Silver recently started outperforming gold again, a watershed event. For long years this white metal has mostly lagged the yellow one, relentlessly battering silver sentiment. But gold surging into year-end 2018 finally sparked some life into moribund silver. This is a bullish sign, as silver has soared in the past once rising prices reach critical mass in attracting new investment capital. Silver looks to be nearing that point again.

Despite a good finish, 2018 was a rough year for silver. Its price slumped 8.6%, way worse than gold’s -1.6% performance. And that still masks miserable intra-year action. At worst in mid-November, silver had plunged 17.3% year-to-date. That was 2.2x gold’s comparable loss, and at $13.99 silver languished at a major 2.8-year low. A soul-crushing 96% of its early-2016 bull market had been reversed and lost!

Back in December 2015 silver had bottomed a few days before gold at a deep 6.4-year secular low. Over the next 7.6 months silver soared 50.2% higher, outpacing gold’s parallel new-bull upleg by 1.7x. That promising start didn’t pan out though, silver crumbed once gold’s advance stalled and failed. Ever since its August 2016 peak of $20.56, silver mostly ground sideways sandwiched between two major downlegs.

It was the latter one that finally bottomed in mid-November 2018, with hope lost and silver bearishness universal and suffocating. Silver’s fortunes are heavily dependent on gold, and silver effectively acts like a gold sentiment gauge. The weak silver prices reflected the lack of enthusiasm for gold, which wasn’t far above its own 19.3-month low of mid-August. Gold had slumped to $1200, and threatened to break below.

For better or worse, gold drives silver. Traders usually ignore the tiny silver market until gold has rallied long enough and high enough to convince them its upside momentum is sustainable. So when gold itself is down in the dumps, silver doesn’t have a prayer. But gold bottomed that day and started clawing back higher, so silver joined along in the bounce. That gradually grew into a new silver upleg over the next 8 weeks.

By early January, silver had rallied 12.4% on a 7.7% gold rally. That made for 1.6x upside leverage to gold, which is still on the low side historically. But it was a welcome change after silver spent much of last year sliding considerably. A sub-span of that advance really caught my attention. Between the hawkish FOMC meeting on December 19th to the young new year on January 3rd, silver surged 7.9% in 9 trading days.

That was 1.9x gold’s 4.2% advance, and silver’s best outperformance relative to gold since that major upleg in H1’16! Something was changing in the left-for-dead silver market, with capital starting to return after more than a couple years of self-imposed exile. Over this past week silver enjoyed another solid stretch of outperformance, offering further confirmation. It started last Friday when gold itself soared 1.7%.

Gold ignited after a Wall Street Journal article claiming the Fed was considering ending its quantitative tightening early! That dovishness hit the U.S. dollar and catapulted gold higher. Over the next 4 trading day’s silver surged 4.8% on gold’s 3.0%, for 1.6x leverage. If that buying can push silver high enough to reach a psychological critical mass and become self-feeding, it portends major silver upside in coming months.

The more silver rallies, the more speculators and investors will want to buy it. The more capital they push into silver, the faster it will ascend. Buying begets buying in silver just like almost everywhere else in the markets. While upside momentum in itself is bullish anytime, silver’s upside potential is far greater than usual because it has been so darned undervalued. That’s made room for massive mean-reversion gains.

Silver’s “valuation” can be inferred relative to gold, its dominant driver. While the global silver and gold supply-and-demand profiles are independent with little direct linkage, these precious metals are joined at the hip psychologically. Silver rarely rallies materially unless gold leads the way. Silver traders look to gold for cues, which makes silver amplify gold’s moves. Silver’s technical relationship to gold is ironclad.

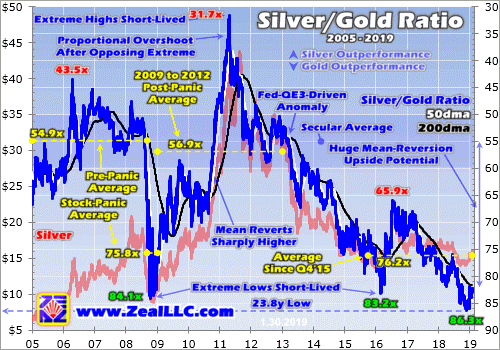

All this makes the Silver/Gold Ratio the most-important fundamental measure of silver-price levels. It is technically calculated by dividing daily silver closes by daily gold closes. But that yields tiny decimals that are hard to parse mentally, like the mid-week SGR of 0.012x. It is far more brain-friendly to consider this ratio from the opposite direction, via the Gold/Silver Ratio. This week it ran at an easier-to-comprehend 82.2x.

Mathematically the SGR is identical to an inverted GSR. So charting the GSR with an upside-down scale yields the same line as the SGR, but with way-more-intelligible numbers. Here this inverted-GSR SGR proxy in blue is superimposed over the silver price in red. Silver has rarely been lower relative to gold than it was in recent months. That portends monster upside as silver mean reverts higher leveraging gold.

At that latest secular silver low in mid-November, the SGR fell to 85.9x. In other words, it took nearly 86 ounces of silver to equal the value of one ounce of gold. While silver started recovering, it initially lagged gold enough to force the SGR lower still. At the end of November it slumped as low as 86.3x on close, an astounding level. That was actually an extreme 23.8-year secular low in the SGR, nearly a quarter-century!

Silver hadn’t been lower relative to gold since early March 1995, practically a lifetime ago considering all that’s happened in the financial markets since. Even during the greatest market fear event in our lifetimes the SGR wasn’t lower. During late 2008’s first-in-a-century stock panic, the SGR just briefly hit 84.1x in mid-October. Being highly-speculative and super-sensitive to sentiment, silver had plummeted leading into it.

That stock-panic episode of extreme SGR lows shows what’s probable after silver inevitably reverses and mean reverts higher. Over the 3.7 years since 2005 leading into that panic, the SGR averaged 54.9x. That was right in line with the mid-50s that had been normal for decades. Silver had generally oscillated around 1/55th the price of gold, so miners had long used 55x as the proxy for calculating silver-equivalent ounces.

With silver so radically out of whack relative to gold, those extreme SGR panic lows weren’t sustainable. Like a beachball pushed too far under water, silver was ready to explode higher to reestablish its normal relationship with gold. That indeed happened during the post-panic years. After plummeting as low as $8.92 in late-November 2008, silver more than doubled by early December 2009 with a 115.4% gain.

While silver was really outperforming gold after its anomalous lows, at best in that initial post-panic rally the SGR only regained 58.6x. That was still below the 55x secular average. So silver continued slowly grinding higher on balance into late 2010. Then gold started surging again, creating the right sentiment conditions to unleash self-feeding silver buying. Silver skyrocketed from there, surging far faster than gold!

The faster silver soared into early 2011, the more traders wanted to own it and the more capital they poured into it. This psychological phenomenon of higher prices being more attractive runs through nearly all markets. The crazy bitcoin mania in late 2017 was a recent example. Silver’s virtuous circle of surging and new capital inflows finally climaxed in late April 2011 at $48.43 per ounce. That was one heck of a bull.

Starting from those extreme stock-panic lows radically undervalued relative to gold, silver had rocketed 442.9% higher in 2.4 years! And that massive run didn’t simply stop at a 55x SGR, but instead the huge buying momentum drove a proportional upside overshoot. The SGR peaked at 31.7x, which was 4/5ths as far above that long-term 55x mean as the SGR was below it at stock-panic lows. This principle is crucial.

After longstanding price relationships driven by some kind of inexorable fundamental or psychological links are forced to extremes, they don’t just mean revert. That reversion momentum blasts them right through their average to overshoot proportionally towards the opposing extreme! This behavior is very pendulum-like. The farther the SGR is pulled one way, the stronger its swing towards the other side of the arc.

Interestingly that massive mean-reversion-overshoot bull following 2008’s stock panic ultimately dragged the SGR high enough to average 56.9x in those post-panic years between 2009 to 2012. Despite great volatility in this ratio, it continued to gravitate towards that 55x secular mean. That persisted until early 2013 when the Fed’s unprecedented open-ended third quantitative-easing campaign greatly distorted markets.

That year alone the Fed conjured $1020b of QE capital out of thin air to inject into the markets! That forced the flagship US S&P 500 broad-market stock index 29.6% higher that year. Such blistering gains made investors forget about gold and silver, so they fell precipitously. That shattered fragile sentiment leading to multi-year bear markets in the precious metals. Silver leveraged gold’s downside like usual.

Thus the SGR slowly collapsed between early 2013 to early 2016 as gold and silver languished in Fed-driven bear markets. That was a very-challenging time psychologically, scaring away the great majority of contrarian speculators and investors. Ultimately silver plunged so far that the SGR fell to 83.2x at worst in late February 2016. That was an extreme low rivaling the 2008 stock panic’s, which truly defies all reason.

Again such SGR extremes weren’t sustainable, so silver blasted higher with gold and amplified its gains in roughly the first half of 2016. Unfortunately that new-bull upleg was cut short, capping silver at mere 50.2% gains and the SGR at 65.9x. Silver’s typical mean reversion out of extreme SGR lows was indeed underway, but unfortunately it was short-circuited by Trump’s stunning surprise election victory that November.

The stock markets started surging on hopes for big tax cuts soon with Republicans controlling the House, Senate, and presidency. So stock traders dumped gold-ETF shares which hammered the gold price and sucked silver down with it. Silver continued underperforming gold on balance until late November 2018 and that latest extreme 86.3x SGR low. Silver both fell faster than gold and rallied slower than it over this span.

Again that crazy nearly-quarter-century low in silver prices relative to gold prices was more extreme than both during late 2008’s stock panic and after late 2015’s secular low. Shockingly the SGR average since Q4’15 is now running 76.2x, which is actually worse than the 75.8x in the four months in late 2008 hosting that stock panic! Silver has languished far too low relative to gold in recent years, an unsustainable anomaly.

That guarantees a massive mean reversion higher for silver as gold’s young upleg continues to unfold. Seeing gold power higher on balance will motivate speculators and investors to redeploy into silver, which will fuel outsized gains in the white metal. That process is already underway, as proven by silver’s sharp gains relative to gold straddling the dawn of this new year. Silver is starting to outperform gold and mean revert!

Let’s assume the worst-case scenario, a silver upleg that fizzles prematurely due to an exogenous shock like Trump’s election win was back in late 2016. If the SGR merely revisits 65x, at $1250 gold that would mean silver near $19.25. While that’s only a 38% upleg from the mid-November lows, it is still well worth riding. At $1300 and $1350 gold, that very-low 65x SGR would yield silver prices near $20.00 and $20.75.

But with the stock markets almost certainly rolling over into a major new bear, it’s unlikely gold’s upleg will be truncated small again. As long as stocks generally weaken, gold investment demand will remain high driving up gold prices. That will keep traders excited about silver, chasing its gains and bidding it ever higher. It’s hard to imagine the SGR not at least mean reverting to its 55x secular average in this scenario.

At 55x and $1250, $1300, and $1350 gold, silver would power up near $22.75, $23.75, and $24.50. Such levels would make for a total silver upleg of 63%, 70%, and 75% from those deep mid-November lows. So even without a proportional overshoot, silver’s upside potential is big after being hammered to such deep lows relative to gold. Some magnitude of mean reversion higher is certain after such extreme SGR lows.

It would take a major gold upleg running for a couple years to fuel an SGR overshoot. In essentially the first half of 2016, this gold bull’s first upleg powered about 30% higher. That is actually on the small side by historical gold-upleg standards. Apply it to gold’s deep mid-August lows driven by record short selling in gold futures, and that yields an upleg target near $1525. That would work wonders for silver sentiment.

Once gold breaks decisively above its bull-to-date peak of $1365 from July 2016, excitement will explode driving outsized self-feeding investment demand. That should fuel a proportional mean-reversion overshoot in silver. Silver far outperforming gold as capital flooded in could even push the SGR up near 35x briefly. While such an upside extreme wouldn’t last any longer than downside ones, silver would soar.

At $1400, $1450, and $1500 gold, a mean-reversion-overshoot SGR of 35x would catapult silver way up near $40.00, $41.50, and $42.75 per ounce! That implies silver upleg gains ranging from 186% to 206% from mid-November’s low. The key takeaway here is after extreme SGR lows, silver’s resulting mean-reversion gains can grow massive. Silver far outperforms gold for a long time after underperforming for years.

That inevitable outperformance already started through late December and early January, when the SGR recovered sharply from 86.3x to 82.0x. That rapid rebound in silver prices is a strong indication that a major mean reversion is now underway. And history proves that once silver starts moving, it tends to rally fast as momentum builds. Buying begets buying, with higher silver prices fueling larger capital inflows.

As always the biggest gains will be won by the fearless contrarians who buy in early before everyone else figures this out. Investors and speculators alike can play silver’s big coming upside in physical bullion, its leading SLV iShares Silver Trust silver ETF, and the silver miners’ stocks. But only the latter will leverage silver’s gains, making them exceptionally attractive. Consider their example from that last major silver upleg.

Again in 7.6 months in mostly the first half of 2016, silver powered 50.2% higher before Trump’s surprise election win short-circuited that rally. The leading SIL Global X Silver Miners ETF rocketed an immense 247.8% higher in essentially that same span! That made for huge 4.9x upside leverage to silver’s gains, which is pretty awesome. The major silver miners’ stocks will amplify silver’s upside in its next big upleg too.

At Zeal we recognized the extreme anomalous lows in the SGR in late 2015 and early 2016 and deployed aggressively in both gold and silver stocks. The resulting gains were outstanding, with the stock trades in our popular weekly and monthly newsletters averaging +111.0% and +89.7% annualized realized gains in 2016! We’ve filled our trading books again in recent months in anticipation of the next big gold and silver uplegs.

To multiply your wealth in the stock markets, you have to do your homework and stay informed. That’s where our newsletters really help. They draw on my decades of experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. I study the markets all day everyday so you don’t have to. Subscribe today and enjoy the fruits of our hard work for just $12 per issue!

The bottom line is silver has started outperforming gold again. After getting pummeled near a quarter-century low relative to gold, silver started surging late last year. Following past extreme SGR lows, silver powered higher in major-to-massive mean-reversion uplegs and bull markets. Their advents have been signaled by silver beginning to rally faster than gold after suffering long periods of underperformance.

That’s now happening again, which is a super-bullish omen for silver. Capital inflows are accelerating as gold’s gains restore more-favorable sentiment. As long as gold continues meandering higher on balance, silver buying will beget more silver buying. That portends big gains coming in silver and especially the stocks of its miners. Silver mean reversions higher out of extreme lows relative to gold can run for years.

Adam Hamilton, CPA

February 4, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.