Copper traded on the US Comex exchange is expected to maintain its price premium over the London Metal Exchange (LME) for at least a year and a half, according to comments delivered Thursday by Robin Martin, head of market development at the LME. Speaking at the World Copper Conference Asia, Martin said the gap between the two benchmarks has become a structural feature of the market and is unlikely to close in the near term.

Martin noted that copper prices on the Comex have consistently traded 2% to 3% above LME levels. He attributed the divergence largely to uncertainty over copper tariffs in the United States, which he said has prompted a shift in how physical metal is stored and priced across exchanges. “There is a persistent premium on the CME contract of 2 to 3% and I do think it is fair to say this is likely now a structural difference in the markets that is likely to persist,” he said.

The price spread has been accompanied by a movement of inventories away from the LME system. Stocks have migrated in large volume to US warehouses, where exchange inventories recently exceeded 400,000 short tons. The build in Comex sheds contrasts with declining levels in LME storage, reflecting changing trading dynamics linked to tariffs and exposure to the US market.

Alongside commentary on pricing trends, Martin outlined steps the LME is taking to broaden access for Chinese market participants. These efforts include making offshore yuan acceptable as collateral and working with major banks in China to ease the process of participation for domestic institutions. He said the exchange is actively pursuing these initiatives as part of a plan to increase engagement with Chinese users.

Martin also said the LME is exploring the potential inclusion of Chinese government bonds as eligible collateral within its clearinghouse. The addition of such instruments would expand the range of financial assets accepted by the exchange and could further integrate Chinese counterparts into LME trading and clearing.

His comments suggest multiple changes in the copper market, one involving the pricing relationship between the US and London benchmarks, and another tied to access and collateral mechanisms aimed at improving participation from China. Both developments indicate evolving structural trends that are influencing trading behavior, inventory distribution, and exchange policy across the global copper trade.

Anglo American’s (LON:AAL) Quellaveco mine in southern Peru has surpassed 1 million tonnes of copper output, a benchmark reached roughly three years after the operation first entered production in 2022. The company disclosed the figure as part of an update on the site’s early operational performance, placing the achievement among the most notable milestones for one of South America’s newest large-scale copper projects.

Quellaveco was designed with an annual nameplate capacity of about 300,000 tonnes during its first decade of operations, and the project’s initial years closely aligned with that plan. According to Anglo American, the mine produced more than 300,000 tonnes of copper in both 2023 and 2024 as performance continued ramping toward steady-state output. The mine is expected to supply between 310,000 and 340,000 tonnes of copper in 2025, consistent with long-term planning assumptions for a project built with an anticipated 36-year operating life.

Company representatives recently pointed to that mine life projection in outlining Quellaveco’s position within Anglo American’s portfolio and the wider global supply landscape. With a multi-decade window of output expected, the operation’s scale is considered significant enough that the company estimates its annual copper production could supply material for more than five million electric vehicles per year. These estimates have been highlighted against the backdrop of rising global consumption of energy transition metals.

The production milestone also brought renewed attention to the mine’s technological and operational framework. Quellaveco operates entirely on renewable electricity and is recognized as the first mining site in Peru to integrate autonomous drilling systems and autonomous haulage fleets. The mine’s remote operations centre and integrated processing technology are intended to allow real-time monitoring, enhance control over production, and stabilize efficiency across long-term output cycles. Anglo American attributes the mine’s performance trajectory to what it describes as a strategy centred on safety, reliability, and advanced technology.

According to executives, these systems form the basis of what they described as a benchmark for sustainable mining operations. They cited the low-carbon power profile and extensive automation as factors intended to improve both safety outcomes and productivity while reducing energy intensity in day-to-day operations.

The company’s comments were released at a time when copper demand projections continue to intensify due to population growth, urbanization, and global efforts to reduce emissions. Anglo American has estimated that meeting future consumption trends may require the development of the equivalent of roughly 60 new mines of Quellaveco’s scale by the year 2040. Industry analysts have noted similar supply-demand pressures, although the pace and scale of actual mine development remain subject to permitting challenges, investment cycles, and political conditions across major copper-producing regions.

With Quellaveco now marking its first major cumulative output milestone, Anglo American has emphasized the long-term operational horizon still ahead. The mine, one of the largest recent additions to Peru’s copper sector, is expected to remain a central component of the company’s copper portfolio for decades as global markets continue to track supply constraints and emerging demand linked to electrification trends.

Harmony Gold (NYSE:HMY) has approved the construction of its Eva copper project in Australia, committing $1.6 billion to a development plan that will begin in the third quarter of 2026 and extend over a three-year build period. The company expects the new mine to begin production in the second half of 2028, marking a major expansion of its presence in the copper sector.

The decision follows two years of study and planning since Harmony acquired Eva in 2022 from Copper Mountain Mining for approximately $230 million. During that time, the company refined the project’s design, updated production estimates, and evaluated the operational role Eva would play in its long-term strategy.

According to the updated plan, the Eva mine is expected to produce 65,000 tonnes of copper per year during its first five years of operation, followed by an average of 60,000 tonnes annually over a projected 15-year mine life. Alongside copper, the operation is also forecast to yield 19,000 ounces of gold per year. The company stated that the operation would carry an all-in sustaining cost of $2.50 per pound of copper.

Harmony chief executive Beyers Nel said the company views the long-term outlook for both copper and gold as supportive of a diversified production profile. He noted that the combination of copper and gold at Eva should help support free cash flow generation while reducing broader business risk. Nel also said that both Eva and the company’s recent acquisition of MAC Copper would provide Harmony with a wider base of metals exposure, which he described as strengthening cash flow through various commodity cycles.

Harmony completed the acquisition of MAC Copper earlier this year in a $1 billion transaction that brought the CSA copper mine in New South Wales into its portfolio. The CSA mine produces about 41,000 tonnes of copper annually. Together, the MAC Copper acquisition and the development of the Eva project are central to Harmony’s plan to grow its copper output to around 100,000 tonnes per year.

The company said that this targeted production level is expected to be reached within five years once Eva is operational and integrated with the CSA mine’s contribution. Funding for Eva’s construction is planned to come from internal cash flow and debt, with Harmony stating that it intends to maintain its existing dividend policy during the development period.

While the Eva project represents a significant capital commitment, Harmony emphasized that the combination of its copper assets aligns with its strategy to expand beyond gold and position itself within metals critical to long-term demand trends. The company has not indicated any adjustments to its wider operational footprint but noted that growth in copper output is now a central component of its near-term and medium-term planning.

A long-standing pricing framework that underpins the global copper-processing sector is heading toward a critical test as the industry enters a new round of negotiations this week. The annual discussions, set against a backdrop of constrained concentrate supply and heightened geopolitical tensions, are taking place in Shanghai, where miners and smelters traditionally attempt to establish treatment and refining charges—known as TC/RCs—for the coming year.

This time, however, several participants expect the structure that has guided copper processing for decades to come under unprecedented stress. The challenge stems from a supply imbalance that has widened as processing capacity—especially in China—has grown faster than mined copper output. Analysts say this divergence has eroded the predictability of yearly benchmarks and raised the likelihood that some parties may pursue alternative pricing arrangements for 2026.

Pressure Building Around the Benchmarking Process

The annual system operates on an assumption that major miners and China’s smelters strike an agreement first, creating the figure that the rest of the industry generally adopts. But the severe drop in fees this year has created uncertainty over whether that model remains sustainable.

TC/RCs collapsed to record lows, and a “further breakdown” in the benchmark is expected, according to Craig Lang of CRU Group. He said companies are already exploring the possibility of bilateral contracts, caps and floors on fees, or more frequent pricing such as quarterly settlements.

Panmure Liberum analysts led by Tom Price described the unfolding dynamic as “a brutal game of industrial survival,” noting it will frame the upcoming negotiations for 2026.

China’s Expansion at the Center of the Dispute

Much of the strain originates in China, which has continued to rapidly expand its smelting capacity despite falling processing fees. Spot treatment charges have turned negative at times—dropping to as low as minus $60 per ton this year—meaning processors have effectively paid miners to access concentrate.

While some Chinese smelters have managed to remain profitable due to strong prices for refined copper and sulfuric acid, this environment has contributed to closures or distress in smelting operations outside China. China’s refined copper output rose 9.7% in the year through October, and its producers have been able to capitalize on elevated refined metal prices, which remained steady at $10,777 a ton on the London Metal Exchange by midday Monday in Shanghai. The price is below but still close to the record above $11,200 reached in late October.

Panmure Liberum analysts said China is “crowding out players abroad by securing the lion’s share of global concentrate supply and crushing the trade’s fee structure.”

Li Chengbin at Mysteel Global pointed to the widening gap between term TC/RCs and spot markets as another factor undermining confidence in the benchmark system. He said there are increasing concerns over how much concentrate Chinese smelters will be able to secure through annual contracts.

Smelters Outside China Push Back

Across multiple countries, smelters are seeking better contractual terms in response to deteriorating economics. A notable shift has emerged among Japanese operators, which are coordinating to strengthen their position against miners. Mitsubishi Materials Corp. said conditions have “significantly deteriorated,” underscoring the pressure on non-Chinese processors.

Government agencies have also intervened. In October, ministries from Japan, South Korea and Spain issued a joint statement criticizing what they described as punitive TC/RCs and warning against “policies and practices that may not reflect fair market dynamics.”

Operational strain is already visible. JX Advanced Metals Co. in Japan announced an output reduction measured in the tens of thousands of tons. In Australia, Glencore Plc received a government bailout to keep its Mount Isa smelter and refinery operating for an additional three years.

Some miners are also reconsidering their participation in the annual benchmark. Freeport McMoRan Inc. has signaled it may pursue alternative pricing strategies based on concerns about the long-term viability of its smelter customers.

A Structural Shift in Concentrate Supply

While last year’s tight concentrate market initially appeared temporary, disruptions at major mines—together with China’s relentless additions to smelting capacity—have contributed to a more persistent supply squeeze. For much of the past decade, TC/RCs have generally moved in line with the balance of mined material and processing demand. The current divergence suggests a structural change rather than a short-term anomaly.

Analyst Xu Wanqiu of Cofco Futures said Chinese smelters are likely to continue securing raw material as long as they can afford to pay for it. Even if market conditions worsen, he expects only limited pullback from Chinese processors next year due to anticipated new capacity and efforts to support broader economic objectives.

As the industry gathers in Shanghai, companies on all sides are grappling with how to maintain operations in a system where fees have fallen to unprecedented lows. The outcome may determine whether the decades-old benchmarking structure remains viable or gives way to a more fragmented, individualized approach to copper processing contracts.

The talks are expected to be contentious. Miners, aware of the ongoing tightness in concentrate supply, are anticipated to push for tougher terms in 2026. Smelters outside China are warning that current economics threaten their survival. And Chinese smelters, despite facing low fees themselves, are still positioned to dominate raw material procurement due to their scale and the strength of refined copper and byproduct markets.

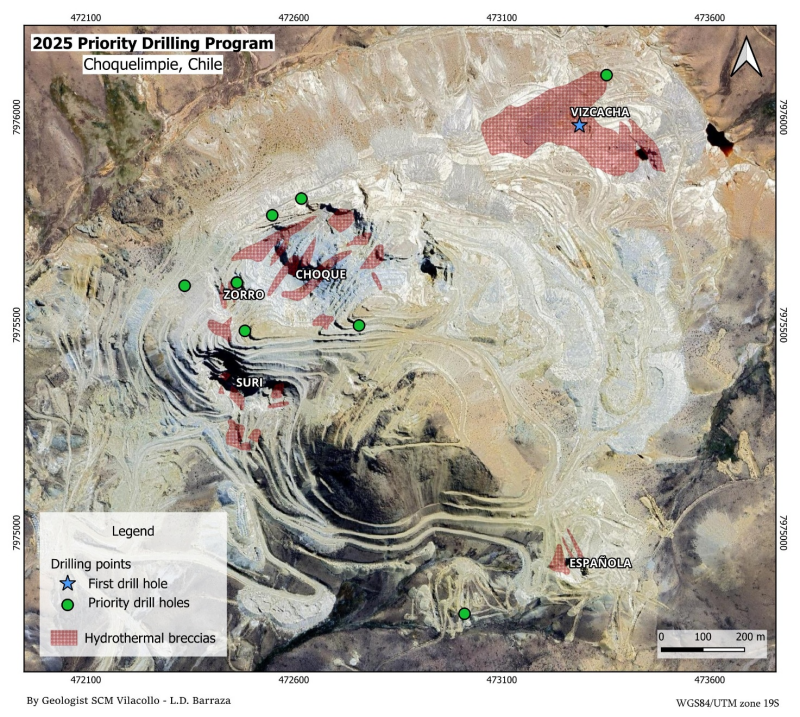

Norsemont Mining (CSE:NOM) has initiated drilling activities for the latest phase of exploration at its wholly owned Choquelimpie high-sulfidation gold-silver-copper project in northern Chile. The company reported that the first diamond drill hole of the Phase 3 program has been collared, coinciding with the arrival of a second drill rig that will be used to accelerate work through the end of December.

The announcement marks the start of a program designed to test deeper and potentially higher-grade zones within the Vizcacha hydrothermal breccia. Drilling will be carried out by DV Drilling Ltd. of Coquimbo, Chile, which is operating a Longyear LF230 truck-mounted drill on a 24-hour schedule. All analytical work will be conducted at Activation Geological Services SpA (AGS), an ISO 17025-certified laboratory located in Coquimbo.

Initial Hole Collared at Vizcacha Zone

The first hole of the campaign, MV25-DD01, has been positioned at coordinates E473,285 and N7,975,980 at an elevation of 4,694 meters. It was collared at an azimuth of 275 degrees, inclined at 70 degrees, and is planned to reach a depth of 225 meters. According to the company, the target is an area where higher-grade gold mineralization has been modeled within the Vizcacha hydrothermal breccia.

Norsemont stated that MV25-DD01 has been specifically designed to explore the Vizcacha Zone at depth, beneath the area where grades were calculated in the April 2025 resource model. Historical drilling in the Vizcacha deposit largely focused on shallow rotary holes, and the company intends to expand the geological understanding of the deeper breccia system through this hole.

Scope of the Phase 3 Program

The Phase 3 exploration campaign is planned to include up to 5,000 meters of diamond drilling, utilizing two diamond drill rigs. Drilling is scheduled to continue into late December. The broader design of the program comprises up to 20 holes, each averaging approximately 250 meters. Priority drill stations for the campaign were outlined in figures accompanying the company’s release.

The focus of this phase is to evaluate down-dip extensions of high-grade gold mineralization hosted within hydrothermal breccia zones. Norsemont is conducting the program through its wholly owned Chilean subsidiary, SCM Vilacollo. Oversight of the exploration activities is being provided by Roman Flores, a Persona Calificada (Q.P.) with the Commission Minera Chile.

Operational and Technical Framework

Drill core from the program will be handled using established sampling and analytical procedures, with assays completed at AGS’s ISO 17025-certified facility. The Vizcacha target, described by Norsemont as a hydrothermal breccia zone with potential for higher-grade gold, will be assessed using deeper drilling than historically conducted in the area. The company reiterated that MV25-DD01 is expected to intersect this breccia zone at depth.

With the second drill rig now on site and the first hole underway, the company plans to maintain continuous drilling activity through the final weeks of the year. Results from the ongoing work will contribute to future evaluations of the Choquelimpie project’s mineral potential and may inform subsequent project development planning.

Chile’s state copper commission, Cochilco, sharply increased its price expectations for the metal over the next two years, citing weak output across several major operations and a broader structural imbalance between supply and demand. The updated figures, released Wednesday, mark the highest annual copper price forecasts the commission has ever issued.

The agency now projects an average price of $4.45 per pound in 2025, revising upward from its previous estimate of $4.30 per pound. Its 2026 forecast has also been raised to $4.55 per pound, compared with an earlier outlook of $4.30 per pound. Both forecasts set new record highs for the commission’s long-term projections.

According to Victor Garay, Cochilco’s mining market coordinator, the commission expects copper prices to remain on an upward trajectory through at least 2030, driven by persistent supply constraints that fail to keep pace with global demand. Garay noted that while the long-term trend appears favorable for prices, several risks remain. These include potential tariff changes and the possibility of a shift in demand patterns, either of which could affect the outlook.

A tighter supply picture in Chile—still the world’s largest producer of copper—has played a central role in the forecast revision. Cochilco reported that weak performance at the Collahuasi mine, which is jointly operated by Anglo American and Glencore, has contributed to lower-than-expected production volumes. The agency also highlighted reduced output from Anglo American Sur and the impact of an accident at Codelco’s El Teniente mine, one of the country’s flagship operations. Taken together, these setbacks have constrained national production levels. Cochilco now expects Chilean copper output to grow only 0.1% this year, reaching 5.51 million metric tons. Production is projected to increase 2.5% in 2026, bringing total output to 5.6 million metric tons.

Garay added that despite the disruption at El Teniente, other operations are expected to compensate for the mine’s reduced production going forward, supporting an anticipated recovery. Cochilco believes Chilean copper production could reach 5.9 million metric tons in 2027 as these adjustments take effect.

On the demand side, Cochilco anticipates continued growth in global consumption of copper, although the commission described this expansion as occurring with “less dynamism” than in previous periods. Still, even moderated demand growth reinforces an environment in which supply struggles to keep up, contributing to the bullish pricing outlook.

The combination of muted near-term production gains, incidents affecting major mines, and sustained demand has underpinned Cochilco’s decision to issue its most optimistic copper price forecasts on record. While the commission maintains confidence in the upward trend through the end of the decade, it continues to watch for potential policy or macroeconomic developments that could alter the trajectory.

Freeport McMoRan (NYSE:FCX) has outlined a schedule to restore large-scale output at Indonesia’s Grasberg minerals district in the second quarter of 2026, marking the first detailed timeline since a fatal incident earlier this year forced a major operational shutdown. The US-based copper producer disclosed the plan Tuesday, noting that remediation and preparatory work at the Grasberg Block Cave underground mine is currently underway to enable a phased restart.

The company suspended Block Cave operations after a Sept. 8 mudslide sent roughly 800,000 metric tons of saturated material into the underground workings. Seven workers were killed in the event, which Freeport described as catastrophic. The firm subsequently declared force majeure and initiated an investigation into the causes of the incident. Although the inquiry has been completed, Freeport has not yet released its findings publicly.

Operations at two other Grasberg underground mines — the Deep Mill Level Zone (DMLZ) and Big Gossan — resumed earlier, with the company stating that neither was affected by the September mud flow. Together with Block Cave, these sites form the core of one of the world’s largest integrated copper-gold mining complexes, previously producing approximately 1.7 billion pounds of copper and 1.4 million ounces of gold per year. The Grasberg district sits in the remote highlands of the Sudirman Mountains in Central Papua.

Grasberg is operated by Freeport, which holds an interest of about 49%, while the Indonesian government owns the remaining stake. The company said its future planning incorporates lessons from the September event. “We have incorporated the learnings from the recent tragic incident into our future plans and are implementing several initiatives to address the conditions that led to the incident,” chief executive Kathleen Quirk stated in Tuesday’s announcement.

The company also updated its multi-year production outlook. For 2026, Freeport expects Grasberg’s output to be on par with 2025 levels — roughly 1 billion pounds of copper and 900,000 ounces of gold. These figures are about 35% below the company’s earlier projections, following a downward revision in September after the incident disrupted long-term mine sequencing.

Production levels are forecast to increase between 2027 and 2029, averaging 1.6 billion pounds of copper and 1.3 million ounces of gold annually over the three-year period. The Block Cave mine is expected to supply about 70% of output during those years, reflecting its role as the source of half of Grasberg’s total mineral reserves.

Copper has officially been added to the U.S. government’s list of critical minerals—those deemed essential to the country’s economic and national security. Yet, in a paradoxical twist, the United States already possesses one of the world’s largest copper stockpiles, second only to China’s. The accumulation has occurred without any federal intervention or taxpayer spending, fueled instead by market dynamics and a widening pricing gap between U.S. and international copper markets.

Over the past year, the U.S. copper market has seen a surge in physical metal inflows as traders capitalized on the arbitrage opportunity between the higher-priced contracts traded on the Chicago Mercantile Exchange (CME) and the lower prices quoted on the London Metal Exchange (LME). The growing premium on U.S. copper—at times reaching extraordinary levels—has incentivized the world’s major traders to divert shipments toward American shores.

This unintentional buildup has created what analysts describe as a de facto strategic stockpile of copper, though it is held by commercial entities rather than the federal government. Consultancy Benchmark Minerals Intelligence estimates that between 731,000 and 831,000 metric tons of copper are now “economically trapped” within the United States. The term refers to the fact that current market conditions make it uneconomical to re-export the metal without a significant reversal in the price differential between U.S. and global markets.

The Arbitrage Opportunity

The roots of this phenomenon can be traced to February, when President Donald Trump ordered an investigation into copper imports on national security grounds. The market swiftly priced in the potential for tariffs similar to those already imposed on steel and aluminum, prompting a wave of speculative and physical trading activity.

By July, the premium for U.S.-traded copper over its London counterpart had ballooned to nearly $3,000 per metric ton. Traders rushed to take advantage, shipping as much refined copper as possible into the U.S. market. However, that premium collapsed almost overnight when the Trump administration surprised traders by announcing tariffs on semi-manufactured copper product, while deferring a decision on refined metal until July 2026.

Although the arbitrage narrowed temporarily, it has since widened again. After dipping below $100 per ton in August, the spot CME premium has climbed back above $300, while the 10-month forward premium is nearing $800 per ton. These levels, though below the mid-year extremes, remain sufficient to cover shipping and handling costs, ensuring that physical inflows continue.

The U.S. as the Copper Market of First Resort

The most visible sign of this trade pattern is the rapid accumulation of copper in CME-registered warehouses, which serve only domestic delivery points. From a low of 83,900 tons in February, CME stocks have surged to more than 335,000 tons—now exceeding the combined inventories held by both the LME and the Shanghai Futures Exchange.

Shipments continue to arrive daily, primarily through New Orleans, with additional inflows reported in Baltimore, Salt Lake City, and Tucson. These visible stocks may represent only a portion of the total volume now held within the country’s borders. Benchmark’s analysis suggests that the overall quantity of copper now effectively immobilized in the U.S. market is far greater.

Trade statistics support this assessment. Despite disruptions to government data reporting due to the recent shutdown, figures from earlier in the year showed that refined copper imports reached more than one million tons in the first seven months of 2025—an increase of roughly 400,000 tons over the same period in 2024. Export data from key suppliers such as Chile, Peru, and Australia indicate that shipments to the U.S. have remained strong since then.

Rising Costs Reflect Tightening Supply Dynamics

The United States’ role as the preferred destination for surplus copper has had ripple effects throughout the global supply chain. Europe’s largest copper producer, Aurubis, has raised its premium for 2026 deliveries by 38% to a record $315 per ton over the LME benchmark. Analysts attribute the move in part to the strong U.S. demand that has tightened availability elsewhere.

As the market continues to anticipate potential policy changes—including the prospect of tariffs on refined copper imports—many traders expect the arbitrage gap to persist or even widen further. This would reinforce the United States’ status as a magnet for global copper supplies.

The result is an unusual market outcome: the creation of what amounts to a national copper reserve, built not through government procurement or strategic planning but through arbitrage-driven private accumulation. The combination of trade policy uncertainty, market speculation, and the new “critical mineral” designation has effectively concentrated vast quantities of the metal inside the U.S. economy.

While the formal intent behind the critical minerals list is to safeguard national supply chains, in copper’s case the market may have already achieved that objective on its own. The metal’s growing domestic inventory base—though held by private entities—now functions as a buffer against potential supply disruptions, trade barriers, or geopolitical shocks.

A long-anticipated lithium joint venture between Chilean state-owned copper producer Codelco and local miner Sociedad Química y Minera de Chile (SQM) has received approval from China’s antitrust authority, removing the final major obstacle before the deal can take effect. The Chinese regulator’s decision, announced Monday, concludes nearly two years of international reviews and sets the stage for the partnership to begin operations in the country’s key lithium-rich Atacama salt flat.

The agreement, first unveiled in late 2023, is part of Chile’s broader effort to expand state participation in the lithium sector and increase production of the metal, a key input for electric vehicle batteries and energy storage systems. Chile is currently the world’s second-largest lithium producer, after Australia, and the Atacama salt flat is one of its most productive resources.

Beijing’s Conditions on Supply and Pricing

China’s State Administration for Market Regulation (SAMR) said it granted its approval on condition that the companies guarantee access to lithium for Chinese customers. The regulator required Codelco and SQM to maintain a minimum supply to China at “fair” terms, specifying that prices should not exceed a certain percentage of benchmark market prices. While the specific terms remain confidential, SAMR emphasized that the two firms must avoid any action that restricts or delays supply to Chinese clients.

“In the event of a major supply change, both sides should make reasonable and best efforts to continue the supply of lithium carbonate products to Chinese customers… they should not turn down, restrict or delay supply to Chinese clients,” SAMR said in its statement.

The regulator added that its decision was based on feedback from various sources, including government agencies, industry associations, competitors, and downstream buyers. It also directed both companies to uphold strict corporate governance standards and to avoid sharing commercially sensitive information with other lithium producers.

SQM said in a regulatory filing that the Chinese conditions were consistent with its current business practices in China, one of its key export markets.

International Reviews and Local Oversight

China’s approval was the final regulatory step needed after a series of reviews in multiple jurisdictions. Competition regulators in Chile, the European Union, Brazil, Japan, South Korea, and Saudi Arabia had previously granted clearance for the deal.

In Chile, the country’s comptroller’s office must still sign off before the partnership can take effect. Codelco said in a separate statement that it expects this final domestic approval to be granted soon, describing it as a procedural formality. A company source indicated that the process should be completed before the end of the year.

The new alliance is expected to formalize joint operations between Codelco and SQM in the Atacama region, aligning with Chile’s national lithium strategy, which seeks to increase state influence over strategic natural resources while maintaining private-sector partnerships.

Political Context and Industry Reaction

Chile’s recently appointed economy minister, Álvaro García, stated in August that the government anticipates the Codelco–SQM deal will be finalized before the current administration leaves office in 2026. The partnership has drawn attention both domestically and internationally due to its potential to reshape the structure of Chile’s lithium sector.

However, the deal also faced opposition from some lawmakers and from China’s Tianqi Lithium, which holds a significant stake in SQM. Tianqi had raised concerns about the structure and transparency of the agreement but has not publicly commented since the Chinese approval was announced.

Toward Implementation

With the final regulatory hurdle cleared, Codelco and SQM can now move toward implementation of their joint venture, marking a new phase in Chile’s lithium industry. The companies plan to increase production capacity in the Atacama salt flat while meeting the government’s objectives for greater state participation in critical mineral projects.

Once the Chilean comptroller’s sign-off is secured, the partnership will formally commence operations, potentially before the end of 2025.

Mayfair Gold Corp. (TSXV: MFG, OTCQX: MFGCF) has provided a detailed update on development activities at its 100%-owned Fenn-Gib gold project in the Timmins region of Northern Ontario, including the launch of a tightly spaced drill program, ongoing geotechnical investigations for the tailings storage facility, and progress toward completion of the project’s Pre-Feasibility Study (PFS) later this year.

Nick Campbell, CEO of Mayfair Gold, commented in a press release: “The Fenn-Gib deposit is unique in that the highest-grade material occurs near the surface which allows for the potential to start operations with a smaller, targeted mining operation focused on low strip ratio, high-grade gold mineralization. Rather than pursue a larger scale operation, the grade distribution at Fenn-Gib provides Mayfair the optionality to fast-track the extraction of high margin material while at the same time mitigating construction risk and initial capital requirements. It also has the benefit of allowing us to follow the well-defined Ontario Provincial permitting process. With the Canadian gold price currently above C$5,000 per ounce, Mayfair is encouraged by the opportunity to rapidly advance the Fenn-Gib Project as a potential new gold producer within the current cycle. The Pre-Feasibility Study remains on track for completion in Q4 2025. We believe a nimble, high-grade, and targeted operation offers a practical path toward a potential production decision within the next three years.”

PFS Nearing Completion Based on Updated Resource Estimate

The upcoming PFS, expected in the fourth quarter of 2025, is being prepared using the updated NI 43-101 Mineral Resource Estimate (MRE) announced in October. The study will form the basis for mine planning and will prioritize near-surface, higher-grade portions of the open pit to maximize early cash flow. The design envisions a conventional open pit operation using standard drill-and-blast techniques with a truck and shovel fleet.

Mayfair is employing an elevated cut-off grade strategy to focus on these near-surface zones while preserving the broader mineral resource base. According to conceptual plans, an open pit based on a 0.7 g/t Au cut-off grade highlights the potential configuration of a high-grade starter pit that could enhance the project’s initial economics.

High-Density Drilling to Refine Starter Pit Model

To further improve confidence in near-surface mineralization, the company has commenced a detailed diamond drilling program within the planned starter pit. Although 97% of the deposit is already classified as indicated, Mayfair launched a 56-hole program spaced 10 by 10 metres apart to verify grade continuity and support future mine design.

Each hole, drilled vertically to a depth of approximately 75 metres, contributes to a total of roughly 4,200 metres. The work is aimed at delineating mineralization expected to feed the processing plant during the early years of production, aligning with the company’s strategy to optimize grade and cash flow in the project’s initial phase.

Drilling began on October 21, 2025, and is scheduled to continue through December. The program is being conducted by Black Diamond Drilling, a contractor from the neighbouring Apitipi Anicinapek Nation. The campaign is also expected to generate new data for metallurgical recovery testing and for calibration of geological and hydrogeological models.

Progress on Tailings Storage Facility Site Work

Geotechnical investigations have advanced to support the engineering design of the project’s tailings storage facility (TSF). The program consisted of 25 test pits and 347 metres of drilling across 10 holes around the TSF footprint. Knight Piésold, which is leading the TSF design, oversaw the fieldwork.

The data collected will refine understanding of the overburden and subsurface conditions that inform foundation and structural designs. Additional site investigations are planned for 2026 as the project moves into later stages of engineering.

Mayfair’s Chief Operating Officer, Drew Anwyll, P.Eng., said the site characterization work is critical to reducing development risks. “A thorough understanding of material properties and underfoot conditions leads to improved foundation and building designs,” he stated, emphasizing that early-stage geotechnical programs play a significant role in project execution confidence.

Remaining Steps Toward the Pre-Feasibility Study

The company reported that the PFS remains on schedule, with outstanding work focused on integrating the results from the latest site investigations into the earthworks and construction planning. These findings will be incorporated into final cost estimates and the overall economic model.

Mayfair also noted that suppliers and contractors are currently facing strong demand driven by higher gold prices, creating a competitive procurement environment. Canadian gold prices remain above C$5,000 per ounce, a level management considers favorable for advancing the Fenn-Gib Project into production within the current gold cycle.

The Fenn-Gib deposit remains Mayfair’s flagship asset. The most recent NI 43-101 compliant resource estimate, effective September 3, 2024, outlines an indicated resource of 181.3 million tonnes grading 0.74 g/t gold for 4.3 million contained ounces, and an inferred resource of 8.9 million tonnes at 0.49 g/t gold containing 141,000 ounces. The estimate applies a 0.3 g/t Au cut-off and is constrained within an open pit shell.

Australia’s Pilbara Minerals (ASX: PLS) is warning that the country’s lithium industry is losing ground to faster-moving competitors, particularly Brazil, where the miner says it has found operations to be smoother and more cost-effective than at home.

Speaking at the WA Mining Club in Perth on Thursday, chief executive officer Dale Henderson said that while Brazil’s Minas Gerais state shares many similarities with Western Australia, the regulatory and operational environment there has so far proven more favorable for mining companies. “We would join the chorus of many others who say it’s got more difficult [in Australia],” Henderson told attendees. “This state, and Australia at large, has been leading the world in resources, but we can lose that mantle.”

Pilbara Minerals completed a A$560 million ($363 million) acquisition earlier this year to secure its foothold in Brazil, part of a broader strategy to diversify geographically and strengthen supply chain resilience. Henderson said that after only a few months on the ground, the company’s experience in Brazil underscored the competitive pressures facing Australian miners.

Henderson cautioned that while Australia remains a dominant player in lithium production, other jurisdictions are growing faster. “Others are growing faster. We’re regressing relative to the rest,” he said. “If we don’t have a successful upstream, we certainly can’t have successful downstream – one leads to the other.” The comments highlight mounting concerns within Australia’s mining sector that regulatory delays, high energy costs, and slow infrastructure development are eroding the country’s global advantage in critical minerals. Henderson urged the government to refocus policy on competitiveness, emphasizing that shared infrastructure and energy availability should be top priorities.

Henderson pointed to the Lumsden Point port development in Western Australia as a model of effective government intervention. “That’s a no-brainer,” he said. “Then after that, it is power infrastructure. Those would be really the two key areas.”

Energy costs were singled out as a growing obstacle for lithium producers. Henderson noted that at Pilbara’s Salinas project in Brazil, electricity is expected to cost between A4–5 cents per kilowatt hour, less than half the A10–20c/kWh currently paid in the Pilbara. “Australia should have low-cost power. We’ve got the space. We’ve got the solar, wind – you name it,” he said. “That’s a key place for government to play – to leverage the incredible strengths we’ve got to bring that cost of power down.”

Market Volatility and Industry Outlook

The Pilbara chief also reflected on the challenges of operating in a still-maturing lithium market characterized by extreme price swings. Pilbara Minerals has endured wide fluctuations in spodumene prices, from lows of around $400 per tonne in 2019 to over $8,000/t during the 2022 boom. Henderson said such volatility was typical of an industry still developing mechanisms for reliable price discovery.

“It explains some of the outsized responses you can get from news or gossip, but ultimately, I think that will get remedied as the industry grows,” he said.

Despite short-term instability, Henderson maintained a positive long-term view. He said the company sees recent price gains as a sign of recovery, with spodumene rising above $900/t last month, up from around $600/t in July. “Our view remains that there’s a structural deficit to emerge, ultimately, given the strong growth, the strong growth drivers and the absence of supply chain investment,” he said. “The big question everyone is wrestling with is when?”

Brazil as a Competitive Benchmark

The contrast between conditions in Brazil and Australia appears to be reinforcing Pilbara Minerals’ strategy to internationalize its operations. Minas Gerais, a state long associated with iron ore and industrial minerals, is emerging as a new hub for lithium development, supported by improving infrastructure and a growing domestic battery materials industry.

For Pilbara, which has built its reputation as one of the world’s leading spodumene producers, Brazil offers not only a hedge against market and policy risks at home but also a testing ground for how quickly other nations can build competitive supply chains.

Henderson’s comments underscore a growing sentiment in Australia’s mining industry: that the nation’s leadership in critical minerals is not guaranteed. With rising costs, slower permitting, and intensifying global competition, miners are increasingly looking abroad for growth—and Brazil, it seems, is quickly becoming one of the preferred destinations.

Lundin Mining (TSX: LUN) has raised its full-year copper production forecast and lowered its cost outlook after reporting stronger-than-expected results from its Caserones mine in Chile. The company now expects to produce between 319,000 and 337,000 tonnes of copper in 2025, up about 4% from its previous guidance of 303,000 to 330,000 tonnes.

The revised forecast comes alongside an improvement across key financial metrics, including production, revenue, and earnings. In its latest quarterly report, the Vancouver-based miner said it generated over $1 billion in revenue and delivered $383 million in adjusted operating cash flow. Copper output, revenue, EBITDA, and earnings all increased compared with both the first and second quarters of the year.

Average consolidated copper cash costs dropped to $1.61 per pound, about 6% lower than in 2024 and the company’s lowest quarterly level so far this year. “We are updating our full-year guidance to reflect strong operational performance, particularly at Caserones,” said president and CEO Jack Lundin. He noted that the midpoint of the company’s copper production outlook had increased by 11,500 tonnes, reaching a new midpoint of 328,000 tonnes within the revised range.

The stronger output at Caserones, along with improved results from the Chapada mine in Brazil, prompted Lundin Mining to cut its overall copper cash cost guidance to $1.85–$2 per pound. “Strong performance at Caserones and Chapada resulted in cost guidance cuts of approximately 12% and 21%, respectively, driving the overall cost reduction,” said Matt Murphy, analyst at BMO Capital Markets. He added that the company appears on track to achieve its updated targets, having already produced 75% of the copper guidance midpoint for the year and currently tracking below the midpoint of the new cost range.

Production and sales figures also outperformed expectations. Lundin’s copper output reached 87,400 tonnes, exceeding the market consensus of 81,100 tonnes. Gold production came in at 37,800 ounces, closely matching forecasts of 37,600 ounces. Copper sales totalled 78,800 tonnes, ahead of expectations of 76,400 tonnes, while gold sales of 38,800 ounces topped consensus estimates of 36,000 ounces.

The company’s operational improvements led analysts to boost their outlook for the stock. BMO’s Murphy raised his price target for Lundin Mining by 14% to C$25, citing a stronger operational record and long-term growth potential.

Alongside its financial update, Lundin announced a leadership change connected to its joint ventures in South America. Ron Hochstein, who has served as president and CEO of Lundin Gold (TSX, NASDAQ: LUG) since 2015, will become the chief executive officer of Vicuña Corp. on Friday. The newly created entity is a joint venture between Lundin Mining and BHP (ASX, NYSE: BHP) overseeing the Filo del Sol and Josemaría copper-gold projects straddling the Chile-Argentina border.

Under Hochstein’s leadership, Lundin Gold developed Fruta del Norte in Ecuador, one of only two large-scale operating mines in the country. He has previously described the project as “a standard for responsible mining development.”

The combination of strong operating performance in Chile and Brazil, lower production costs, and strategic leadership changes at the corporate level have positioned Lundin Mining for what analysts see as a more confident close to the year.

Solaris Resources (TSX: SLS; NYSE: SLSR) released results of a Pre-Feasibility Study (PFS) for its Warintza copper-molybdenum project in southeastern Ecuador, reporting a maiden open-pit mineral reserve of 1.3 billion tonnes at 0.41% copper-equivalent (CuEq) and a 22-year life-of-mine (LOM) constrained by tailings storage design. The study outlines average annual CuEq production of more than 300,000 tonnes in the first five years and over 240,000 tonnes during the first 15 years, with a post-tax NPV (8%) of US$4.617 billion, a post-tax IRR of 26%, and a 2.6-year post-tax payback.

Production, costs and economics

The PFS contemplates 60.2 Mt per year of throughput and LOM average Cu head grades of 0.31% with 84% Cu recovery. Average annual copper production is 230 kt in years 1–5 and 183 kt in years 1–15, alongside by-products averaging 8.6 kt/y molybdenum, 57 koz/y gold and 1.3 Moz/y silver during the first 15 years. LOM totals are 3,436 kt Cu, 154 kt Mo, 1.079 Moz Au and 26.6 Moz Ag. Unit operating costs total US$9.74/t milled in the first five years (US$8.75/t LOM), including mining US$3.38/t milled in the first five years (US$2.40/t LOM), processing US$5.58/t and G&A US$0.78–0.79/t. C1 cash costs are projected at US$0.59/lb Cu payable in the first five years (US$1.01/lb LOM) and AISC at US$0.85/lb in the first five years (US$1.25/lb LOM). Average annual EBITDA is US$1.9bn in the first five years and US$1.4bn during the first 15 years; average annual post-tax free cash flow is US$1.3bn and US$1.0bn over the same periods, respectively. Total post-tax free cash flow over the mine life is estimated at US$13.5bn. Initial capital (including 15.7% overall contingency) is US$3.729bn, with sustaining capital of US$1.713bn and closure costs of US$200m. Capital intensity over the first 15 years is ~US$15,440 per average tpa-CuEq. Base-case metal prices used for the economic analysis are copper US$4.50/lb, molybdenum US$20/lb, silver US$28/oz and gold US$2,800/oz for the first three years then US$2,500/oz thereafter. Sensitivity analysis indicates the post-tax NPV (8%) is most sensitive to copper price (or equivalently copper grade), followed by LOM operating costs, initial capital and molybdenum price.

Reserves, resources and strip ratio

Proven reserves total 797 Mt at 0.49% CuEq (0.37% Cu, 0.02% Mo, 0.05 g/t Au, 1.37 g/t Ag) and probable reserves 503 Mt at 0.28% CuEq (0.22% Cu, 0.01% Mo, 0.03 g/t Au, 1.19 g/t Ag). Payable metal assumptions are Cu 96.5%, Au 91%, Ag 91% and Mo 100%. Oxide and mixed material comprise <0.02% of total reserves. The LOM average strip ratio is 0.53:1; the first-five-years strip ratio is 0.37:1. A maiden 2025 Mineral Resource Estimate (MRE) reports Measured plus Indicated resources of 3.746 Bt at 0.32% CuEq (0.24% Cu, 0.01% Mo, 0.04 g/t Au, 1.19 g/t Ag) and Inferred resources of 2.092 Bt at 0.20% CuEq (0.16% Cu, 0.01% Mo, 0.02 g/t Au, 1.11 g/t Ag), at a 0.1% Cu cut-off within an optimized pit and an NSR cut-off of US$6.30/t. Oxide and mixed material account for <0.01% of resources. The company reports a 312% increase in Measured + Indicated tonnage relative to its 2024 MRE following an additional ~75,000 m of drilling (total ~177,118 m) and initial inclusion of Warintza West. The 2025 MRE incorporates silver grades and a change from a 0.25% CuEq reporting cut-off in 2024 to the stated NSR + 0.1% Cu cut-off. The effective date of the resource and reserve estimates is May 1, 2025.

CuEq methodology. For sulphide material: CuEq (%) = Cu (%) + 3.94 × Mo (%) + 0.52 × Au (g/t) + 0.01 × Ag (g/t). Mixed: CuEq (%) = Cu (%) + 3.76 × Mo (%) + 0.50 × Au (g/t) + 0.005 × Ag (g/t). Oxide: CuEq (%) = Cu (%). The PFS notes that mineral resources are inclusive of reserves and that resources that are not reserves do not have demonstrated economic viability.

Mine design and schedule

Warintza is planned as a conventional owner-operated open pit developed through two main pits (Warintza Central and Warintza East) and eight phases to sequence higher-grade ore early. The operation targets steady-state ore production of ~60.2 Mt/y after a two-year pre-strip. The primary fleet includes 120-t class cable shovels, 70-t wheel loaders and 320-t haul trucks, supported by dozers, graders and water trucks. Bench heights range 15–30 m; dual-lane haul roads are 40 m wide; slope angles are 36°–47° depending on geotechnical domains. Drilling and blasting will use 311 mm holes; annual explosives consumption peaks at ~46,000–58,000 t. Approximately 221 Mt of low-grade ore is scheduled for stockpiling and later processing, with LOM balances constrained by tailings storage limits; later years transition primarily to stockpile reclaim ahead of closure and reclamation.

Processing and product

The 165,000 t/d (60.2 Mt/y) concentrator is a conventional Cu-Mo flowsheet treating predominantly hypogene chalcopyrite with some supergene chalcocite/bornite. Ore will be primary- and secondary-crushed, then ground in two lines each with a 24 MW dual-pinion SAG mill and two 22 MW dual-pinion ball mills to P80 150 µm. Rougher flotation concentrate will be reground to P80 25 µm and cleaned in three stages to produce a bulk Cu-Mo concentrate for downstream separation. Copper and molybdenum concentrates will be dewatered for offsite smelting. Tailings will be thickened; cyclone stations will produce sand for dam construction with fines deposited in the Tailings Management Facility (TMF). The plant site is on steep terrain; footprint optimization and terracing may reduce earthworks costs. The company states both a high-quality copper concentrate and a clean molybdenum concentrate are expected, with non-material deleterious elements.

Infrastructure, logistics and power

The project is accessed by national/provincial highways with a final 58 km along the Limón–Warints road. Concentrate is planned to be transported to the Port of Bolívar near Machala; Bolívar (Machala) and Posorja (Guayaquil) are the planned ports for heavy equipment and materials. Power demand is estimated at 236 MW, to be supplied via a 62.1 km, 230 kV transmission line from the Bomboiza substation. Raw water will be supplied from a rainwater intake on the North Diversion Channel and transported by gravity; non-contact water will be diverted and contact water recycled from the TMF. Project communications will include a fibre-optic line with leased internet and radio backup, redundant switches, industrial Wi-Fi 6E (up to 40 Gbps), ~100 4K CCTV cameras with NVR redundancy, biometric/RFID access control, TETRA radios and a centralized monitoring centre. Site accommodation includes a main permanent camp near the plant and temporary camps at Piuntz, Yawi and Warintz for construction.

Tailings and waste rock

The TMF is designed to store ~1.3 Bt of tailings within the Warintza River basin over the projected mine life, contained by four dams in the Warints stream valley. Starter dams will be rockfill with a low-permeability core and a geomembrane liner on Dam No. 1, with centreline raises thereafter. Cycloning will separate coarse fractions for dam construction; fine fractions will be deposited in the TMF. Geochemical modelling indicates neutral pH at the final collection point based on current testing. The upstream Waste Rock Facility is designed for ~670 Mt and will be placed from downstream to upstream for stability.

Permitting, environmental and social

Solaris submitted an exploitation-phase Environmental Impact Assessment (EIA) in August 2024 to Ecuador’s Ministry of Environment, Water and Ecological Transition (MAATE), recently incorporated into the Ministry of Environment and Energy (MAE). The company reports it has addressed government inquiries and submitted the final Technical EIA, which is under review. In July 2025, the Sub-Secretary of MAE visited site and met Indigenous and local stakeholders regarding readiness for the Free, Prior and Informed Consultation (FPIC) process required under Ecuadorian law. The company states it is working with MAE to advance Exploitation Agreement permits, with progress on engineering facilities and water management. Environmental and social baseline programs cover biology, cultural resources, geochemistry, hydrology and groundwater.

Solaris reports formal community agreements with the Shuar centres of Warints and Yawi, including a Strategic Alliance (2019) and an Impacts & Benefits Agreement (IBA) signed in 2020 and later updated. As of September 2025, the company says it has signed cooperation agreements with all Indigenous organizations surrounding Warintza, including PSHA and FICSH, described as Ecuador’s two largest Shuar representative bodies, developed with government support. The agreements provide for employment, training, education, local procurement, infrastructure and direct financial benefits.

District context and property

Warintza is part of a porphyry corridor in southeastern Ecuador that includes the Mirador mine to the south and the San Carlos and Panantza deposits to the west. The property comprises nine metallic mineral concessions totalling 26,773 ha (268 km²). Solaris announced an option to acquire up to 100% of ten additional adjacent concessions (~40 km²) considered prospective for porphyry copper and epithermal gold. The site’s average elevation is ~1,200 m, with regional elevations from ~800–2,700 m and slopes of 25°–40°. The climate is tropical humid (Af), ~22.9°C average temperature and ~1,900 mm annual precipitation, permitting year-round operations.

Marketing, streaming and offtake

Production is planned to be sold as copper concentrate with gold and silver by-products and as molybdenum concentrate. The company has a gold streaming agreement with Royal Gold Inc. and a partial offtake agreement with Orion Resource Partners for copper and molybdenum concentrates; the remainder is to be sold on the open market. Treatment and refining charges are based on regional benchmarks for similar products.

Company statement

Matthew Rowlinson, CEO and President of Solaris Resources Inc., said: “Warintza checks every box: global scale, size, and longevity, technical simplicity in a supportive mining jurisdiction, exceptional economics driven by a world-class strip adjusted grade, and above all, optimal timing to production in a tightening copper market. With over 3.7 billion tonnes of Measured and Indicated Resources, 2.1 billion tonnes of Inferred Resources, 1.3 billion tonnes of Mineral Reserves, a low strip ratio, and early access to high-grade material, Warintza stands as one of the most compelling copper development assets anywhere in the world. We are fully funded for a construction decision through a US$200 million non-dilutive financing from Royal Gold earlier this year, while importantly retaining 100% ownership and full strategic control. In a copper market characterized by declining grades, few new discoveries, and increasingly complex permitting environments, Warintza is uniquely positioned to come online at the right moment, helping meet a critical global supply gap, while delivering strong returns to stakeholders. This is a rare window of opportunity: a generational discovery in a mining-friendly jurisdiction, with deep community support and a proven management team driving it forward. The future is bright, and we look forward to unlocking Warintza’s real value.”

Investor presentation

Solaris plans an online presentation today at 14:00 (Zug) / 08:00 (Toronto) via the Investor Meet Company (IMC) platform; the event is open to existing and potential shareholders, and questions can be submitted during the presentation. Registration details are provided in the company announcement.

Capital and operating breakdowns

Initial capital of US$3.729bn comprises (US$M): processing plant including earthworks (1,063), camp and site infrastructure (273), EPCM (256), mine equipment (304), TMF and water management (509), pre-stripping and haul road construction (179), other preliminary works/project team & G&A/IT/light vehicles (89), indirect costs (310), contingency (505) and VAT (242). Sustaining capital totals US$1.713bn, including open pit (736), infrastructure (356), TMF (239), water management (211), processing plant (65) and indirect/studies (106). LOM operating costs sum to US$3,116m mining (US$1.38/t moved), US$7,250m processing (US$5.58/t milled) and US$1,010m G&A (US$0.78/t milled).

In one of the largest transactions in the gold sector in recent years, Coeur Mining (NYSE: CDE) announced it will acquire New Gold Inc. (TSX: NGD) in an all-stock merger valued at approximately $7 billion, forming a new heavyweight in North American precious metals production. The move comes during a historic rally in gold prices, which have surged above $4,000 per ounce this year, with expectations across the industry that the metal could surpass $5,000 per ounce within the next 12 months.

Under the agreement, investors in New Gold will receive 0.4959 shares of Coeur for each New Gold share, representing a premium of about 16% based on Friday’s closing prices. The merged entity will have a combined valuation of roughly $20 billion, positioning it among the leading gold and silver producers in North America.

Combined Operations and Production Outlook

The new company will merge Coeur’s existing operations in the United States and Mexico with New Gold’s two producing mines in Canada, bringing together a geographically diversified portfolio of assets across the continent. The combined group is expected to produce approximately 900,000 ounces of gold and 20 million ounces of silver next year, significantly expanding Coeur’s current production profile.

Coeur stated that the transaction will strengthen its balance sheet and cash flow, providing “greater strategic flexibility.” The company also indicated that the integration of New Gold’s operations is expected to lower overall production costs and improve profit margins.

Following the merger, Coeur will maintain New Gold’s Toronto office and pursue a Canadian stock market listing, reflecting its expanded presence in Canada and commitment to maintaining ties with the country’s mining sector and investor base. Coeur, currently headquartered in Chicago, said the move will help facilitate broader North American market engagement.

Market Context and Industry Trends

The deal comes amid an environment of strong investor sentiment toward precious metals, driven by record gold prices and a surge in global demand for safe-haven assets. The gold price rally has propelled the valuations of mining companies across the sector, and both Coeur Mining and New Gold have seen their shares triple in 2025, reflecting renewed market confidence in the long-term fundamentals of gold and silver.

The merger continues a wave of consolidation in the mining industry as producers seek to scale up operations, reduce costs, and diversify geographically. The combined entity’s size and output will place it among the most significant gold producers operating in North America, with exposure to both gold and silver markets.

Coeur emphasized that absorbing New Gold’s assets will enhance its production base while providing a stronger platform for growth in both precious metals. New Gold’s established operations in Canada are viewed as complementary to Coeur’s existing portfolio, which includes mines in Nevada, Alaska, and northern Mexico.

Analysts have noted that the transaction gives Coeur a stronger footing in politically stable jurisdictions and adds operational diversity at a time when resource nationalism and regulatory risks are rising in some global mining regions. The expected cost efficiencies from the merger are also anticipated to improve the company’s ability to weather potential price fluctuations in the metals markets.

As gold prices continue to hover near all-time highs, the newly merged miner will begin operations in a favorable economic environment, supported by strong bullion demand and robust silver prices. With an annual gold output projected at nearly one million ounces, the new Coeur-New Gold entity will stand as one of North America’s major players in precious metals production, reflecting the broader trend of consolidation reshaping the mining landscape.

Anglo Asian Mining has signed a sales agreement with global commodities trader Trafigura for the concentrates produced at its newly commissioned Demirli copper mine in Azerbaijan, marking a major step forward in the company’s transition toward becoming a predominantly copper-focused producer.

The London-listed miner (LON: AAZ) confirmed that the agreement includes a revolving prepayment facility of up to $25 million, which will provide additional financial flexibility as Demirli ramps up output. The first shipment under the Trafigura contract is expected to be completed by mid-November, the company said.

The Demirli mine, located in the Karabakh region, was successfully commissioned in July 2025. Production from the site is forecast to reach approximately 4,000 tonnes of copper in concentrate during its first year of operation. Anglo Asian anticipates that annual output could increase significantly to around 15,000 tonnes beginning in 2026 as operations scale up.

Demirli is the second copper operation Anglo Asian has brought online this year. In May, the company began production at its Gilar underground deposit, which hosts estimated resources of 54,000 tonnes of contained copper. Both projects form part of Anglo Asian’s longer-term strategy to reposition itself as a major regional copper producer by 2029. For nearly two decades, the company’s primary focus had been on gold, largely through operations at the Gedabek open pit mine.

Anglo Asian also confirmed that it has received the necessary Azerbaijani government approvals to execute the Trafigura sales contract and to operate its processing facilities at Demirli. Final documentation related to the licensing process is still being completed, but the company said all essential permits are now in place to support full-scale operations.

Among the approvals was authorization to utilize the existing tailings storage facility for up to 12 months. During that period, a new, dedicated tailings dam will be constructed to support the mine’s future expansion. The company also stated that the operating lease for the Demirli processing plant officially commenced on October 1, 2025.

Anglo Asian chief executive Reza Vaziri described the receipt of the final licenses and completion of the Trafigura sales agreement as significant developments for the company’s operations in Azerbaijan. “I am delighted that we have received all the relevant licenses to operate the plant and tailings dam at Demirli, an important milestone as the mine becomes fully operational and increasingly contributes to group production,” Vaziri said in a statement.

He added that the combination of regulatory approvals and the Trafigura sales contract “enables us to now commence copper concentrate sales and deliver value from Demirli.”

The addition of the Demirli and Gilar mines expands Anglo Asian’s portfolio beyond its long-standing gold assets and aligns with its broader plan to shift its production base toward copper and other critical minerals over the remainder of the decade. The company has said it expects the ramp-up of these assets to strengthen its operational and financial position as global demand for copper continues to rise.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

CMC Metals Ltd. CMC Metals Ltd. |

CMB.V | +900.00% |

Eden Energy Ltd Eden Energy Ltd |

EDE.AX | +200.00% |

| GoviEx Uranium Inc. |

GXU.V | +42.86% |

| Eagle Nickel Ltd. |

ENL.AX | +41.67% |

| Citigold Corp. Limited |

CTO.AX | +33.33% |

| Mount Burgess Mining NL |

MTB.AX | +33.33% |

| Exalt Resources Limited |

ERD.AX | +31.94% |

| Casa Minerals Inc. |

CASA.V | +30.00% |

| Cariboo Rose Resources Ltd |

CRB.V | +28.57% |

| Belmont Resources Inc. |

BEA.V | +28.57% |