35/lb. on 12/31/15. From $2.35/lb., the Chinese vanadium pentoxide price has risen at a 3-yr CAGR of ~93%. A price between US$15-US$25 is a sweet spot, too high a price and VRBs get priced out of the market.

Perfect Storm of Demand & Supply Fundamentals

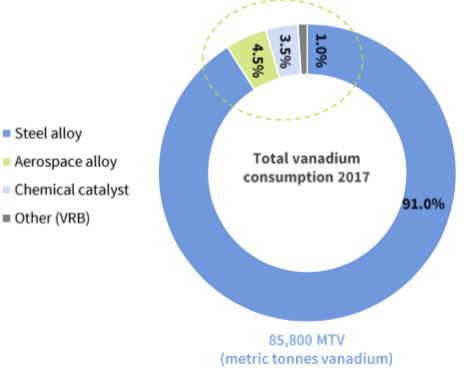

Vanadium is primarily used (91%) to strengthen steel rebar, (2 pounds of vanadium added to a tonne of steel doubles its strength), last year China came out with new regulations for Chinese rebar makers– use more vanadium! However, reportedly, 30%-40% of Chinese rebar producers did not follow the regulation implemented in November, which was likely a big factor in the vanadium price crash. The increased demand from this initiative alone is estimated at 10,000 tonnes per year. That’s on a global market of about 90,000 tonnes. 10,000 tonnes/yr. is what Largo Resources’ main mine in Brazil produces, one of the largest mines in the world.

Global demand for vanadium is also being enhanced by other internal moves in China, most notably a total ban on the import of slag and scrap (waste products) that contain vanadium. These waste streams had been used as feedstock for vanadium producers in China. The ban is expected to reduce domestic Chinese production by ~5,000 tonnes/yr.

Quickly on the supply side there have been mine closures dating back to 2015 that are impacting the market. In 2015 a major Brazilian company liquidated, closing the Evraz Highveld mine, representing 10%-15% of global vanadium production. However, at the time the inventory of vanadium was high, so there was a limited price reaction.

Fast forward 2-3 years, there have been other smaller mine closures in China & Brazil, and the above mentioned increase in demand, causing vanadium inventory to be drawn down substantially. Therefore, both sustained demand drivers and ongoing supply constraints help explain the price move from $2.35/lb. at the end of 2015 to a peak of nearly US$35/lb. in 4th qtr. 2018.

Vanadium Reflux Flow Batteries Could use 31k tonnes of V2O5 by 2025

And then there’s Vanadium Reflux Flow Batteries (“VRBs“). They represent just ~1.5% of the global vanadium market, but some pundits have large, grid-scale energy storage growing at a CAGR of up to 40%. Roskill forecasts vanadium use in VRBs to be 31,000 tonnes by 2025. If true, VRB’s would be a significant demand driver, easily overtaking the uses in Aerospace & chemical catalysts combined.

2019 could be a sweet spot in vanadium pricing, several experts expect prices in the US$15/lb. to US$25/lb. range. That would sustain bullish sentiment for companies with properties outside of China, Russia & South Africa. Delrey Metals has exactly that, 5 early-stage prospects in Canada, all with decent infrastructure, all situated on past producing mining or logging sites, and most important, all having had historical work. Prior work included magnetic and other surveys, soil sampling, surface samples, concentrates were made from some samples, and a drill program (at the Star property).

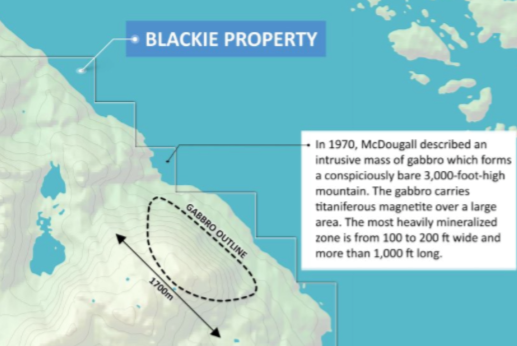

Blackie Vanadium Property

The Blackie Vanadium property is in west-central British Columbia,, ~96 km south-southwest from Prince Rupert. The property is on Banks Island and is accessible year-round. It is located on tidewater, accessible to the Prince Rupert deep water port, which allows for an 8 day trip to North American west coast ports. There’s a network of logging roads (<500 meters away) allowing for low-cost exploration & development.

The property consists of 5 tenures covering 1,213 Hectares, open for expansion in multiple directions. Blackie is on a brownfield site, the Yellow Giant underground mine was operational as recently as 2015. Blackie is host to a gabbroic body 1.2 km by 0.4 km, with an estimated thickness of at least 500 m (McDougall, 1985).

Assays from samples collected by McDougall (1984) ranged from 20% to 25% Iron, 1.1% to 1.9% Titanium, and up to 0.33% V (0.59% V205). Concentrate results made from these samples returned 0.5% to 1% V (0.89% to 1.78% V205). Individual outcrop results from a previous operator returned up to 49% Iron, 7.0% Titanium and an extremely anomalous 1.2% V (2.14% V2O5). “Several million tons of Iron-Titanium-Vanadium bearing material are known at this locality” 1(Rose and Mulligan, 1970).

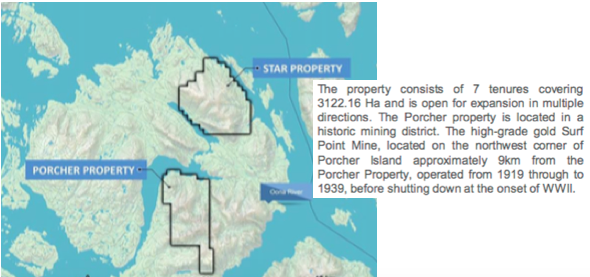

The Porcher property

The Porcher property is located in west-central BC, ~38 km south-southwest from Prince Rupert. The property is located on Porcher Island and is accessible year-round. There’s a network of nearby logging roads, allowing for cost-effective exploration & development.

Porcher consists of 7 tenures covering 3,122 Hectares, open for expansion in multiple directions. The property is located in a past-producing mining district. The Surf Point Mine, located ~9 km from the Porcher property, operated from 1919 through to 1939. Like with the Blackie property, Porcher is located on tidewater, less than 39 km from Prince Rupert’s deep water port.

Porcher is host to 2 gabbroic dykes hosting iron-titanium-vanadium mineralization. These sizable dykes are 5.2 km x 1 km, and 4 km x 0.6 km. The dykes are coincident with a large magnetic anomaly identified in the Canada 200 m Residual Total Magnetic field dataset. Limited sampling by McDougall (1961) was completed, with concentrate results ranging from 0.3% to 1.5% Titanium and 0.2% to 0.5% V (0.34% to 0.84% V205). V2O5 deposits globally range from about 0.3% to 0.7%.

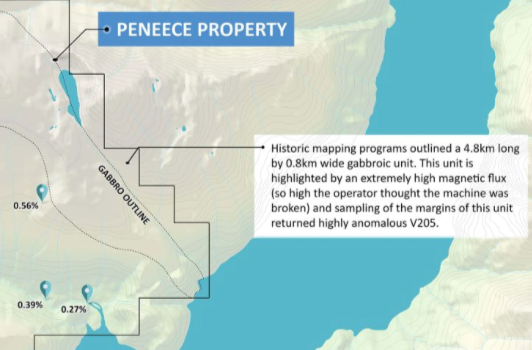

Peneece Vanadium Property

The Peneece Vanadium property is in southwest BC, a narrow coastal mainland fjord 85 km east of Vancouver Island. The property consists of 5 tenures covering 1,500 Hectares, open for expansion in multiple directions. Peneece is located along tidewater and is accessible year-round. There’s a network of logging roads within the center of the project area.

The property is host to a >4.8 km long by 0.8 km wide (open to the northwest) pyritic gabbroic complex associated with a very large and intense magnetic anomaly which is believed to be caused by a large body of vanadium-bearing massive titaniferous magnetite.

Access problems prevented sampling of the highly magnetic core, and only marginal material samples were obtained. Concentrate results from these samples graded 0.16% to 0.33% V (0.29% to 0.59% V205 – AR 12204) and up to 6.5g/t Ag, a precious metal not typically found in these systems.

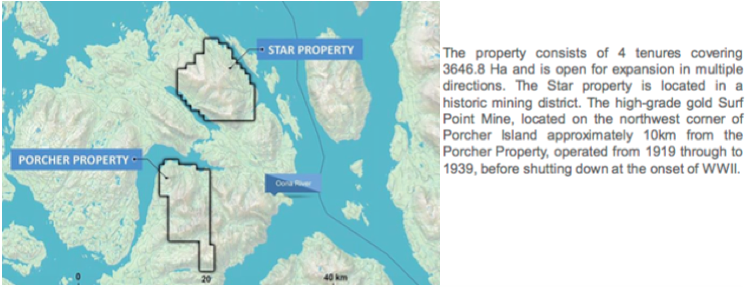

The Star Property

The Star property is located in west-central BC, ~ 27 km south-southwest from Prince Rupert. Like the Porcher property, Star is situated on Porcher Island and is accessible year-round. There’s a network of logging roads covering the majority of the property.

Star consists of 4 tenures covering 3,647 Hectares, open for expansion in multiple directions. The Star property is in the same historic mining district as the Porcher property. A gold mine operated from 1919 to 1939. It is located 10 km from the Star property.

The eastern part of the property was explored and drilled in 1955 for Iron Ore by One Resources Canada Corp. Twelve short (<50 m) diamond drill holes were completed for a total of 696 m, targeting a small magnetic anomaly. Conclusions from this work program were that ‘at least several hundred thousand tonnes of magnetite-bearing rock with a grade of the order of 35% Iron exist within the drilling area’ (PF671671).

The One Resources Canada Corp. 200m Residual Total Magnetic field dataset highlights a large 5 km x 7 km magnetic high located in the center of the Star claim group. Historic drilling indicated a much larger resource potentially exists within the property area to the west. While the historic drill program did not analyze the magnetite for Vanadium, a Regional Geochemical Survey (RGS) was completed by the British Columbia Geological Survey in 2000 over the Star claim group, which highlighted up to 148 ppm vanadium-in-silt (99th percentile) and 5.06% Iron.

Management believes the Star property has the makings of a significant vanadium discovery including a large magnetic (5km x 7km) high, drained by extremely anomalous vanadium-in-stream results, with a several hundred-thousand-tonne magnetite resource on the margin.

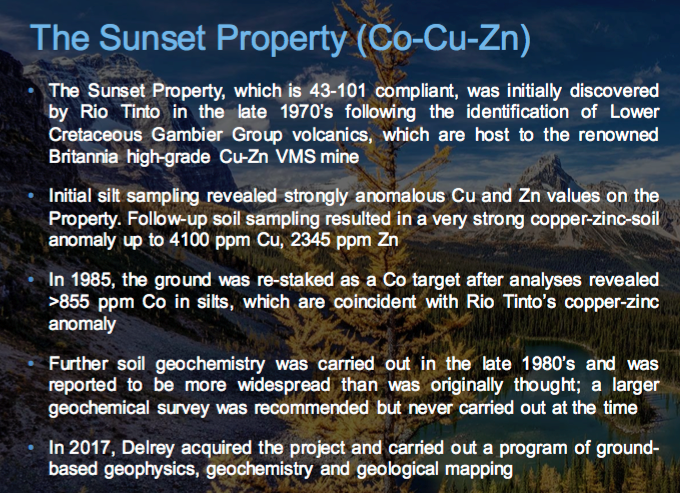

The Sunset Property

The Sunset Property consists of 4 mineral titles covering 785 Hectares. The area had exploration work done in the 1970’s-1980’s. Several cobalt-copper-zinc soil geochemistry anomalies were discovered. In 1987, Decade International outlined a large cobalt‐copper‐zinc anomaly.

A recent exploration program consisting of mapping, grid preparation, geochemical soil sampling & magnetometer surveys has been done, validating the previous cobalt‐copper-zinc soil geochemical anomaly. Copper values in soil over 500 ppm, when plotted with historical values, indicate a cluster about 1,000 meters by 500 meters. Numerous anomalous Cobalt values lie within this area and a smaller cluster of anomalous zinc in soil is also present.

The presence of elevated levels of Cobalt is interesting, and a 2% NSR royalty on Cobalt only has been sold to Cobalt 27 Capital Corp.

Delrey Metals recently finished a phase one exploration program at Sunset. In September 2018, the Company collected 708 soil samples, 68 rock samples and 11 stream sediment samples. As a result of the sampling, management extended its cobalt-copper-zinc anomaly about a kilometre to the west, and discovered a new zone, called Roughrider, which graded up to 4.3% copper. Management believes the new zone may indicate a cobalt-copper-zinc VMS-style of mineralization.

With these 5 properties, investors have multiple opportunities to win if management advances any of the properties to a maiden resource or to a PEA. If one believes in the fundamentals of Vanadium, Canada is a great place to be looking for potentially economic deposits. In addition, management is actively looking at other attractive properties to acquire or option. 2019 is shaping up to be a busy and productive year for Delrey Metals (CSE:DLRY, FSE:1OZ).

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Delrey Metals, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing co-ntained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Delrey Metals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Delrey Metals was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic. [ER] may buy or sell shares in Delrey Metals and other advertising companies at any time.

Earlier this year on March 11th, while the price of uranium was making a resurgence, Japan experienced the worst earthquake disaster in its modern history. The earthquake, a 9.0 on the richter scale, was followed by a deadly tsunami that resulted in near complete destruction of the infrastructure in northern parts of Japan and served a serious blow to the uranium market.

With tax-loss selling in full effect and the equity markets experiencing extreme volatility as the end of 2011 draws near, we connected with Stewart Wallis of Crosshair Energy for an exclusive interview to find out what’s in store for the company in 2012.

Crosshair is a diversified mining and exploration company focused on uranium, vanadium and gold. After a difficult 2011 for the uranium sector, what is on the horizon in 2012 for your uranium projects?

In 2012 we will be focusing on our Wyoming uranium projects, Bootheel and Juniper Ridge. Both projects will have 43-101 resource updates released early in January, followed by scoping studies to be completed in the first quarter. Based on these reports, the 2012 programs will focus on permitting and additional drilling designed to aggressively advance these projects towards development.

Your Canadian uranium projects are located in the CMB Labrador and Crosshair spent $3.8 million on drilling in 2011 – what is the timeline for updating the company’s uranium resource estimates?

Crosshair maintains multiple and expandable uranium resources in Labrador. 2011 drill programs were conducted on both the CMB Uranium/Vanadium Project and the CMB Joint Venture Project, with a goal of increasing the uranium and vanadium resources as well as testing new targets outlined from earlier exploration programs. We anticipate updated resource estimates in 2012 on the CMB C-Zone/Armstrong corridor and the Joint Venture Two Time Zone.

How important is vanadium to the economics of the company’s CMB uranium/vanadium project?

We have not completed a scoping study on the CMB project so we cannot predict the actual cash benefit of the vanadium as a by-product. However, the vanadium mineralization occurs in the hanging wall of any open pit which might be developed on the uranium mineralization and we do know that the vanadium recoveries range from 13.4% to 93.6% based on our metallurgical test work in 2010. Typical recoveries range between 45-85%, and based on our metallurgical test reports a reasonable vanadium recovery of 85% was selected in our resource estimate.

Comparatively speaking there are quite a few uranium companies that are trading at or near 52 week lows – in your opinion, is the market effectively “throwing the baby out with the bath water” at these valuations?

Since Fukushima, all uranium companies are trading at approximately 60% of their pre Fukushima values. Once the world realizes that there are no other “green” options for base load power, the valuations of uranium explorers and developers should increase.

CXX has been trading at a discount to its peers since the Labrador Mining Moratorium was announced in April 2008. One could expect that our share price should improve when this Moratorium is removed. The INUIT government is reviewing the lifting of the Moratorium and a vote is expected to be held on or about the week of December 12th, 2011.

With Rio Tinto’s proposed acquisition of Hathor Exploration many people are wondering what’s next for the uranium sector. Is M&A something the management team is considering at this juncture?

Crosshair is constantly looking at both property and company acquisitions. Earlier this year we announced that we were looking at acquiring the US assets of AusAmerican Mining, an Australian Company. Upon completion of our due diligence and based on the current market situation we declined to proceed with the transaction. That being said we continue to evaluate other situations in the uranium sector.

Your Gold project is located in the Newfoundland and Crosshair completed a Bulk Sample in late 2010 – what is the status of this project?

The company has spent approximately $1.9 million since April 2008 on its 60% owned Golden Promise Property in central Newfoundland. This Joint Venture project with Paragon Minerals contains a NI 43-101 Inferred Resource of approximately 89,500 ounces contained in 921,000 tonnes at a grade of 3.02g/t that is open and expandable. Our 2,174 tonne Bulk Sample, done with a goal of better determining grade and recoverability rates, produced approximately $430,000 in gold and silver earlier this year.

Crosshair recently completed a name change from Crosshair Exploration to Crosshair Energy – is it safe to assume that, at some point, you intend to spin-out your gold project to focus on energy?

Crosshair is currently evaluating its strategic options for its gold assets and these options may include a sale, spin-out or option agreement.

President Obama likes vanadium; or rather, he likes to say the word vanadium. Last February Obama joked that “Vanadium redox fuel cells is one of the coolest things I’ve ever said out loud“. Obama also said this “next generation energy storage system will help families and businesses cut down on energy waste, save money and reduce dangerous carbon emissions”. So what is vanadium and, more importantly, what is a vanadium redox fuel cell?

Vanadium is the 23 element on the periodic table and is a soft silver-grey ductile transition metal. It is primarily produced in Russia and China from steel smelter slag and in a few other countries around the world as a flue dust of heavy oil or a byproduct of uranium mining. Most vanadium, approximately 85%, is used as an alloy called ferrovanadium as an additive to improve steels. But recently its vanadium’s status as a strategic metal and its green energy applications that have people, including President Obama, talking. Although, the more correct terminology is the vanadium redox flow battery.

Vanadium redox flow batteries are distinguished from fuel cells by the fact that the chemical reaction involved is reversible meaning that they can be recharged without replacing the electroactive material. Also, an important factor in the redox flow battery is that the power and energy density of the batteries are independent of each other in contrast to rechargeable secondary batteries which avoids cross contamination. These special characteristics make the vanadium redox flow battery uniquely applicable for energy storage applications including transportation and utilities.

Although vanadium has only recently been grabbing media headlines, one TSX-V listed company decided to pursue vanadium as an emerging opportunity when they fortuitously discovered the critical element in Nevada while drilling for base metals back in November, 2007. That company was American Vanadium which, at the time, was operating as Rocky Mountain Resources.

American Vanadium recently reported they are on track at the Gibellini vanadium project in Nevada to delivery of Feasibility Study in Q3, 2011 and is looking to start of production by 2013. This will position the company to have the only vanadium mine in the US, which is by some accounts, an enviable position.

Chris Barry, an analyst at House Mountain Partners, notes in a recent report, “With its low-cost project economics, AVC presents a unique opportunity to join the ranks of vanadium producers and contribute to the growing demand for this little-known metal. This is where we think AVC can create value for shareholders, near-term production of a strategic metal in a stable geopolitical jurisdiction.” Mr. Barry went on to say that, “Vanadium is most exciting because there is an increasing potential demand for the metal in the energy storage and battery spaces.”

MiningFeeds.com interviewed Bill Radvak, President & CEO of American Vanadium, to get to the bottom of vanadium and to find out what’s in store for the company.

Vanadium is certainly not a house-hold name, please tell our readers about vanadium, its uses and why you were attracted to this particular transition metal.

I volunteered for this job eighteen months ago because it is was perfect mix for me as a start-up where I could use my education and experience as a mining engineer and also leverage my fifteen year stint in the technology industry. And that is what the American Vanadium opportunity is about: an advanced vanadium resource which truly gives us the capability to lead the creation of the mass storage industry in the US using vanadium flow batteries.

The street knowledge of Vanadium has jumped tremendously in the time I have been with AVC and that is only going to continue to increase due to its growing importance and new critical uses that will affect everyday life. Historically, vanadium is all about being a premiere steel strengthener which was first used in the Model T Ford and since then has become increasingly critical to the steel industry. A great example is that on July 1 of this year, China implemented a new regulation for their rebar grade that will result in an additional 27,000 Metric tons of Vanadium consumed in China which is a 40% increase in global vanadium consumption in the next few years. As well, Vanadium is absolutely critical and irreplaceable in the production of titanium alloys for aircraft and the defense industry, catalytic converters and important chemical production.

A great statement we heard recently from the US Department of Energy was “the electric grid is the world’s largest supply chain without a warehouse”. Their biggest urgency is to build these “warehouses” and the most advanced mass storage battery technology is the vanadium flow battery. Essentially these are massive vats of vanadium in sulphuric acid that allow the continual storing and discharging of electrical energy. The key is that these vanadium flow batteries are scalable to meet any needs and will last for decades and that is why there is a huge effort to commercialize these batteries worldwide.

Vanadium is on the Critical Element list in America, how might this help shape American Vanadium?

Given that the US government has recognized it is in a terrible spot trying to secure supplies of rare earth metals, it taking a very serious look at all their supply chains. We have helped them further recognize that the US only domestically produces 5% of its raw vanadium needs as a by-product of a uranium mine while 80% of its needs are met by the Venezuela, China, Russia and South Africa. One hundred percent of the supply for the vanadium flow battery industry will come from these same countries. And 100% of the vanadium required for their titanium alloys used in the aircraft and defense industries comes from a single source in Russia.

When key industries and national defense rely on a critical element primarily from Venezuela, China, Russian and South Africa, the US has to look for domestic supply. And there is no other domestic US option on the table or being considered other than American Vanadium. As we are driving fast on our timetable to begin production by the end of 2012, we are being taken seriously by the US Government agencies as the key domestic source of vanadium for current and future needs. Importantly, this gives us tremendous leverage in partnering with vanadium flow battery companies as anyone seriously wanting to capitalize on the huge need in the US logically has to have access to our production which could easily be turned 100% to meet this premium need.

Please tell us a bit about the background of the company and, specifically, some background on your flag-ship Gibellini project in Nevada?

American Vanadium was built around the Gibellini Project which was historically drilled up by Union Carbide, Noranda and Atlas mining. What has made this project economic is we have recognized that the unique geology enables us to use simple and cost-effective heap leach processing to extract the vanadium. Being located in the middle of Nevada, the unique sedimentary hosted deposit is essentially a ridge of exposed, heavily oxidized, crumbled rock with a strip ratio of a remarkable 0.2.

A Scoping Study was completed by AMEC in 2008 and the operation they designed had an after tax IRR of 40% with a capital cost of less than $100 million. AMEC has been engaged to complete a Feasibility Study and we expect this to be delivered in this quarter.

The Gibellini project has a defined 43-101 resources estimate of 122 million pounds of indicated vanadium (i.e., vanadium pentoxide or V205) grading at 0.339%, where does this put American Vanadium in terms of size and grade of other known deposits?

At 3 million tons per year mined, our mining project could be considered small relative in the mining industry, but this production rate would represent about 50% of the United States annual vanadium demand or about 5% of the world supply this year. This makes our operation very important to the vanadium industry, particularly the US consumers. We are fortunate that we are in a very friendly mining jurisdiction where we can control costs on an already inexpensive mining and processing operation. Therefore, while our grade is relative low, we expect it to be very economic as most other mines have a magnetite that requires stages of crushing, grinding, magnetic separation and roasting.

We also have a very expandable resource potential. We focused on getting to production base on the historic drilling on the main occurrence. Now that the Feasibility Study on this occurrence is nearing completion, we are turning our immediate attention on building the resource on expanding this main occurrence and upgrading the already drilled Louie Hill that is adjacent to the Gibellini. After that there are a handful of other occurrences on the property we will be exploring as well as looking regionally.

What does the end-user market look like for Vanadium and how is Vanadium sold into that market?

The vanadium market has been in a state of oversupply for the past decade and is now transitioning into an extended period of undersupply; coincidentally, this is anticipated around the time we expect to reach production. This bodes well for the producers as the price of vanadium is forecast to climb for the next 5 – 10 years. And this does not take into account any demand at all from the vanadium redox battery so obviously we are thrilled with market timing and the vanadium outlook.

The consumers are now becoming worried about surety of supply. Our priority, while the vanadium flow battery market grows, is to pursue the US consumers beginning with the handful of steel companies that rely on foreign sources. We can offer a longer term, domestic supply to satisfy their surety of supply concerns. Additionally, we will be focussing on the titanium market where vanadium sells for a premium. While on a global scale only 4% of world vanadium is consumed in titanium alloys, in the US almost 20% of the vanadium is consumed in titanium alloys due to the significant aircraft and defense industries which rely on a sole source of vanadium from Russia.

What milestones do you hope to reach before the end of 2011?

We have a number of very important milestones we expect to deliver in the coming months including the completion of our bankable Feasibility Study by AMEC in Q3, issuing a revised NI43-101 within 45 days of the Feasibility Study and testing of our vanadium electrolyte for the mass storage industry. We will leverage these near term milestones to pursue a number of key initiatives such as joint ventures and partnerships with international leaders in the Vanadium Flow Battery space and off-takes with steel producers for our early production. Project wise, we are going to put a lot of energy towards increasing the resource thereby extending the mine life. All in all, there is lots going on and lots to look forward to for the remainder of this year and next.

This interview is featured in the article 5 Critical Mineral Stocks to Watch – CLICK HERE – to read more.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |