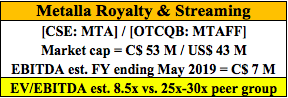

The following interview of CEO Brett Heath of Metalla Royalty & Streaming (CSE: MTA) / (OTCQB: MTAFF), was conducted by phone & email over the 3-day period ended January 21st. Metalla is a well-run, rapidly growing, precious metals Royalty & Streaming company that is relatively unknown. The Company’s tried and true business model typically commands a premium market valuation, led by industry darlings like Franco-Nevada (TSX-V: FNV) / (NYSE: FNV), Royal Gold (NYSE: RGLD) and Wheaton Precious Metals (NYSE: WPM).

{Bios of Mr. Heath and other key executives}

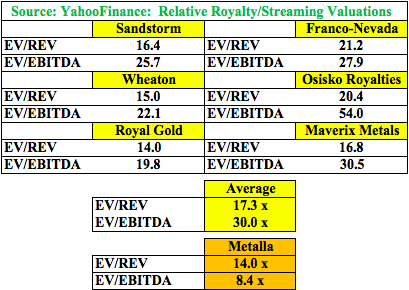

Management believes its valuation is meaningfully lower than its peers. According to YahooFinance; peers are trading at an average trailing 12 months EV/EBITDA ratio of 30.0x (25.2x excluding Osisko’s elevated 54.0x ratio), and an average EV/Revenue ratio of 17.3x. By contrast, Metalla’s anticipated [FY 2018 ending May 31, 2018] EV/EBITDA metric is just 8.4x — a 72% discount (8.4x vs. 30.0x) to its peer group.

CEO Brett Heath commented in the interview that EBITDA for FY 2019, (ending May 31, 2019), could be ~C$8-$10 M based only on existing assets in the portfolio, meaning that the 2019 EV/EBITDA ratio might be as low as ~6.5x. Pro forma for prospective new royalty/streaming acquisitions, Heath thinks EBITDA could be running at “well above” C$10 M by next year. Management expects at least 4 new deals in 2018.

At some point this year, or in my opinion by early 2019 at the latest, investors will have enough demonstrated cash flow and dividend history — and visibility towards future cash flows — to warrant a higher EV/EBITDA valuation. How much higher remains to be seen, but cutting the discount from 72% from to 40% (from and EV/EBITDA ratio of 8.4x to 18.0x) would allow for a doubling in Metalla’s share price.

Here’s my interview with Brett.

I received my first (monthly) dividend check in the mail… Thanks! What can you tell us about the dividend program moving forward this year?

We are very excited to have accomplished this important milestone early on as a company. The power of compounding dividends over time is significant when looking at total return. We expect to continue to raise the dividend this year until we reach 50% of after tax and G&A cash flow. Based on our last quarter, that has the potential to get to C$0.003/month (from C$0.001/month).

That might not sound like a lot, but it would be a 5.0% dividend yield — (all else equal, assuming no new share issuance for acquisitions) — based on the current C$0.72 share price. That would be triple the next highest yield in the precious metals royalty & streaming sector. NOTE: {Wheaton Precious Metals (NYSE: WPM) is yielding 1.62%}.

The board will meet quarterly to adjust the dividend based on silver & gold prices and the operating performance of mines that we have royalties or streams on. We started with a low dividend rate to maintain a strong balance sheet to facilitate upcoming transactions.

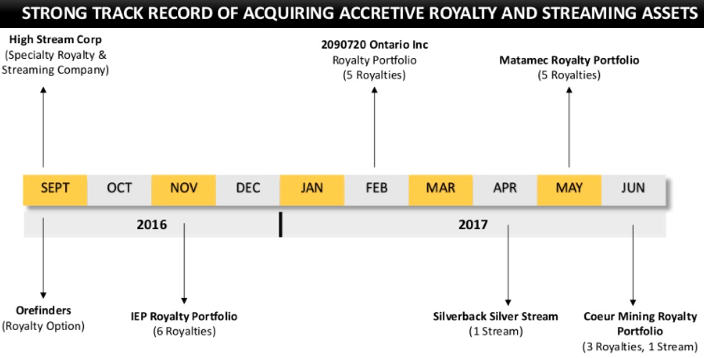

Please update readers on potential acquisitions of new royalty & streaming assets, are you close on anything?

Yes, we are working on some very exciting deals and hope to close at least 4 transactions this year.

Metalla’s cash flow is heavily weighted towards silver, will it remain that way, or do you expect cash flow from gold assets to even things out?

Good question. It just so happens we are overweight silver vs. gold by virtue of executing on the best available deals at the time. We do expect gold assets to fill in as we complete more transactions. That being said, we will be heavily weighted towards silver over the next couple of years. Silver often outperforms gold in bull markets, so we are very comfortable with our positioning.

Investors have been waiting months for Metalla to be up-listed to the TSX Venture exchange. Why is it taking so long?

We are very close. I can assure you that it has been as frustrating for management as it has been for shareholders and prospective investors. A lot of it has been out of our control unfortunately, but it remains a priority and we will be a tier 1 issuer. Given the growth profile of the Company, we will be evaluating a U.S. listing as early as next year.

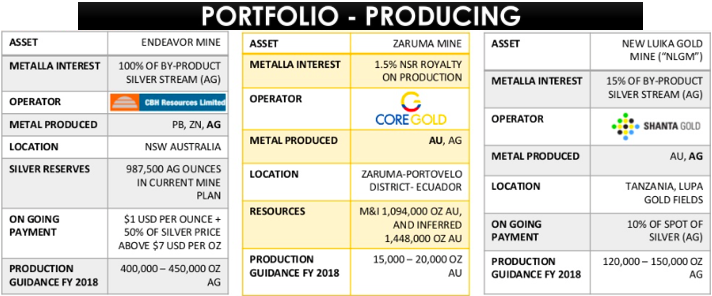

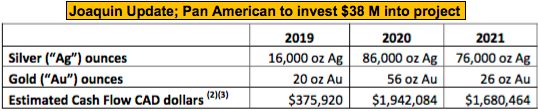

In December, your team provided an update on its 2% on the NSR Joaquin project. Tell us about Joaquin and explain the update’s significance?

This was a great update for Metalla shareholders. Pan American Silver is allocating $40 M to develop Joaquin with production starting in 2019. What this means is Metalla will have another top tier counter-party in the producer category. The mine plan is only based on one high-grade zone of the overall deposit. This asset will most likely cash flow to Metalla for many years. Our suspicion is that if we see higher silver prices, Pan American is likely to scale up the production profile.

What is your team’s latest estimate of cash flow for the fiscal year ending May 31, 2018? How should investors think about next year’s cash flow?

We are on track to hit our goal of CAD $6 M in operating cash flow for FY 2018 (ending May 31, 2018). First quarter (FY 2018) production was lower due to the ramp up of the Endeavor mine. We haven’t given formal guidance on FY 2019 yet, but internal estimates are looking to be in the CAD $7M – $9M range. That’s not including any new deals. With the addition of new transactions, our goal is to reach an annualized rate well north of CAD $10 M within the next 12 months.

Is Metalla paying any cash taxes? Or, are you benefiting from historical operating losses to offset earnings?

Unlike more established industry leaders like Franco-Nevada, Wheaton Precious Metals and Royal Gold, we don’t expect to pay any cash taxes for several years. This will support our dividend paying ability.

A slide in your corporate presentation shows how Metalla stacks up against its peers. Can you talk about that?

Yes, we are relatively unknown to investors, which might be why our valuation appears cheap compared to peers. Our FY 2018 cash flow estimate, plus ~C$1 M in “G&A,” is ~C$ 7 M in EBITDA. Our EV (market cap + debt – cash) is roughly C$ 59 M (we have ~C$ 3 M in cash & ~C$ 8.5 M of low coupon, unsecured convertible debt owned by our largest shareholder Coeur Mining). That gives us an EV/EBITDA ratio of about 8 and a half, compared to well over 20x for our peer group.

Admittedly, part of our valuation discount is probably warranted– we are a new company with a less proven track record, and we are under-followed, for example we don’t have any sell-side research coverage. But, as we grow, we believe our valuation gap will close, perhaps by a lot.

Thanks Brett. It sounds like the story is poised to gain traction with a Tier I TSX-V listing right around the corner, new acquisitions, a rising dividend payout and a cheap valuation. I look forward to updates on Metalla Royalty & Streaming (CSE: MTA) / (OTCQB: MTAFF) in the weeks and months to come.

Disclosures: The content of this interview is for illustrative and informational purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research, [ER] including but not limited to, commentary, opinions, views, assumptions, reported facts, estimates, calculations, etc. is to be considered implicit or explicit, investment advice. Further, nothing contained herein is a recommendation or solicitation to buy or sell any security. Mr. Epstein and [ER] are not responsible for investment actions taken by the reader. Mr. Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Mr. Epstein and [ER] are not directly employed by any company, group, organization, party or person. Shares of Metalla Royalty are speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned shares in Metalla Royalty and the Company was an advertiser on [ER]. By virtue of ownership of the Company’s shares and it being an advertiser on [ER], Peter Epstein is biased in his views on the Company. Readers understand and agree that they must conduct their own research, above and beyond reading this article. While the author believes he’s diligent in screening out companies that are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.