First Vanadium Corp. (TSX-V: FVAN) / (OTCQX: FVANF) has been under pressure, along with hundreds of battery metal juniors and the underlying metals including vanadium, cobalt, lithium. Even vanadium giant Largo Resources is down 61% from its 52-week high. Yet, if one believes in vanadium, it’s hard to ignore First Vanadium’s shares at C$0.44, down 78%! The pro forma Enterprise Value [market cap + debt – cash] is just US$12.8M. The Company has C$1.9M in cash.

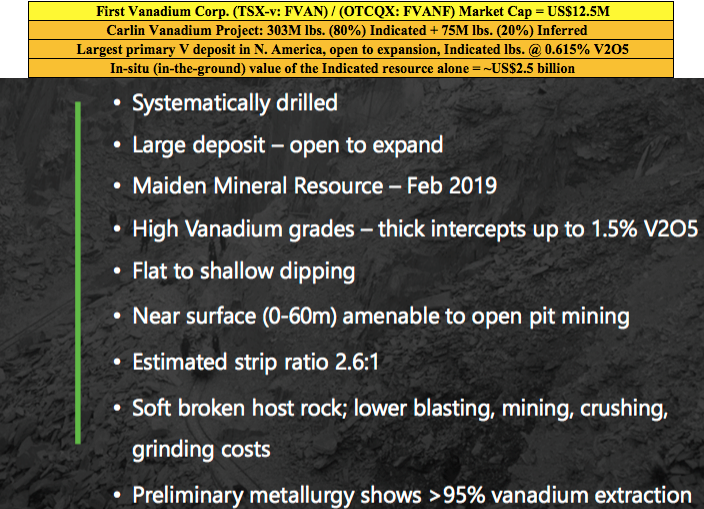

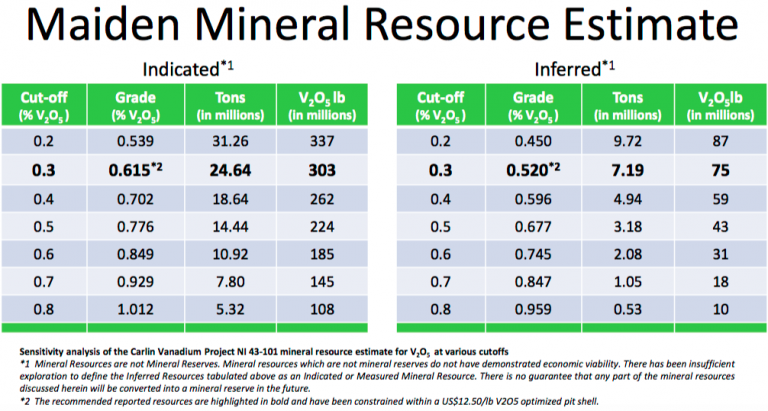

Yet, even at current vanadium pentoxide (“V2O5“) prices, the in-situ value of the Indicated-only portion (303 million pounds) of the Company’s estimated resource is ~US$2.5 billion. Management believes it has the largest high-grade primary vanadium resource in North America.

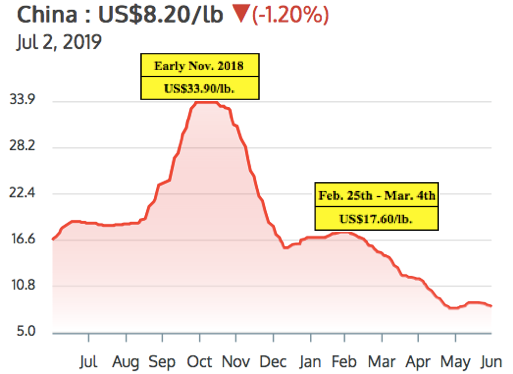

There has been a lot of weeping and gnashing of teeth over the V2O5 (China) price falling from a 2019 high of US$17.6 to its current US$8.2 per pound. But, as the saying goes, the cure to low prices is…. low prices. Few new projects make sense at today’s levels. I believe that V2O5 (China) between US$10-US$15 per pound might be a sweet spot, good for both producers and end users.

Steel companies can afford to pay higher prices for V2O5, but grid-scale, Vanadium Redox Flow Battery (“VRBs“) Energy Storage Systems (outside of China) might need prices below US$10/lb. to go mainstream. Importantly though, VRB plant costs are coming down. Vincent Sprenkle, a lead researcher at the U.S. Department of Energy’s Pacific Northwest National Laboratory, (“PNNL“) recently said, “VRB costs could be lowered by another 50%.” That would be very bullish for vanadium prices, it would allow for widespread adoption of VRBs even with V2O5 prices above US$10/lb.

First Vanadium has a sizable resource, a good grade, in a great jurisdiction. A Preliminary Economic Assessment (“PEA”) is expected by year end. The following interview of Paul Cowley, P.Geo., President, CEO & Director of First Vanadium, was conducted by phone & email between June 24th & July 2nd.

Please tell us about yourself and your team.

I’m an exploration geologist with 40 years’ experience in the discovery & evaluation of mineral deposits around the world. About half of my career was with a Major, BHP Minerals. I was involved in leading the team in the Canadian arctic that made 4 gold deposit discoveries that generated about 6 million ounces of gold. I also worked at Escondida and BHP’s Ekati diamond mine during their exploration days.

I’m a senior guy, but I’m the youngest of our group. The others have even more years of experience. We have two mining engineers that held mine general manager positions of very significant mines at Majors. We have four metallurgists that have worked for Majors, in senior roles. We have a construction engineer who’s built 20 mines in North & South America, he’s currently building Lundin’s mine in Ecuador.

What do you make of the recent volatility in the vanadium price?

Since early March 2019 the vanadium price has taken an unexpected turn lower. Prices are not responding to the bigger picture demand and supply imbalance. Chinese steel plants did not recharge their vanadium inventories in this period, as many expected they would, putting pressure on traders to liquidate at undercutting prices, but they will have to restock. The U.S.-China trade wars, and some shortfall of enforcement of new Chinese rebar standards, appear to have exacerbated the situation in the short term.

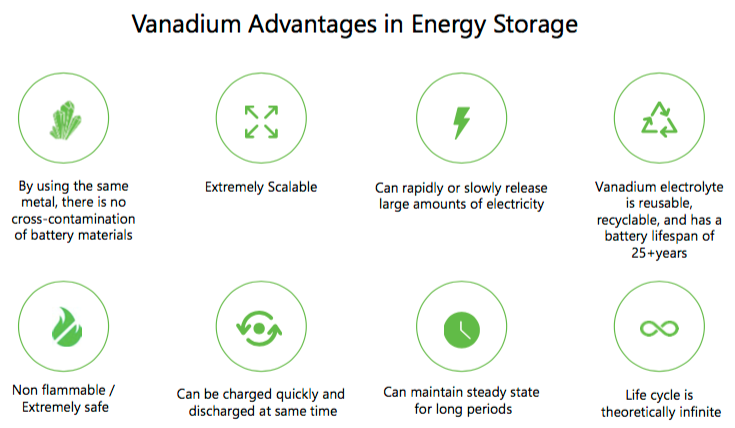

It’s our view that the fundamentals of demand in global steel applications will outstrip supply and should push vanadium prices higher again in the second half of the year, and beyond. Adding to the demand side is the exciting boom in solar & wind projects, all of which require battery storage. This is happening on so many levels around the world that we expect to see the vanadium battery carve out a healthy market share in this expanding renewable space. Some are calling the 2020’s, the Solar Decade.

Please explain the significance of the historical data you recently received, that extended the strike length by 300 meters to the south.

It means more potential than we had expected. From our drilling, the deposit appears to be open to expansion in several areas, but we did not expect the deposit to be open to the south. The newly acquired data demonstrates a 15% strike length increase to the south and it’s still open in that direction. This is exciting news as this data was not included in the resource estimate we put out in February.

You already have a 303 million pound vanadium resource (in-situ value of ~US$2.5 billion) in the Indicated category alone. Does the resource need to get any bigger?

That’s a good question. But it needs to be answered through an economic study. In our view, the resource is sizable. It’s currently the largest, highest-grade primary vanadium resource in North America. Our immediate priority is to demonstrate potential economic viability with what we have, knowing that we believe we could always make it bigger if and when we need to.

Several readers may assume that First Vanadium will need an expensive roaster in its operating flow sheet. What are your latest thoughts?

Not true. The path we are on with our metallurgical flow sheet does not include, or require, a roaster.

Although Nevada is the #1 global mining jurisdiction in the latest Fraser Institute Mining Survey, some complain that it takes a long time to get permits. What does your team expect in this regard?

In general, in the U.S. that is true, but not in Nevada. Nevada has a responsible review and process, but it’s a mining state. And, even more so for us now that vanadium is on the critical minerals list. The U.S. has unveiled its strategy in an effort to rebuild struggling domestic supply chains for metals & minerals it deems “critical” to the country’s manufacturing & defense sectors. Recently this was reiterated when President Trump & Prime Minister Trudeau announced a plan for the U.S. & Canada to collaborate on critical minerals.

What are the latest developments on the metallurgical front?

We continue to make strides on the metallurgical front. In April we announced an average of 95% vanadium extraction from the rock across the deposit, into solution. We do not know what ultimate recoveries will look like just yet, but we are making good progress. And, we’re making strides in the area of pre-concentration, with the aim to reduce the plant size, which would lower the capital intensity of the project.

What are First Vanadium’s plans for a Preliminary Economic Assessment (“PEA”)? Might that be a 1H 2020 event?

No, we think that we can move faster, our aim is to initiate a PEA in the 3rd quarter, with results to be reported before the end of the year.

Why should readers consider buying shares of First Vanadium?

I see very good value and upside; an exceptional senior technical team, a good share structure and a great project. We now have C$1.9 million in cash with the recent private placement closing, and 42.4 million shares. Our share price now is where it was at the beginning of 2018! Yet, we have delivered two successful drill campaigns, a mineral resource with considerably higher grades, and more metal in the ground than our historical resource, and 80% (303 million pounds) of it is in the Indicated category.

That, plus positive metallurgical test work and environmental baseline studies to advance permitting. If one is bullish on the vanadium price, currently at US$8.20/lb., then First Vanadium’s (TSX-V: FVAN) / (OTCQX: FVANF) project in the #1 of 84 ranked global jurisdiction of Nevada should be high on the list of projects to consider investing in.

Thank you Paul, very interesting and timely commentary on the vanadium market and on First Vanadium. I look forward to seeing a PEA later this year!

Peter Epstein

Epstein Research

July 9, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Vanadium Corp., including, but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Vanadium Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of First Vanadium Corp. and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.